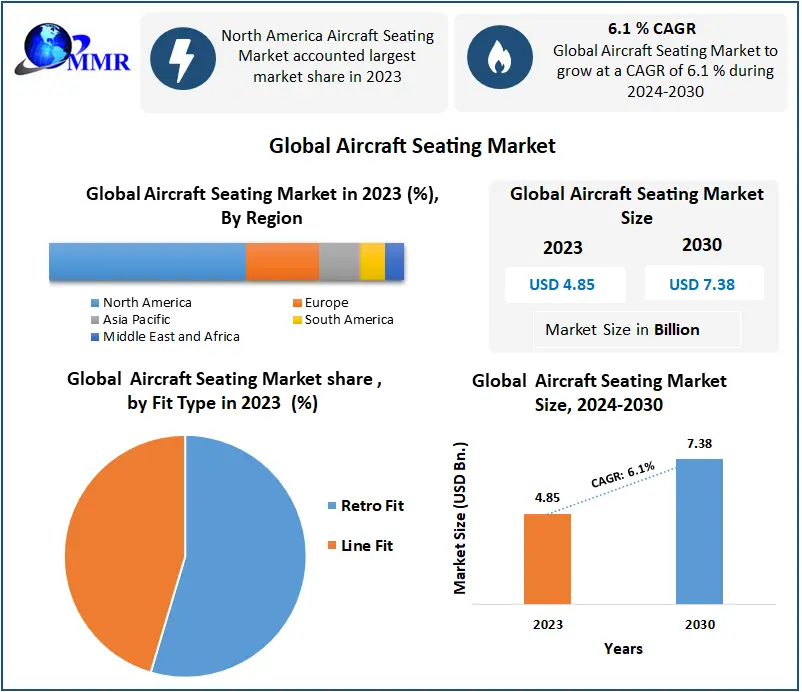

The global airline seating market is undergoing rapid transformation, driven by rising air passenger traffic, increasing demand for fuel-efficient aircraft interiors, and a growing emphasis on passenger comfort and in-flight experience. According to a 2023 report by Mordor Intelligence, the airline seating market was valued at USD 5.1 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 6.8% from 2023 to 2028, reaching an estimated USD 7.7 billion by the end of the forecast period. This expansion is fueled by fleet modernization efforts, especially among low-cost carriers in Asia-Pacific, and heightened demand for premium economy and business class configurations on long-haul routes. Additionally, sustainability initiatives are prompting manufacturers to adopt lightweight materials and modular designs to reduce aircraft weight and carbon emissions. As airlines increasingly prioritize operational efficiency and brand differentiation through cabin experience, the competitive landscape among seat manufacturers has intensified. The following list highlights the top 10 airline seat manufacturers shaping this dynamic industry through innovation, global supply chain capabilities, and strategic partnerships with major aircraft OEMs and carriers.

Top 10 Airline Seat Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Airline Seat

H2: 2026 Market Trends for Airline Seats

The airline seat market in 2026 is poised for significant transformation, driven by evolving passenger expectations, sustainability mandates, technological innovation, and post-pandemic recovery dynamics. As the global aviation industry rebounds and adapts to long-term structural changes, seat manufacturers and airlines are increasingly focused on balancing comfort, cost-efficiency, and environmental performance. Key trends shaping the airline seat market in 2026 include:

1. Lightweight and Sustainable Materials

Environmental regulations and fuel efficiency targets are accelerating the adoption of lightweight composite materials in seat construction. By 2026, a growing number of airlines are expected to prioritize seats made from recyclable, bio-based, or low-carbon footprint materials. Manufacturers such as Recaro, Geven, and Expliseat are expanding their use of magnesium alloys, recycled plastics, and plant-based foams to reduce weight by up to 20%, directly contributing to lower fuel consumption and emissions.

2. Premiumization in Economy and Middle-Market Cabins

Passenger demand for enhanced comfort—especially in economy class—is driving innovation in slimline and adjustable seats. Airlines are investing in ergonomic designs, improved recline mechanisms, and better personal space optimization. Additionally, the rise of “premium economy lite” configurations allows carriers to offer upgraded seating without major cabin reconfiguration, appealing to cost-conscious travelers seeking added comfort.

3. Smart and Connected Seating

Integration of smart technologies into seats is gaining momentum. By 2026, more aircraft are expected to feature seats with embedded sensors, wireless charging, personalized climate control, and connectivity to in-flight entertainment (IFE) systems via personal devices. These features enhance the passenger experience while enabling airlines to collect anonymized data on seat usage and comfort preferences for future design improvements.

4. Modular and Reconfigurable Seat Designs

Flexibility is a key priority for airlines responding to fluctuating demand and route changes. Modular seat systems that allow quick reconfiguration between layouts (e.g., standard economy to premium or family seating) are becoming more prevalent. This adaptability supports dynamic fleet utilization and helps airlines optimize revenue per square foot of cabin space.

5. Focus on Health, Hygiene, and Well-being

Post-pandemic, health-conscious travelers continue to influence design decisions. Antimicrobial surfaces, improved air filtration at the seat level, and enhanced ventilation near seating areas are being integrated into new seat models. Additionally, ergonomic improvements aimed at reducing deep vein thrombosis (DVT) risk and supporting better sleep during long-haul flights are being emphasized.

6. Regional Market Divergence

Market trends vary significantly by region. In Asia-Pacific, high-density configurations remain common due to strong domestic and regional traffic, but with increasing demand for comfort upgrades. In North America and Europe, passenger advocacy and regulatory pressure are pushing airlines toward more spacious and sustainable seating solutions. Meanwhile, Middle Eastern carriers continue to lead in luxury seat innovation, particularly in business and first class.

7. Consolidation and Strategic Partnerships Among Suppliers

The competitive landscape is seeing consolidation, with major players acquiring niche innovators to expand their technology portfolios. Partnerships between seat manufacturers and tech companies are also on the rise, aiming to accelerate the integration of IoT, AI, and data analytics into cabin interiors.

Conclusion

By 2026, the airline seat market will be defined by innovation grounded in sustainability, passenger experience, and operational agility. As airlines face increasing pressure to decarbonize and differentiate their service offerings, investment in next-generation seating will be a critical component of competitive strategy. Manufacturers that successfully combine lightweight engineering, smart features, and modular design will lead the market, shaping the future of air travel comfort and efficiency.

Common Pitfalls in Sourcing Airline Seats: Quality and Intellectual Property Risks

Sourcing airline seats involves significant complexity, with potential pitfalls that can impact safety, compliance, costs, and brand reputation. Two of the most critical areas of concern are quality assurance and intellectual property (IP) risks.

Quality-Related Pitfalls

Sourcing airline seats that meet rigorous aviation standards is essential for passenger safety and operational reliability. However, several quality pitfalls often arise:

Inadequate Supplier Vetting

Failing to thoroughly evaluate a supplier’s certifications, manufacturing capabilities, and track record can lead to substandard products. Airlines must verify that suppliers hold relevant certifications such as FAA, EASA, or other applicable regulatory approvals, and conduct on-site audits to assess production processes and quality control systems.

Non-Compliance with Regulatory Standards

Airline seats must comply with stringent airworthiness regulations, including flammability, crashworthiness (e.g., 16g dynamic testing), and emergency evacuation requirements. Sourcing seats that lack proper certification or fail to meet updated regulations can result in grounding, costly retrofitting, or regulatory penalties.

Inconsistent Build Quality and Material Degradation

Seats sourced from low-cost suppliers may use inferior materials or inconsistent manufacturing practices, leading to premature wear, structural weaknesses, or non-uniform appearance across the cabin. This undermines passenger comfort and increases long-term maintenance costs.

Poor Integration and Fit Issues

Seats must be precisely engineered to integrate with cabin systems (e.g., floor tracks, in-flight entertainment, power, and oxygen systems). Poorly specified or manufactured seats can lead to installation delays, rework, or operational inefficiencies during aircraft delivery or retrofitting.

Intellectual Property (IP) Risks

The design and technology behind modern airline seats often involve protected intellectual property, making IP compliance a critical concern in sourcing:

Use of Counterfeit or Cloned Designs

Some suppliers may offer seats that closely mimic patented or trademarked designs from leading manufacturers. Using such seats exposes airlines to legal liability for infringement, potential product seizure, and reputational damage.

Lack of IP Warranty and Indemnification

Contracts that fail to include clear IP warranties and indemnification clauses leave airlines vulnerable if a third party claims ownership over seat designs or components. Suppliers should affirm that their products do not infringe existing IP rights and agree to cover legal costs if disputes arise.

Unclear Ownership of Custom Designs

When airlines collaborate with suppliers on bespoke seat designs, ambiguous agreements about IP ownership can lead to disputes. Without clear contracts, the supplier may retain rights to design elements, limiting the airline’s ability to reproduce, modify, or transfer the design to another manufacturer.

Exposure to Trade Secret Violations

Sourcing from suppliers with weak internal controls may inadvertently involve the use of trade secrets misappropriated from other companies. Airlines could face secondary liability if they benefit from such practices, even unknowingly.

Mitigating these pitfalls requires due diligence, robust contractual safeguards, and close collaboration with legal and technical experts throughout the sourcing process.

Logistics & Compliance Guide for Airline Seats

Product Classification & Harmonized System (HS) Codes

Airline seats are typically classified under HS Code 8803.30 (Parts of aircraft and spacecraft), specifically covering seat assemblies and components designed for aircraft interiors. Accurate classification is critical for customs clearance, duty assessment, and trade compliance. Confirm the exact HS code with local customs authorities, as subcategories may vary by country and seat complexity (e.g., integrated IFE, motors, or safety systems).

Regulatory Compliance Requirements

Airline seats must comply with stringent aviation safety and environmental standards. Key regulations include:

– FAA (Federal Aviation Administration): 14 CFR Part 25 (airworthiness standards) and Technical Standard Order (TSO) C39e for flammability and crashworthiness.

– EASA (European Union Aviation Safety Agency): CS-25.853 (flammability) and CS-25.561 (seat strength and occupant protection).

– Environmental Regulations: Compliance with REACH (EU) and RoHS (restriction of hazardous substances) for materials used in manufacturing.

– Certification: Seats must carry valid Supplemental Type Certificates (STCs) or Parts Manufacturer Approvals (PMAs) where applicable.

Packaging & Handling Specifications

Proper packaging ensures seats arrive undamaged and meet airline delivery standards.

– Use wooden or reinforced pallets with edge protectors and waterproof wrapping.

– Secure moving parts (e.g., recline mechanisms) with non-marring restraints.

– Label each unit with handling instructions (e.g., “Fragile,” “This Side Up”) and traceability data (serial number, model, destination).

– For international shipments, comply with ISPM 15 for wood packaging material.

Transportation & Shipping Modes

Airline seats are commonly shipped via:

– Air Freight: For urgent deliveries or long international routes; requires IATA-compliant packaging and documentation.

– Ocean Freight: Cost-effective for bulk shipments; use 20’ or 40’ containers with moisture barriers and anti-corrosion protection.

– Ground Transport: Ideal for regional distribution; ensure trailers are enclosed and climate-controlled if needed.

Coordinate logistics with certified freight forwarders experienced in aerospace components.

Documentation & Customs Clearance

Ensure complete and accurate documentation to avoid delays:

– Commercial Invoice (with detailed description, value, and HS code)

– Packing List (itemizing each seat and component)

– Certificate of Origin

– Airworthiness Certification (e.g., FAA 8130-3 or EASA Form 1)

– Bill of Lading or Air Waybill

– Import Permits (if required by destination country)

Import/Export Controls & Licensing

Verify export regulations based on origin and destination.

– U.S. Exports: Subject to ITAR (International Traffic in Arms Regulations) if seats contain defense-related technology; otherwise, EAR (Export Administration Regulations) may apply.

– EU Exports: Check dual-use regulations under EU Regulation 2021/821.

Obtain necessary export licenses and maintain records for audit purposes.

Quality & Traceability Management

Maintain full traceability throughout the supply chain.

– Assign unique serial numbers to each seat.

– Keep records of materials, manufacturing dates, inspection reports, and certifications.

– Implement an AS9100-compliant quality management system for aerospace components.

End-of-Life & Environmental Responsibility

Plan for end-of-life seat disposal in compliance with environmental laws.

– Recycle metals, foams, and fabrics where feasible.

– Dispose of hazardous materials (e.g., fire-retardant coatings) per local regulations.

– Follow airline sustainability programs for cabin retrofitting and component reuse.

Risk Mitigation & Contingency Planning

Identify and manage supply chain risks:

– Maintain buffer inventory for critical programs.

– Use dual sourcing for high-risk components.

– Conduct regular audits of logistics partners and compliance status.

– Develop response plans for customs delays, damage claims, or regulatory changes.

In conclusion, sourcing airline seat manufacturers requires a strategic approach that balances quality, cost, innovation, compliance, and long-term partnership potential. Airlines must evaluate suppliers based on stringent safety and regulatory standards, product durability, weight efficiency, passenger comfort, and customization capabilities. Leading manufacturers such as Recaro, Safran, and Collins Aerospace offer proven track records and advanced technologies, while emerging players may provide competitive pricing and innovative designs.

A successful sourcing strategy should include thorough due diligence, lifecycle cost analysis, and consideration of sustainability trends, such as recyclable materials and fuel-efficient lightweight designs. Furthermore, building strong supplier relationships and incorporating flexibility for future upgrades will support operational resilience and enhance the passenger experience. Ultimately, selecting the right seat manufacturer contributes significantly to an airline’s brand reputation, operational efficiency, and competitive advantage in the global aviation market.