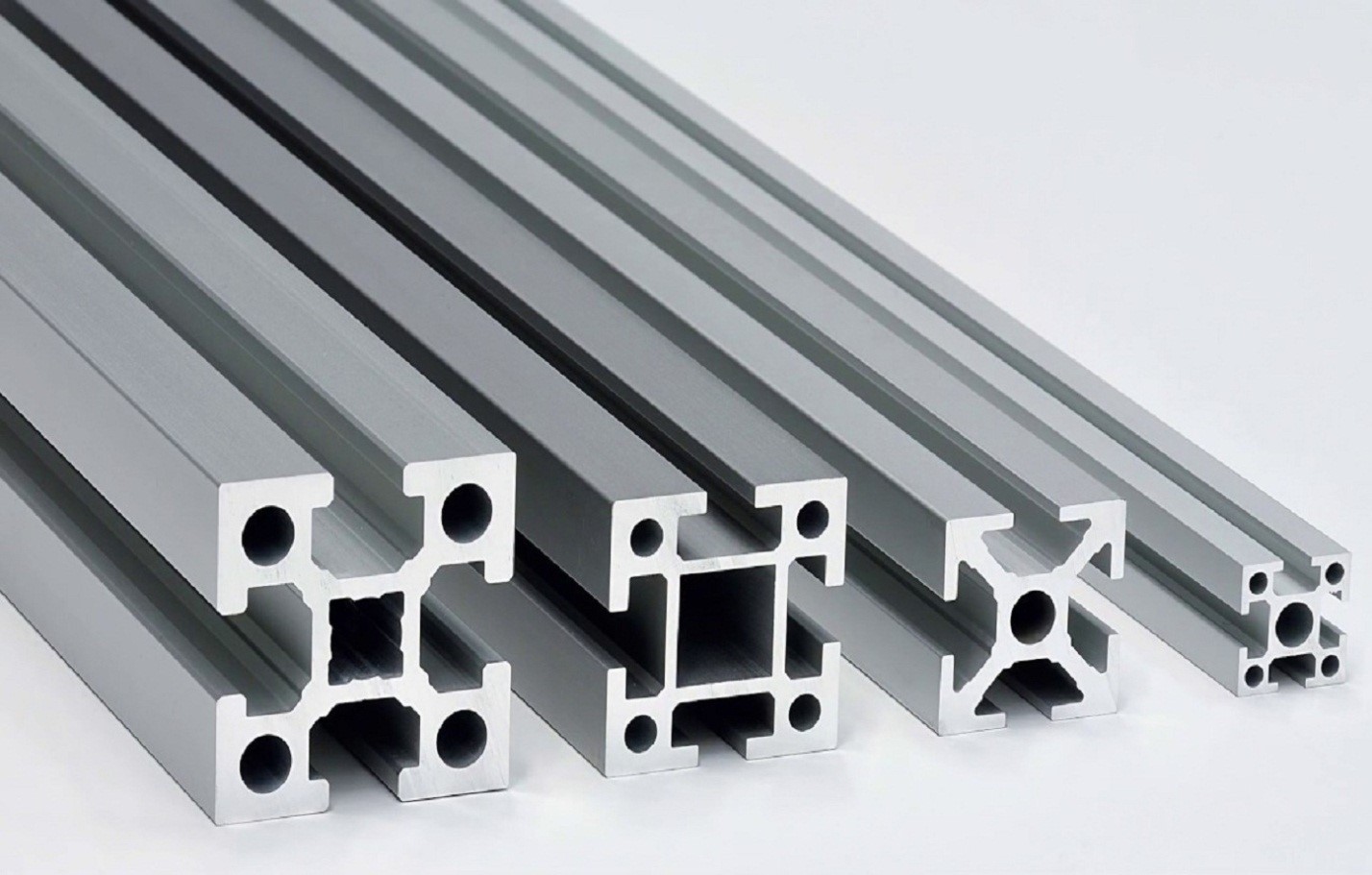

The global aluminium profiles market is experiencing robust growth, driven by rising demand in construction, automotive, and renewable energy sectors. According to Grand View Research, the global aluminium profiles market size was valued at USD 86.7 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 5.8% from 2023 to 2030. Increasing urbanization, infrastructure development, and the shift toward lightweight, energy-efficient materials are key factors fueling this expansion. China, as the world’s largest producer and consumer of aluminium, plays a dominant role in this landscape—accounting for over 50% of global aluminium production and hosting a dense network of profile extrusion manufacturers. Domestic policies supporting green buildings and sustainable transportation further strengthen the industry’s momentum. Against this backdrop, identifying the leading aluminium profile manufacturers in China is essential for global buyers seeking quality, scale, and innovation. The following list highlights the top eight manufacturers based on production capacity, technological capabilities, export footprint, and market reputation—companies that are shaping the future of the global aluminium value chain.

Top 8 Aluminium Profile In China Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Aluminium Profile In China

H2: Market Trends for Aluminium Profiles in China (2026)

By 2026, China’s aluminium profile market is poised for significant transformation, driven by shifting industrial demands, technological advancements, and evolving sustainability priorities. The market will likely exhibit the following key trends:

H2: Continued Growth in High-Performance and Specialized Applications

The most dynamic growth will occur in high-value segments, moving beyond traditional construction uses:

* Green Building & Energy Efficiency: Stringent national building energy efficiency standards (e.g., “China Standard for Energy Efficiency in Public Buildings”) will drive demand for thermally broken and highly insulating aluminium profiles in windows, curtain walls, and doors. Profiles designed for passive houses and net-zero energy buildings will gain prominence.

* New Energy Vehicles (NEVs): This sector will be a major growth engine. Demand for lightweight, high-strength aluminium profiles for EV battery trays, motor housings, chassis components, and structural parts will surge as automakers intensify weight reduction efforts to extend range. Precision extrusion and complex cross-sections will be critical.

* Renewable Energy Expansion: The massive rollout of solar power (especially large-scale PV farms and rooftop installations) will significantly boost demand for aluminium profiles used in solar panel mounting systems (racks, trackers). Profiles for wind turbine components will also see steady growth.

* Electronics & 3C Products: Demand for high-precision, anodized, or painted aluminium profiles for laptops, smartphones, tablets, and consumer electronics enclosures will remain strong, driven by consumer preference for premium finishes and durability.

H2: Intensified Focus on Sustainability and Green Production

Environmental regulations and carbon neutrality goals (China’s “Dual Carbon” targets) will profoundly reshape the industry:

* Green Aluminium Sourcing: Downstream fabricators and end-users (especially in export-oriented sectors and EVs) will increasingly demand aluminium profiles produced with low-carbon or recycled content. This will pressure upstream smelters to adopt more renewable energy and improve recycling rates. “Green aluminium” premiums may emerge.

* Energy Efficiency in Extrusion: Manufacturers will invest heavily in energy-efficient extrusion presses, oven technologies, and optimized heat recovery systems to reduce Scope 1 & 2 emissions and comply with stricter energy consumption quotas.

* Circular Economy Emphasis: Closed-loop recycling within manufacturing facilities and increased use of post-consumer scrap in extrusion billets will become standard practice, reducing reliance on primary aluminium and lowering the overall carbon footprint. Government policies will likely incentivize this shift.

* Sustainable Product Design: Design for disassembly, recyclability, and reduced material usage in profile designs will gain importance.

H2: Technological Advancement and Automation

To maintain competitiveness and meet complex demands, the industry will accelerate its technological adoption:

* Advanced Extrusion Technologies: Wider adoption of high-speed extrusion, precision die technology, and complex multi-cavity dies for intricate profiles (common in EVs and electronics) to improve yield and consistency.

* Increased Automation & Smart Manufacturing: Integration of automation in handling, inspection (e.g., AI-powered visual defect detection), surface treatment (anodizing, powder coating), and logistics within “smart factories” to enhance productivity, quality control, reduce labor costs, and minimize defects.

* Digitalization & Industry 4.0: Implementation of MES (Manufacturing Execution Systems), IoT sensors for real-time monitoring of extrusion parameters, and digital twins for process optimization and predictive maintenance.

H2: Market Consolidation and Value Chain Integration

The competitive landscape will continue to evolve:

* Consolidation: Smaller, less efficient, or non-compliant producers (especially those using older, polluting technologies) will face increasing pressure from regulations and competition, leading to market consolidation. Larger players with scale, technology, and access to green energy/resources will gain market share.

* Vertical Integration: Leading companies will strengthen control over the value chain, integrating backwards into recycling and potentially billet production, or forwards into system solutions (e.g., supplying fully fabricated window systems or solar mounting solutions).

* Focus on Niche Expertise: Success will increasingly depend on specialization in high-growth, high-margin niches (e.g., automotive-grade profiles, ultra-high-precision electronics profiles, specialized solar trackers) rather than competing solely on volume in commoditized construction segments.

H2: Evolving Raw Material and Cost Dynamics

- Billet Price Volatility: The market will remain sensitive to fluctuations in primary aluminium (LME) prices and the availability/cost of high-quality recycled aluminium scrap.

- Energy Cost Pressure: Rising industrial electricity prices and carbon pricing mechanisms (like the national ETS potentially expanding to include manufacturing) will be significant cost factors, favoring efficient producers located near renewable energy sources.

- Trade Dynamics: Export competitiveness may be influenced by global tariffs (e.g., potential anti-dumping duties) and China’s own export policies on semi-finished goods. The focus may shift towards higher-value fabricated exports.

In summary, the 2026 Chinese aluminium profile market will be characterized by a strategic pivot towards high-value, sustainable, and technologically advanced applications. Success will require manufacturers to embrace green production, invest in automation and R&D, specialize in growth sectors like NEVs and renewables, and navigate a landscape marked by consolidation and stringent environmental regulations. The era of growth driven solely by basic construction demand is waning, replaced by a focus on quality, innovation, and sustainability.

Common Pitfalls Sourcing Aluminium Profiles in China (Quality, IP)

Sourcing aluminium profiles from China offers cost advantages and manufacturing scale, but buyers often encounter significant challenges related to quality consistency and intellectual property (IP) protection. Being aware of these pitfalls is crucial for mitigating risk and ensuring a successful procurement strategy.

Quality Inconsistencies and Lack of Standardization

One of the most frequent issues is inconsistent product quality across batches. While some Chinese manufacturers produce high-grade extrusions, others may cut corners to reduce costs. Common quality problems include dimensional inaccuracies, surface defects (such as scratches, dents, or uneven anodizing), improper alloy composition, and failure to meet specified tolerances (e.g., ISO 2768 or customer-specific standards). This inconsistency often stems from inadequate quality control processes, use of recycled or substandard raw materials, and limited adherence to international testing protocols. Buyers may also face mislabeling of alloy grades (e.g., passing off 6060 as 6063), which impacts mechanical performance and durability.

Inadequate or Non-Compliant Surface Finishes

Surface treatment is a critical aspect of aluminium profiles, particularly for architectural or consumer-facing applications. Pitfalls include uneven anodizing thickness, color variation between batches, poor adhesion of powder coatings, and susceptibility to corrosion. Some suppliers may not follow proper pre-treatment processes (e.g., etching, rinsing, sealing), resulting in finishes that fail salt spray or humidity tests. Additionally, environmental regulations on coatings (such as REACH or RoHS compliance) may not be strictly observed, leading to potential compliance issues in export markets.

Weak Intellectual Property Protection and Design Theft

Sourcing involves sharing technical drawings, 3D models, and custom profile designs—valuable IP that is vulnerable in China’s manufacturing environment. Despite legal frameworks, enforcement of IP rights remains challenging. A significant risk is unauthorized replication: suppliers may produce and sell your custom-designed profiles to competitors, often at lower prices. Some manufacturers may even register your design under their own name, complicating legal recourse. Non-disclosure agreements (NDAs) are commonly used but may lack enforceability without proper jurisdiction and legal support.

Supply Chain Opacity and Subcontracting Risks

Many sourcing agents or export companies do not manufacture the profiles themselves but subcontract to third-party extruders. This lack of transparency makes it difficult to verify production conditions, quality control, or compliance with specifications. Buyers may believe they are dealing directly with a reputable factory, only to discover later that production was outsourced to a lesser-known facility with inferior capabilities. This fragmentation increases the risk of quality deviations and IP exposure.

Miscommunication and Specification Gaps

Language barriers and technical misunderstandings can lead to incorrect interpretations of drawings, finishes, or tolerances. For example, metric vs. imperial units, ambiguous surface finish codes, or undefined critical dimensions may result in non-conforming products. Without clear, detailed, and technically reviewed specifications—and ideally, physical prototypes—buyers risk receiving products that don’t meet functional or aesthetic requirements.

Lack of Traceability and Certification

Reliable documentation such as material test reports (MTRs), mill certificates, or compliance certifications (e.g., ISO 9001, CE, AAMA) may be incomplete, falsified, or unavailable. This lack of traceability makes it difficult to verify alloy composition, heat treatment processes, or adherence to industry standards—especially important for structural or safety-critical applications.

How to Mitigate These Risks

To avoid these pitfalls, buyers should conduct thorough due diligence: verify supplier credentials, perform factory audits, request sample batches, and use third-party inspection services (e.g., SGS, BV). Legal safeguards—such as registered IP in China, legally binding contracts with clear IP clauses, and jurisdictional agreements—are essential. Building long-term relationships with trustworthy partners and investing in clear communication and technical alignment can significantly reduce both quality and IP risks.

Logistics & Compliance Guide for Aluminium Profile in China

Understanding the logistics and compliance landscape is crucial when importing, exporting, or distributing aluminium profiles within or from China. This guide outlines key regulations, documentation, transportation considerations, and quality standards specific to this sector.

Import/Export Regulations and Documentation

Aluminium profiles are subject to standard international trade controls in China. Exporters must ensure compliance with both Chinese export regulations and the import requirements of the destination country. Key documentation includes a commercial invoice, packing list, bill of lading or air waybill, and a certificate of origin. For certain markets, additional certifications such as a Certificate of Conformity (CoC) or test reports from accredited labs may be required. Exporters should also be aware of any anti-dumping duties or trade remedies imposed by importing countries on Chinese aluminium products.

Customs Clearance and Tariff Classification

Accurate tariff classification under the Harmonized System (HS Code) is essential for customs clearance. Aluminium profiles typically fall under HS Code 7604.21 (alloy aluminium) or 7604.29 (non-alloy aluminium), depending on composition. Misclassification can lead to delays, fines, or incorrect duty payments. Importers must declare the correct value, quantity, and specifications. Customs authorities may inspect shipments, particularly for high-value consignments or if documentation is incomplete. Pre-shipment verification and use of licensed customs brokers are recommended to streamline clearance.

Quality Standards and Product Certification

Aluminium profiles manufactured or sold in China must comply with national standards (GB standards), such as GB/T 5237 for architectural aluminium alloy profiles. These standards cover mechanical properties, dimensional tolerances, surface treatment (e.g., anodizing, powder coating), and chemical composition. Exporters targeting international markets may also need to meet standards like EN (Europe), ASTM (USA), or JIS (Japan). Third-party testing and certification (e.g., ISO 9001, CE marking where applicable) enhance market acceptance and demonstrate compliance.

Transportation and Handling Considerations

Due to their length and susceptibility to scratching or bending, aluminium profiles require careful packaging and handling. They are typically bundled and protected with corner guards, plastic film, or wooden crates. For domestic transport in China, road freight via specialized carriers is common. For international shipping, containerized ocean freight (FCL or LCL) is standard. Proper lashing and blocking in containers prevent shifting during transit. Air freight may be used for urgent, high-value, or sample shipments.

Environmental and Safety Compliance

Manufacturers and exporters must adhere to China’s environmental regulations, particularly concerning emissions, waste management, and energy consumption in production facilities. Surface treatment processes (e.g., anodizing, coating) must comply with local environmental protection bureau (EPB) requirements. Safety data sheets (SDS) should be available for coated or chemically treated profiles. Compliance with REACH (EU) or other chemical regulations may be needed for exports to regulated markets.

Incoterms and Contractual Clarity

Clearly defining responsibilities using internationally recognized Incoterms (e.g., FOB, CIF, DDP) is critical in contracts involving aluminium profiles. This determines who handles logistics, insurance, customs clearance, and risk transfer. Misunderstandings can lead to cost overruns or delivery disputes. It is advisable to work with experienced freight forwarders and legal counsel when drafting international supply agreements.

Intellectual Property and Labeling Requirements

Ensure that product designs and trademarks do not infringe on existing patents or intellectual property rights in China or the destination market. Proper labeling, including product specifications, manufacturer details, batch numbers, and compliance marks (e.g., GB, CE), is required for traceability and regulatory compliance. Bilingual labeling (Chinese and English) is recommended for export shipments.

By adhering to these logistics and compliance guidelines, businesses can efficiently manage the movement of aluminium profiles through China’s supply chain while minimizing risks and ensuring regulatory adherence.

In conclusion, sourcing aluminum profile manufacturers in China offers a compelling combination of cost efficiency, extensive production capabilities, and technological expertise. China’s well-developed aluminum industry, supported by a robust supply chain and advanced extrusion technologies, enables reliable mass production and custom solutions for diverse applications across industries such as construction, electronics, automotive, and renewable energy.

However, successful sourcing requires careful due diligence to ensure quality, compliance, and reliability. Buyers should prioritize manufacturers with relevant certifications (such as ISO 9001, ISO 14001, and CE), proven experience in international exports, and strong communication capabilities. Utilizing sourcing platforms, attending trade fairs like the Canton Fair, and engaging third-party inspection services can further mitigate risks and enhance transparency.

Ultimately, building long-term relationships with reputable Chinese aluminum profile manufacturers can lead to sustainable cost savings, timely delivery, and consistent product quality—making China a strategic sourcing destination for global procurement needs.