The Chinese automotive industry has emerged as a global powerhouse, driven by rapid technological advancement, robust domestic demand, and strong government support for new energy vehicles (NEVs). According to Mordor Intelligence, the China automotive market was valued at approximately USD 590 billion in 2023 and is projected to grow at a CAGR of over 5.8% from 2024 to 2030. This expansion is further fueled by the country’s dominance in electric vehicle (EV) production, which accounted for over 60% of global EV sales in 2023, as reported by Grand View Research. With policies promoting sustainable transportation and significant investments in intelligent manufacturing, China is home to a new generation of automobile manufacturers that blend innovation, scale, and cost-efficiency. The following list highlights the top nine automotive manufacturers in China shaping the future of mobility, both domestically and internationally, based on market share, production volume, export performance, and technological leadership.

Top 9 Automobile And Of China Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Automobile And Of China

2026 Market Trends for the Automobile Industry in China

By 2026, China’s automobile market is poised to solidify its position as the world’s most influential and advanced automotive landscape, driven by technological innovation, evolving consumer preferences, and robust government support. Several key trends will define the industry’s trajectory:

Electrification Dominance and BEV Maturity

China’s leadership in electric vehicles (EVs) will deepen, with Battery Electric Vehicles (BEVs) becoming the core of new car sales. By 2026, BEVs are projected to account for over 40% of total passenger vehicle sales, driven by improved battery technology, expanded charging infrastructure, and aggressive pricing from domestic manufacturers. The market will shift from early adoption to mass-market maturity, with increased competition leading to consolidation among EV startups and heightened focus on profitability and lifecycle cost efficiency.

Rise of Intelligent and Connected Vehicles (ICVs)

Intelligent and Connected Vehicle technology will transition from a differentiator to a baseline expectation. Advanced Driver Assistance Systems (ADAS) will be standard on mid-to-high-end models, with significant progress toward Level 3 conditional automation in premium offerings. Chinese tech giants and automakers will intensify integration of AI-driven infotainment, over-the-air (OTA) updates, and V2X (vehicle-to-everything) communication, enhancing safety, convenience, and user experience. The ecosystem around smart cockpits and autonomous driving software will become a critical battleground.

Domestic Brands Accelerate Global Expansion

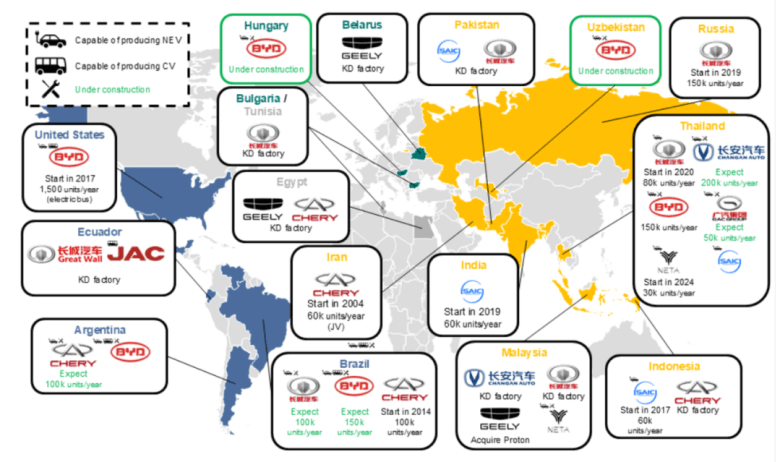

Chinese automakers such as BYD, Geely, NIO, XPeng, and Great Wall will continue their aggressive international expansion. Europe, Southeast Asia, the Middle East, and Latin America will be key targets. These brands will leverage cost advantages, technological innovation (especially in EVs and software), and strategic partnerships to capture market share. By 2026, Chinese brands are expected to account for over 15% of global EV exports, challenging traditional European and Japanese OEMs.

Supply Chain Resilience and Localization

In response to geopolitical tensions and trade barriers, Chinese automakers will prioritize supply chain localization and diversification. Investments in domestic semiconductor production, battery raw material sourcing (including lithium and cobalt through overseas partnerships), and software development will accelerate. The push for self-reliance will strengthen China’s position in critical components while fostering innovation in next-generation technologies like solid-state batteries.

Regulatory and Policy Support

Government policies will continue to shape the market. While direct subsidies for EV purchases may taper, non-financial incentives such as preferential license plate allocation in major cities, infrastructure investment, and supportive regulations for autonomous driving testing will persist. Stricter emissions standards and fuel efficiency requirements will further incentivize electrification. Additionally, national strategies around smart city integration and digital economy will bolster the development of connected vehicle ecosystems.

Shift in Consumer Behavior

Urban Chinese consumers will increasingly prioritize digital experiences, sustainability, and brand values. Subscription models, flexible ownership, and shared mobility services will gain traction, especially among younger demographics. Demand for personalized, software-upgradable vehicles will grow, reinforcing the importance of direct-to-consumer sales models and robust digital platforms.

Challenges and Competitive Pressures

Despite growth, the market will face challenges including overcapacity, price wars among EV manufacturers, and rising scrutiny from international regulators on trade practices and data security. Profitability will remain a key concern as companies balance innovation investment with cost control. Cybersecurity and data privacy regulations will also tighten, impacting how vehicle data is collected and used.

In conclusion, by 2026, China’s automobile industry will be characterized by a fully electrified, highly connected, and globally competitive landscape. Innovation in EVs, intelligent systems, and business models will define market leaders, while domestic champions extend their influence beyond borders, reshaping the global automotive order.

Common Pitfalls Sourcing Automobiles from China: Quality and Intellectual Property Risks

Sourcing automobiles from China can offer cost advantages and access to innovative technologies. However, businesses must navigate several critical pitfalls, particularly concerning quality control and intellectual property (IP) protection. Understanding these risks is essential for mitigating potential losses and ensuring long-term success.

Quality Control Challenges

One of the most significant concerns when sourcing vehicles from China is maintaining consistent quality standards. Chinese automotive manufacturers vary widely in production capabilities, and without stringent oversight, subpar products can reach the market.

-

Inconsistent Manufacturing Standards: Not all Chinese manufacturers adhere to international quality benchmarks such as ISO/TS 16949. Differences in production processes, material sourcing, and worker training can result in inconsistent build quality and reliability issues.

-

Lack of Transparency in Supply Chains: Many suppliers use third- or even fourth-tier sub-suppliers for components, making it difficult to trace the origin and quality of critical parts like batteries, electronics, or safety systems.

-

Insufficient Testing and Certification: Some exporters may not conduct comprehensive durability, safety, or emissions testing required in target markets. Vehicles might meet Chinese domestic standards but fail to comply with EU, U.S., or other regional regulations.

-

Language and Communication Barriers: Miscommunication due to language differences can lead to misunderstandings about specifications, tolerances, and performance requirements, potentially resulting in defective or non-compliant vehicles.

Intellectual Property Risks

Protecting intellectual property when sourcing from China is a major challenge, especially in the automotive industry where design, technology, and branding are crucial.

-

Design and Technology Copying: Chinese suppliers may reverse-engineer designs or use proprietary technology without authorization. There have been documented cases where prototypes or technical data provided for manufacturing were later used to produce competing products.

-

Weak Enforcement of IP Rights: While China has improved its IP laws, enforcement remains inconsistent. Legal recourse can be slow, costly, and difficult, especially for foreign companies unfamiliar with local regulations and judicial practices.

-

Unauthorized Production and Grey Market Sales: Suppliers may exceed agreed production volumes and sell excess units through unofficial channels, diluting brand value and undermining market pricing strategies.

-

Lack of Confidentiality Agreements and Safeguards: Many sourcing agreements lack robust confidentiality clauses or fail to specify ownership of designs, software, or innovations developed during collaboration, leaving companies vulnerable to IP theft.

Mitigation Strategies

To address these pitfalls, companies should implement rigorous due diligence, establish clear contractual protections, and engage third-party inspection and legal experts. Conducting factory audits, requiring certifications, using secure technical documentation protocols, and registering IP in China are essential steps to reduce exposure to quality and IP risks.

Logistics & Compliance Guide for Automobiles in China

China’s automotive market is one of the largest and most complex in the world, with stringent regulations, evolving standards, and a vast logistics network. To successfully import, export, manufacture, or distribute automobiles in China, businesses must navigate a multifaceted regulatory environment and optimize their supply chain operations. This guide provides an overview of key logistics and compliance considerations.

Regulatory Framework and Compliance

National Development and Reform Commission (NDRC) and MIIT Oversight

The NDRC and the Ministry of Industry and Information Technology (MIIT) regulate the automotive industry in China. The NDRC approves investment projects and manufacturing capacity, while MIIT manages vehicle type approvals and production qualifications. All automakers—domestic and foreign—must obtain production licenses and meet industrial policy requirements.

Vehicle Type Approval (VTA)

All vehicles sold or imported into China must pass Vehicle Type Approval, which involves comprehensive testing for safety, emissions, noise, and fuel consumption. The China Compulsory Certification (CCC) mark is mandatory and administered by the Certification and Accreditation Administration of China (CNCA). Without CCC certification, vehicles cannot be registered or legally driven.

Emission Standards

China has adopted China VI emission standards (equivalent to Euro 6), which apply to light-duty and heavy-duty vehicles. These standards regulate nitrogen oxides (NOx), particulate matter (PM), and other pollutants. Importers must ensure vehicles meet the applicable emission level for the region of entry.

Cybersecurity and Data Compliance

For connected and electric vehicles (EVs), compliance with China’s Cybersecurity Law, Data Security Law, and Personal Information Protection Law (PIPL) is critical. Automakers must store Chinese user data locally and undergo security assessments if transferring data abroad. The MIIT also requires reporting on software updates and over-the-air (OTA) functions.

Import and Export Procedures

Import Licensing and Tariffs

Automobiles imported into China are subject to several taxes:

– Import Duty: Ranges from 15% (passenger vehicles) to 25% (some commercial vehicles).

– Value-Added Tax (VAT): 13% on the sum of CIF value, duty, and consumption tax.

– Consumption Tax: Applies to vehicles based on engine displacement (ranging from 1% to 40%).

Electric vehicles (EVs) often benefit from lower or zero consumption tax, promoting green mobility.

Special Economic Zones and Free Trade Ports

China operates several Free Trade Zones (FTZs), such as Shanghai’s Lingang and Hainan Free Trade Port, which offer simplified customs procedures, tax incentives, and faster CCC certification processing. Using FTZs can significantly reduce time-to-market for imported vehicles.

Export Controls and Dual-Use Items

Components involving advanced technologies (e.g., autonomous driving systems, high-performance batteries) may be subject to export controls under China’s Dual-Use Items and Technologies Export Control Regulations. Exporters must screen items and obtain licenses when required.

Logistics Infrastructure and Supply Chain Management

Port and Inland Transportation Network

China has world-class port infrastructure, including Shanghai, Ningbo-Zhoushan, and Shenzhen. Roll-on/roll-off (RoRo) terminals are available for vehicle shipment. Post-port, vehicles are transported via rail, road, or inland waterways to distribution centers.

Automakers often use bonded logistics parks to defer duties and streamline distribution.

Warehousing and Distribution

Automotive distributors utilize regional distribution centers (RDCs) near major cities. Cold chain and hazardous materials logistics apply to EV battery transport, requiring compliance with GB standards for lithium-ion battery handling.

Just-in-Time (JIT) and Supplier Integration

Domestic and joint-venture manufacturers (e.g., SAIC-GM, FAW-Volkswagen) operate JIT systems that rely on tightly coordinated supplier networks. Foreign suppliers must integrate into local supply chains, often establishing local warehouses or partner with third-party logistics (3PL) providers.

Electric Vehicle (EV) Specific Considerations

Battery Regulations and Recycling

China enforces strict regulations on EV battery production, traceability, and recycling under the “Automotive Power Battery Recycling and Utilization Management Plan.” Battery producers must register with the MIIT and ensure end-of-life recycling.

Charging Infrastructure Compliance

EVs and charging equipment must meet GB/T standards for connectors, communication protocols, and safety. Non-compliant charging systems cannot be sold or installed.

After-Sales and Recall Compliance

Mandatory Recall System

The State Administration for Market Regulation (SAMR) oversees vehicle recalls. Manufacturers must establish monitoring systems for defects and report safety issues promptly. Failure to comply may result in fines, production suspension, or market exclusion.

Warranty and Service Requirements

Foreign automakers must provide parts and service networks that meet local consumer protection laws. Extended warranties and customer service in Mandarin are often expected for market competitiveness.

Conclusion

Operating in China’s automotive sector demands in-depth understanding of logistics networks and regulatory compliance. From securing type approvals and managing customs duties to ensuring data localization and environmental standards, businesses must adopt a holistic strategy. Partnering with local experts, leveraging FTZs, and staying current with policy updates are essential for long-term success in China’s dynamic automotive market.

Conclusion: Sourcing Automobile Manufacturers and Brands from China

Sourcing automobile manufacturers and brands from China presents a strategic opportunity for global businesses seeking cost-effective, innovative, and increasingly high-quality vehicles and automotive components. Over the past two decades, China has transformed into the world’s largest automotive market and a leading manufacturing hub, driven by strong government support, rapid technological advancements, and a growing domestic demand for new energy vehicles (NEVs).

Chinese automakers such as BYD, Geely, SAIC Motor, NIO, Xpeng, and Great Wall Motors have made significant strides in electric vehicle (EV) technology, autonomous driving, and smart mobility solutions. Their competitive pricing, coupled with improving reliability and design, makes them attractive partners for international markets. Additionally, joint ventures between Chinese and foreign automakers, as well as acquisitions like Geely’s ownership of Volvo and Lotus, highlight China’s expanding influence in the global automotive industry.

However, challenges such as regulatory compliance, intellectual property concerns, quality control variability, and geopolitical factors must be carefully managed. Due diligence, strategic partnerships, and a deep understanding of local market dynamics are essential when sourcing from Chinese manufacturers.

In conclusion, China’s robust automotive ecosystem, innovation in green technologies, and scalable production capabilities position it as a key player in the future of global mobility. For companies looking to diversify supply chains, reduce costs, or enter the EV market, sourcing from Chinese automobile manufacturers offers compelling advantages—provided it is approached with informed strategy and long-term vision.