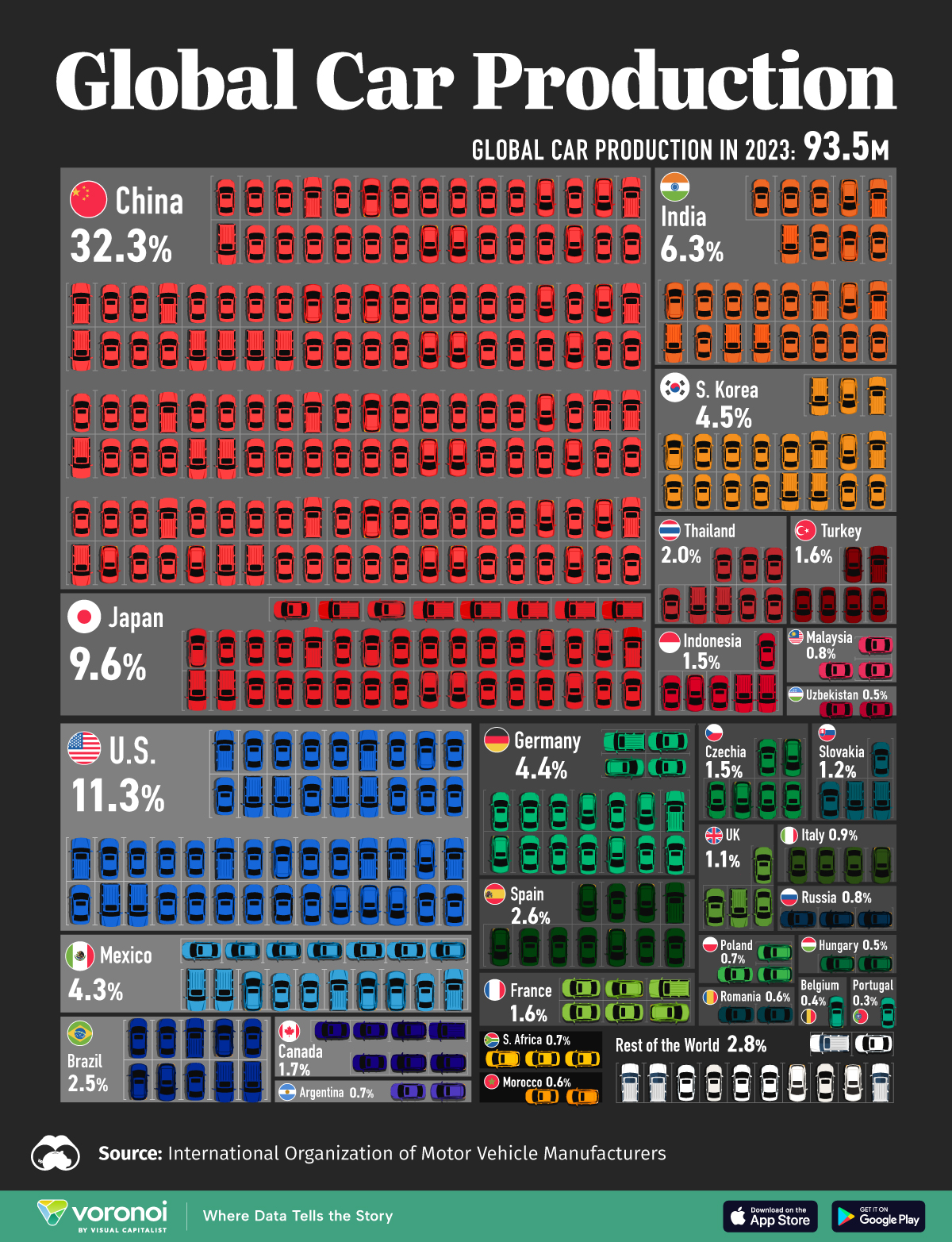

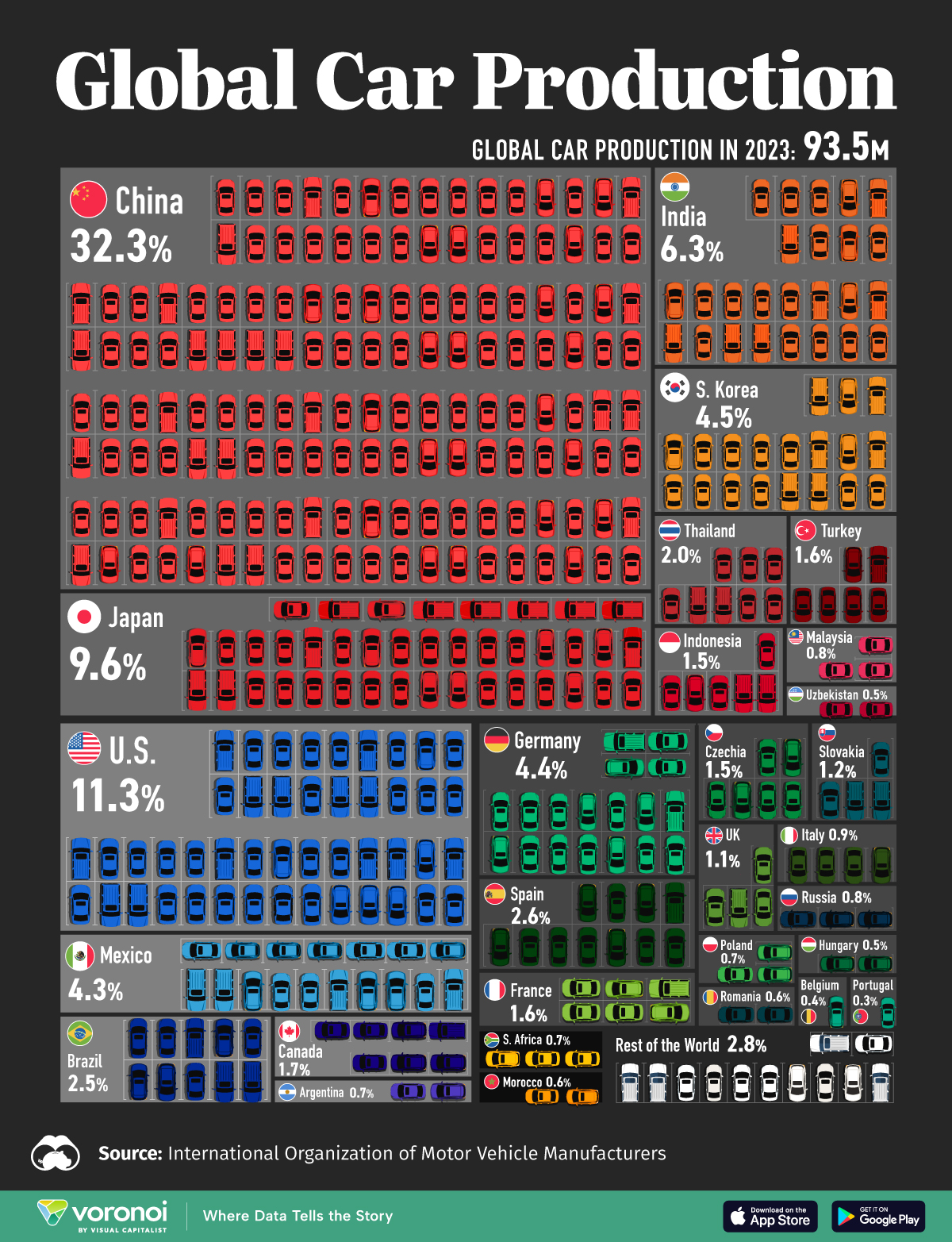

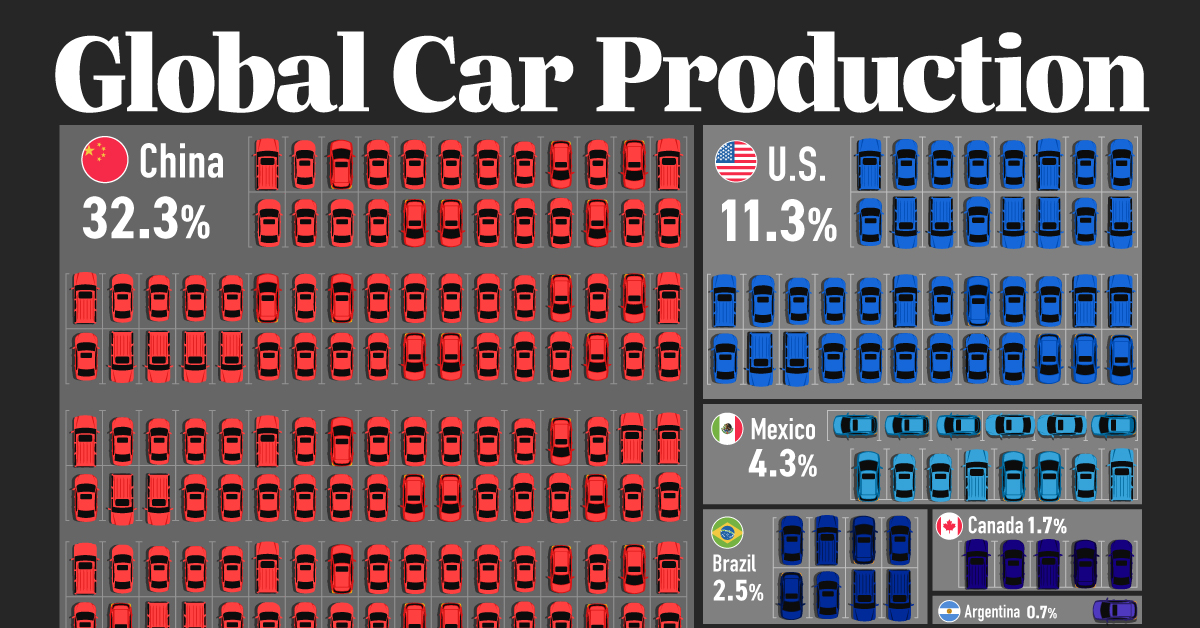

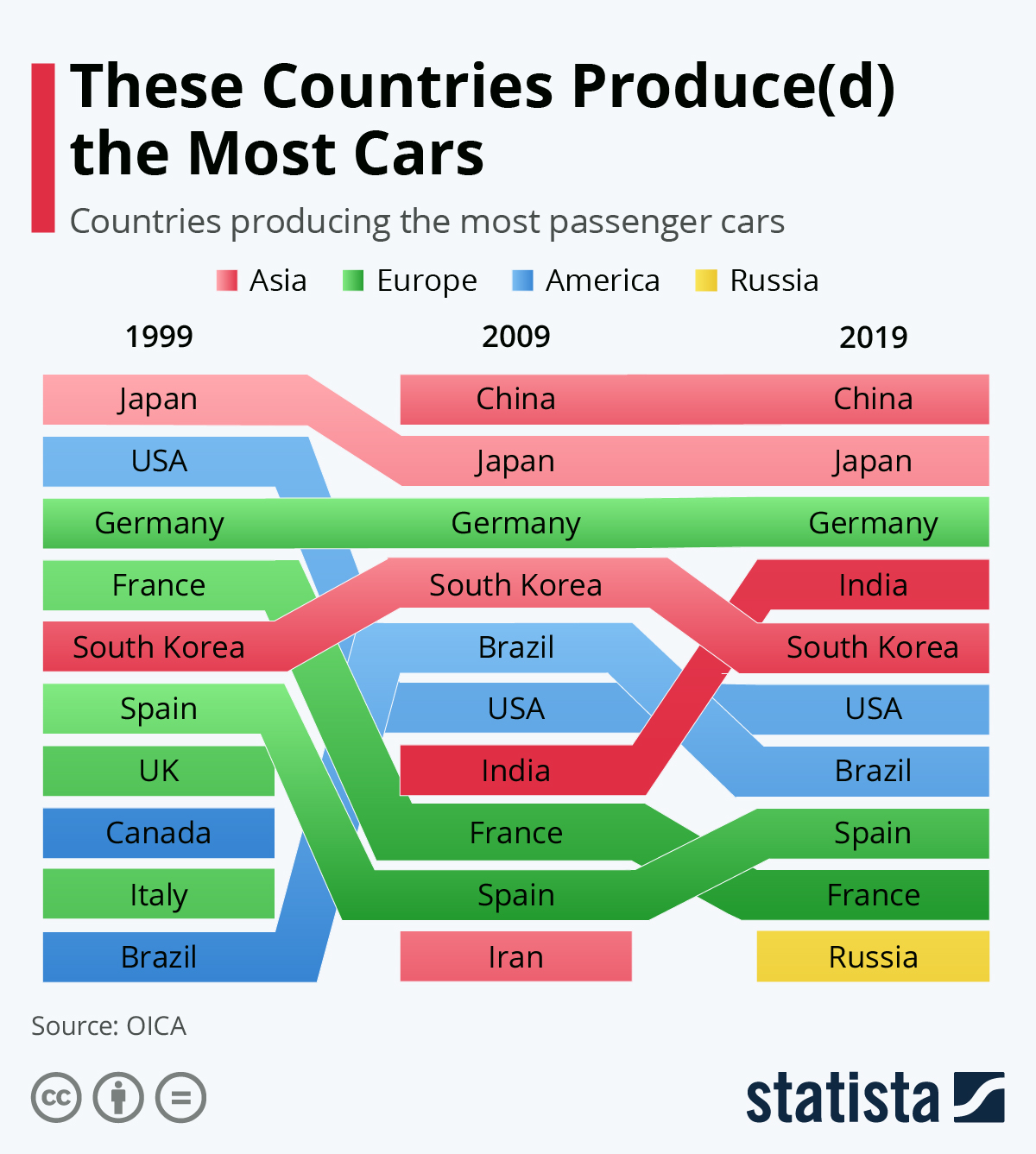

The global automotive manufacturing industry continues to expand, driven by technological innovation, increasing demand for electric vehicles (EVs), and evolving consumer preferences. According to Mordor Intelligence, the global automotive market was valued at approximately USD 3.5 trillion in 2023 and is projected to grow at a CAGR of over 4.8% from 2024 to 2029. This growth is underpinned by regional manufacturing strengths, supply chain advancements, and government policies promoting sustainable mobility. As the industry becomes more decentralized, with key players emerging across diverse geographies, understanding the leading automobile manufacturers by country provides critical insights into market dynamics, production capabilities, and innovation leadership. Drawing on data from Mordor Intelligence and Grand View Research—whose reports highlight Asia Pacific’s dominance due to China and India’s expanding production bases—this overview identifies the top seven automobile manufacturers by country, reflecting both historical influence and future trajectory in a rapidly transforming sector.

Top 7 Automobile By Country Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Automobile By Country

2026 Market Trends for Automobile by Country

United States

The U.S. automotive market in 2026 is projected to experience sustained growth in electric vehicle (EV) adoption, driven by federal incentives, expanding charging infrastructure, and increasing consumer demand. Automakers like Ford, GM, and Tesla continue to expand their EV lineups, with GM aiming for an all-electric light-duty fleet by 2035. The Biden administration’s updated fuel efficiency standards and Clean Air Act regulations are accelerating the shift toward zero-emission vehicles. Additionally, advancements in battery technology and lower production costs are expected to make EVs more affordable. Autonomous driving features are becoming more prevalent, with Level 2+ driver assistance systems now standard in many new models. However, challenges remain, including supply chain constraints for critical minerals and semiconductor shortages.

China

China remains the world’s largest automotive market, and by 2026, it will continue to lead in EV production and consumption. Domestic brands such as BYD, NIO, Xpeng, and Li Auto are outpacing legacy automakers in innovation and market share. The Chinese government’s strong policy support—through subsidies, license plate incentives in major cities, and strict emissions regulations—fuels EV dominance. By 2026, over 40% of new car sales in China are expected to be fully electric. The country is also advancing in smart mobility, with integrated 5G connectivity, vehicle-to-everything (V2X) communication, and autonomous driving pilots in cities like Shanghai and Shenzhen. However, intense competition is pressuring profit margins, and regulatory scrutiny on data security and foreign tech partnerships adds complexity for international players.

Germany

As the heart of Europe’s automotive industry, Germany in 2026 is undergoing a transformational shift toward electrification. Traditional OEMs like Volkswagen, Mercedes-Benz, and BMW are accelerating their EV rollouts, with VW investing heavily in its ID series and battery gigafactories. The German government continues to support EV adoption through purchase incentives and tax benefits, although these are expected to taper as market maturity grows. Challenges include adapting the workforce for EV manufacturing and navigating EU emissions regulations. Hydrogen fuel cell vehicles are also gaining attention, particularly for commercial transport. Meanwhile, autonomous driving remains limited to pilot programs due to stringent safety and legal frameworks.

Japan

Japan’s automotive market in 2026 reflects a cautious but steady transition to electrification. While Toyota, Honda, and Nissan are expanding their EV offerings, the country maintains a strong focus on hybrid vehicles, which still dominate sales. The government’s “Green Growth Strategy” targets carbon neutrality by 2050, pushing automakers to innovate in battery tech and hydrogen fuel cells. Toyota’s investment in solid-state batteries could position Japan as a leader in next-gen energy storage. However, consumer preference for smaller, fuel-efficient cars and limited charging infrastructure slow full EV adoption. Japan also remains a key exporter, with growing demand for its vehicles in Southeast Asia and Africa.

India

India’s automotive sector is poised for rapid transformation by 2026, fueled by rising urbanization, government initiatives like the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme, and increasing disposable incomes. Two- and three-wheelers lead the EV revolution, but passenger EVs are gaining momentum, with Tata Motors dominating the segment. Global brands like Hyundai and MG Motor are also launching affordable EV models tailored to Indian consumers. The government aims for 30% electric passenger vehicle sales by 2030, and progress is accelerating through charging infrastructure development and local battery manufacturing. Challenges include high upfront costs and power grid reliability, but policy support and falling battery prices are expected to drive adoption.

South Korea

South Korea’s automotive market in 2026 is characterized by strong domestic EV production and technological innovation. Hyundai and Kia are leading the charge with globally competitive EVs like the Ioniq 5 and EV6, which receive acclaim for design and range. The government supports the transition with subsidies, tax breaks, and investments in charging networks. South Korea is also advancing in autonomous driving, with pilot projects in smart cities like Songdo. The country is positioning itself as a key supplier of EV components, including batteries from companies like LG Energy Solution and Samsung SDI. Exports remain vital, particularly to North America and Europe.

United Kingdom

In 2026, the UK automotive market continues its push toward a 2030 ban on new internal combustion engine (ICE) vehicle sales. EV adoption is rising, supported by government grants, expanded charging infrastructure, and consumer awareness. British brands like Jaguar are going fully electric, while Nissan’s Sunderland plant remains a key EV manufacturing hub. However, economic uncertainty and inflation are affecting consumer spending. The UK also faces challenges in securing battery supply chains and maintaining competitiveness post-Brexit. Autonomous vehicle testing is ongoing, particularly in cities like London and Coventry, but regulatory hurdles delay widespread deployment.

France

France’s automotive landscape in 2026 is shaped by strong state involvement and environmental policy. The government offers substantial EV incentives, including the “bonus écologique,” and supports domestic manufacturers like Stellantis (Peugeot, Citroën, Renault). Renault, in particular, is focusing on affordable EVs like the Renault 5 EV to capture mass-market demand. France is investing in battery gigafactories and promoting circular economy practices in vehicle production. Urban mobility solutions, such as electric scooters and car-sharing, are expanding in cities like Paris. However, high energy costs and labor market tensions pose risks to sustained growth.

Brazil

By 2026, Brazil’s automotive market shows growing interest in flex-fuel and electric vehicles. While internal combustion engines still dominate, especially those running on ethanol, EV adoption is increasing in urban centers like São Paulo and Rio de Janeiro. The government has introduced tax incentives for EVs, and automakers such as Fiat, Toyota, and local startup Grupo Caoa are launching electric models. China-based EV makers like BYD and NIO are also entering the Brazilian market. Infrastructure development remains a bottleneck, but public-private partnerships are expanding charging networks. The long-term potential is significant, driven by Brazil’s vast renewable energy capacity.

Canada

Canada’s automotive market in 2026 is aligning closely with U.S. trends due to integrated supply chains and shared regulations. Federal and provincial incentives are boosting EV adoption, with targets for 100% zero-emission vehicle sales by 2035. Ontario remains a key manufacturing center, with investments in EV production from Ford, GM, and Stellantis. Canada is also leveraging its abundant natural resources—lithium, nickel, and cobalt—to build a domestic battery supply chain. Challenges include regional disparities in charging infrastructure and colder climate impacts on battery performance. Nonetheless, consumer interest in EVs continues to grow, supported by environmental awareness and improving vehicle range.

In summary, the global automotive market in 2026 is defined by a convergence toward electrification, digitalization, and sustainability, with regional variations shaped by policy, consumer behavior, and industrial capacity. While developed nations lead in EV adoption and technology, emerging markets are catching up rapidly, driven by innovation and strategic government support.

Common Pitfalls Sourcing Automobiles by Country: Quality and Intellectual Property Concerns

Sourcing automobiles from different countries offers opportunities for cost savings and access to innovative technologies. However, businesses often encounter significant challenges related to quality control and intellectual property (IP) protection. Below are some common pitfalls to watch for when sourcing automobiles by country.

1. Inconsistent Quality Standards Across Regions

Automobile quality can vary significantly depending on the manufacturing country due to differences in regulatory standards, production practices, and oversight. For example:

- Emerging Markets: Countries with rapidly growing auto industries may lack stringent quality control systems, leading to inconsistent build quality, substandard materials, or premature component failure.

- Regulatory Gaps: Some nations enforce less rigorous safety and emissions standards than regions like the EU or North America, which can result in vehicles unsuitable for export markets.

- After-Sales Support: Poor availability of spare parts and service networks in certain countries can compromise long-term vehicle reliability.

2. Misrepresentation of Vehicle Specifications

Suppliers may exaggerate performance metrics, fuel efficiency, or safety ratings to appeal to international buyers. This is particularly common when sourcing from countries with limited third-party verification or lax advertising regulations.

- Independent testing and certification (e.g., Euro NCAP, NHTSA) should be required before finalizing procurement.

- Conducting factory audits and requesting detailed technical documentation can help verify claims.

3. Intellectual Property Infringement Risks

Sourcing from certain countries increases exposure to IP violations, such as:

- Design and Technology Copying: Some manufacturers replicate patented designs, software systems, or engine technologies without authorization—common in regions with weak IP enforcement.

- Counterfeit Parts: Use of unlicensed or cloned components (e.g., ECUs, sensors, infotainment systems) can void warranties and create legal liabilities.

- Software and Firmware Issues: Embedded software in modern vehicles may infringe on copyrights or lack proper licensing, especially in countries with limited digital IP governance.

4. Lack of Transparency in Supply Chains

Complex, multi-tiered supply chains in countries like China, India, or Turkey can obscure the origin of components. Hidden subcontractors may source parts from unauthorized or non-compliant vendors, increasing exposure to quality defects and IP risks.

- Implement supply chain mapping and traceability systems.

- Require suppliers to disclose sub-tier vendors and certifications.

5. Weak Legal Recourse in Case of Disputes

In some countries, legal systems offer limited protection for foreign buyers. Enforcing contracts, recalling defective vehicles, or litigating IP theft can be costly and time-consuming.

- Use international arbitration clauses in contracts.

- Partner with local legal counsel familiar with automotive regulations and dispute resolution.

6. Non-Compliance with Export Regulations

Vehicles compliant in the country of origin may not meet the import standards of the destination market (e.g., U.S. DOT, EU Whole Vehicle Type Approval). This can lead to customs delays, fines, or rejected shipments.

- Verify conformity with target market regulations before sourcing.

- Work with certification bodies to pre-validate compliance.

Conclusion

To mitigate risks when sourcing automobiles by country, businesses must conduct thorough due diligence, prioritize suppliers with strong compliance records, and implement robust quality assurance and IP protection protocols. Engaging third-party inspectors, securing legal protections, and staying informed about regional regulatory environments are essential steps in avoiding these common pitfalls.

Logistics & Compliance Guide for Automobiles by Country

United States

Logistics Overview:

The U.S. has a well-developed automotive logistics network, including major vehicle processing ports (e.g., Baltimore, Brunswick, and Los Angeles), inland rail and trucking systems, and distribution centers. Just-in-time (JIT) delivery is common among manufacturers and dealerships.

Regulatory Compliance:

– NHTSA (National Highway Traffic Safety Administration): Enforces Federal Motor Vehicle Safety Standards (FMVSS). All new vehicles and major modifications must comply.

– EPA (Environmental Protection Agency): Regulates emissions standards and fuel economy (Corporate Average Fuel Economy – CAFE).

– DOT (Department of Transportation): Oversees vehicle identification numbers (VINs) and import certification.

– Import Requirements: Vehicles must meet FMVSS and EPA standards. Non-conforming vehicles may be imported under a “show or display” exemption or modified by an Independent Commercial Importer (ICI).

– Customs: CBP (Customs and Border Protection) requires entry documentation, including EPA Form 3520-1 and DOT Form HS-7.

Key Considerations:

– Right-hand drive (RHD) vehicles face significant restrictions unless for specific exemptions.

– Used vehicle imports subject to 25-year rule (generally cannot import vehicles under 25 years old not originally certified for U.S. market).

– State-level regulations (e.g., California’s CARB standards) may be stricter than federal rules.

Germany

Logistics Overview:

Germany is a central logistics hub in Europe with excellent road, rail, and inland waterway networks. Major automotive manufacturing centers (e.g., Wolfsburg, Stuttgart) are well-connected to European distribution routes.

Regulatory Compliance:

– KBA (Kraftfahrt-Bundesamt): Federal Motor Transport Authority responsible for vehicle type approval, registration, and roadworthiness.

– Type Approval: Vehicles must have EU Whole Vehicle Type Approval ( WVTA) under EU Directive 2007/46/EC.

– Emissions Standards: Must comply with Euro 6/7 standards.

– Import Requirements: For non-EU vehicles, national type approval may be required. Used vehicle imports need inspection (e.g., TÜV or DEKRA certification).

– CO₂ Taxation: Company cars are subject to taxation based on CO₂ emissions.

– Customs: For non-EU imports, duties and VAT apply. Intra-EU trade is duty-free.

Key Considerations:

– Strict roadworthiness testing (Hauptuntersuchung) every 2 years after first registration.

– Environmental zones (Umweltzonen) in major cities require vehicles to display an emissions sticker (Feinstaubplakette).

– Right-hand drive vehicles permitted but not common; may require special registration.

China

Logistics Overview:

Automotive logistics in China is rapidly modernizing, with key ports like Shanghai and Tianjin serving as major import hubs. Rail (including China-Europe rail links) and domestic trucking networks support distribution, though regional disparities exist.

Regulatory Compliance:

– MIIT (Ministry of Industry and Information Technology): Administers the CCC (China Compulsory Certification) mark required for all vehicles sold in China.

– Ecological Environment Ministry: Enforces China 6 (equivalent to Euro 6) emissions standards.

– Customs & Import: Vehicles imported as complete units (CBU) face high tariffs (typically 15%–25%) and VAT (13%). Luxury vehicles may incur additional consumption tax (up to 40%).

– Type Approval: Requires CCC certification, including testing for safety, emissions, and EMC.

– Local Production Incentives: Policies favor domestic or joint-venture manufacturing (e.g., NEV mandates).

Key Considerations:

– Electric vehicles (EVs) are strongly incentivized; foreign brands may need local partnerships for full market access.

– Left-hand drive standard; right-hand drive vehicles generally not permitted for civilian use.

– Complex regional registration quotas in major cities (e.g., Shanghai license plate auctions).

Japan

Logistics Overview:

Japan features a dense, efficient logistics system, with major ports like Yokohama and Kobe handling vehicle exports and limited imports. Domestic distribution relies heavily on rail and specialized car carriers.

Regulatory Compliance:

– MLIT (Ministry of Land, Infrastructure, Transport and Tourism): Oversees vehicle safety and road regulations.

– Type Approval: Vehicles must pass Shaken (automotive inspection) and meet Japanese Industrial Standards (JIS).

– Emissions: Comply with Japanese under JC08 or WLTC test cycles; strict particulate and NOx limits.

– Import Requirements: Used vehicle exports are common, but imports into Japan require inspection and modification to meet Japanese standards (e.g., speedometer in km/h, headlights adjusted).

– Customs: Duties apply (e.g., 4.7% for passenger vehicles), plus consumption tax (10%).

Key Considerations:

– Shaken inspection every 2 years; costly and comprehensive (safety, emissions, weight).

– Right-hand drive standard; left-hand drive vehicles require special approval and are rarely registered.

– Used car importers often modify imported vehicles (e.g., VIN translation, lighting) to pass inspection.

Brazil

Logistics Overview:

Logistics infrastructure is improving, but challenges remain with road conditions and port efficiency. Automotive manufacturing clusters in São Paulo and Paraná are linked via federal highways and railways.

Regulatory Compliance:

– INMETRO: Responsible for vehicle safety and conformity assessment (Portaria 409/2021).

– CONPET: Sets fuel efficiency and labeling requirements.

– IBAMA (Environmental Agency): Enforces PROCONVE emissions standards (equivalent to Euro 5/6).

– ANFAVEA: Industry association that supports compliance and standards adoption.

– Import Duties: High tariffs (35% under Mercosur rules); additional Tax on Industrialized Products (IPI) and state-level ICMS taxes apply.

Key Considerations:

– National Vehicle Labeling Program (etiqueta) discloses fuel consumption and CO₂ emissions.

– Right-hand drive vehicles prohibited except for specific government or diplomatic use.

– Local content rules incentivize domestic production; foreign-assembled vehicles face higher costs.

India

Logistics Overview:

India’s automotive logistics network is expanding rapidly, with key manufacturing zones in Pune, Chennai, and Gurgaon. Multi-modal transport (road, rail, and coastal shipping) supports distribution, though congestion can delay delivery.

Regulatory Compliance:

– Ministry of Road Transport and Highways (MoRTH): Enforces safety standards under CMVR (Central Motor Vehicle Rules).

– Bharat Stage Emission Standards (BS-VI): Equivalent to Euro 6; mandatory since April 2020.

– Type Approval: Required under CMVR; testing at ARAI or other government-approved labs.

– Customs & Import: CBU imports face high duties (60%–100%); kits (CKD/SKD) attract lower rates to promote local assembly.

– FAME India Scheme: Incentivizes electric vehicle adoption and local manufacturing.

Key Considerations:

– Right-hand drive standard; left-hand drive vehicles generally not registered.

– State-level road tax and registration rules vary significantly.

– Mandatory fitness tests after 15 years for commercial vehicles; private vehicles have no periodic federal test (but may require state-level checks).

United Arab Emirates (UAE)

Logistics Overview:

The UAE serves as a key logistics gateway to the Middle East, with world-class ports (e.g., Jebel Ali) and free zones. Vehicle distribution is efficient across Emirates via modern highways.

Regulatory Compliance:

– Ministry of Interior / RTA (Roads and Transport Authority): Manages vehicle registration and road safety.

– ESMA (Emirates Authority for Standardization and Metrology): Enforces UAE Conformity Assessment Scheme (ECAS).

– GCC Standards: Vehicles must meet GCC Standardization Organization (GSO) regulations (based on EU standards).

– Emissions: Must comply with Euro 4 or higher (Euro 6 preferred).

– Customs: 5% customs duty on imported vehicles; VAT of 5% applies. No duty within GCC.

Key Considerations:

– Right-hand drive vehicles permitted (due to historical British influence) and common.

– Mandatory vehicle inspection (e.g., in Dubai at Tasjeel centers) every 2 years.

– Extreme heat requires vehicles to meet specific durability and cooling standards.

Australia

Logistics Overview:

Vehicle logistics rely on major sea ports (e.g., Melbourne, Sydney, Brisbane) and long-haul road transport due to vast distances. Domestic distribution is dominated by large logistics providers.

Regulatory Compliance:

– Department of Infrastructure, Transport, Regional Development, Communications and the Arts: Oversees the Australian Design Rules (ADR).

– ADR Compliance: All new vehicles must meet ADRs for safety, emissions (ADR 79 based on Euro 5/6), and anti-theft.

– Import Approval: Vehicles under 25 years old must be on the Register of Approved Vehicles (RAV). Non-modified RHD vehicles from certain countries (e.g., UK, NZ, Japan) may qualify.

– Customs & Biosecurity: Quarantine inspection by DAFF for soil, plant matter, or pests.

Key Considerations:

– Right-hand drive standard.

– 25-year rule applies to private imports (vehicles older than 25 years can be imported freely).

– State-based registration and safety inspections (e.g., pink slip in NSW).

Canada

Logistics Overview:

Integrated with U.S. logistics, especially in the automotive corridor (Southern Ontario to Michigan). Rail and trucking dominate, with key ports in Vancouver and Halifax.

Regulatory Compliance:

– Transport Canada: Enforces Canada Motor Vehicle Safety Standards (CMVSS), closely aligned with U.S. FMVSS.

– Environment and Climate Change Canada: Administers emissions and fuel efficiency regulations (aligned with U.S. EPA).

– Import Requirements: Vehicles must comply with CMVSS. Non-conforming vehicles may be imported if modified by a Registrar of Imported Vehicles (RIV).

– Customs: Duties may apply depending on country of origin (e.g., under CUSMA/USMCA, many vehicles are duty-free).

Key Considerations:

– Right-hand drive vehicles allowed but must meet CMVSS; rarely registered.

– Cold-weather adaptations (e.g., block heaters) recommended for compliance in extreme climates.

– Provincial regulations vary for registration, emissions testing (e.g., Drive Clean in Ontario – now suspended), and safety inspections.

In conclusion, sourcing automobile manufacturers by country reveals a diverse and dynamic global industry shaped by regional expertise, economic policies, technological advancements, and supply chain efficiencies. Countries such as Germany, Japan, and South Korea are renowned for engineering excellence and high-quality manufacturing, while the United States stands out for innovation and large-scale production. Meanwhile, emerging markets like China, India, and Mexico are increasingly significant due to cost-effective production, growing domestic demand, and supportive government initiatives.

Each country offers unique advantages—be it skilled labor, advanced infrastructure, favorable trade agreements, or proximity to key markets—making strategic sourcing a critical component of automotive supply chain management. Ultimately, the choice of sourcing location should align with business objectives such as cost reduction, quality assurance, scalability, and sustainability. A well-informed, global sourcing strategy enables automakers to remain competitive, resilient, and responsive to evolving market demands in an increasingly interconnected industry.