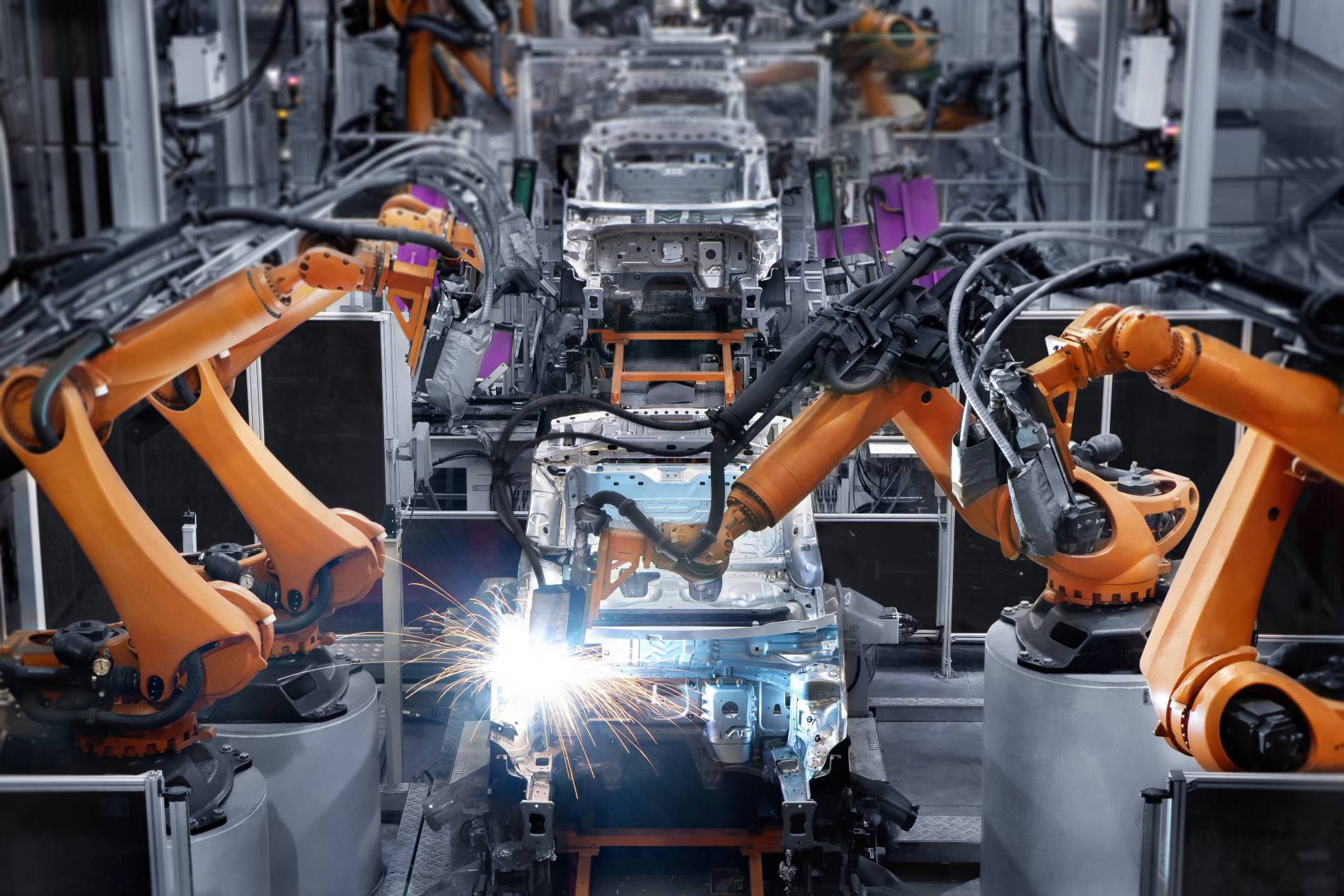

The U.S. automotive manufacturing industry remains a cornerstone of the nation’s industrial economy, contributing significantly to employment, technological innovation, and GDP. According to a 2023 report by Grand View Research, the U.S. automotive market size was valued at approximately $1.1 trillion and is projected to grow at a compound annual growth rate (CAGR) of 4.7% from 2023 to 2030. This expansion is driven by rising demand for electric vehicles (EVs), advancements in autonomous driving technologies, and strong consumer appetite for SUVs and light trucks. Mordor Intelligence further supports this trajectory, forecasting a CAGR of 5.2% for the U.S. automotive market between 2024 and 2029. As the sector evolves, domestic manufacturers are increasingly investing in sustainable production methods and digital supply chain integration to maintain competitiveness. Against this backdrop, nine key players have emerged as leaders in innovation, output volume, and market influence—shaping the future of mobility across the United States.

Top 9 Automotive In Usa Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Automotive In Usa

H2: Key Automotive Market Trends in the USA for 2026

As the U.S. automotive industry moves toward 2026, it is poised for transformative shifts driven by electrification, technological integration, evolving consumer behavior, and regulatory pressures. The second half of the decade is expected to solidify several key trends that will redefine mobility, manufacturing, and market dynamics across the nation.

1. Accelerated Electrification and EV Market Maturation

By 2026, electric vehicle (EV) adoption in the USA is expected to reach a critical inflection point. EVs could represent 18–22% of total new light-duty vehicle sales, up from around 9% in 2023, fueled by expanded model availability, declining battery costs, and stronger federal and state incentives.

- Diverse EV Lineups: Legacy automakers (Ford, GM, Stellantis) will have fully rolled out their next-generation EV platforms, offering affordable EVs below $35,000 to compete with Tesla and emerging players like Rivian and Lucid.

- Battery Innovation: Solid-state batteries may begin limited commercial deployment, enhancing range (400+ miles), reducing charging times, and improving safety.

- Charging Infrastructure Expansion: The federal National Electric Vehicle Infrastructure (NEVI) program will have significantly expanded fast-charging networks along major highways, alleviating range anxiety and supporting long-distance EV travel.

2. Regulatory and Policy-Driven Transformation

Federal and state policies will continue to shape the automotive landscape.

- EPA and NHTSA Standards: Stricter emissions and fuel economy regulations (aligned with the Biden administration’s 2032 targets) will accelerate internal combustion engine (ICE) phase-outs and push automakers toward zero-emission vehicles (ZEVs).

- California’s ZEV Mandate Influence: California and the 17 states adopting its standards will mandate that over 50% of new car sales be ZEVs by 2026, forcing OEMs to prioritize EV production.

- Incentive Evolution: The Inflation Reduction Act (IRA) tax credits will remain pivotal, though eligibility rules tied to battery sourcing and final assembly locations will drive reshoring of supply chains.

3. Technological Advancements and Software-Defined Vehicles

The car is increasingly becoming a software platform, with over-the-air (OTA) updates, connected services, and advanced driver-assistance systems (ADAS) becoming standard.

- Widespread ADAS Adoption: By 2026, Level 2+ autonomy (e.g., adaptive cruise, lane-keeping, automated parking) will be standard in most new vehicles. True Level 3 systems (conditional autonomy) may debut in limited luxury or fleet applications.

- Vehicle-to-Everything (V2X): Pilot programs for V2X communication will expand, enhancing traffic safety and enabling smart city integration.

- Monetization of Software Services: Automakers will increasingly generate revenue through subscription-based features (e.g., enhanced navigation, performance boosts, entertainment).

4. Supply Chain Resilience and Domestic Manufacturing

Geopolitical tensions and pandemic-era disruptions have pushed automakers to localize supply chains.

- Battery Gigafactories Boom: The U.S. will host over 40 battery manufacturing plants by 2026, supported by IRA investments, reducing reliance on Asian suppliers.

- Critical Mineral Sourcing: Partnerships with allied nations (Canada, Australia) and domestic mining initiatives will aim to secure lithium, cobalt, and nickel supplies.

- Reshoring of EV Components: Increased production of motors, power electronics, and semiconductors within North America will enhance supply chain security.

5. Shifting Consumer Preferences and Mobility Models

Consumers are re-evaluating car ownership, especially in urban areas.

- Rise of Subscription and Leasing Models: Flexible ownership options, including short-term EV subscriptions and lease-to-own programs, will gain traction among younger demographics.

- Growth of Mobility-as-a-Service (MaaS): Integration of ride-hailing, car-sharing, and public transit apps will offer seamless multi-modal transportation.

- Demand for Larger Vehicles Persists: Despite EV growth, consumer preference for SUVs and pickup trucks will continue, prompting automakers to electrify these high-margin segments (e.g., F-150 Lightning, Silverado EV).

6. Challenges and Headwinds

Despite progress, several challenges could impact the 2026 outlook.

- Affordability Concerns: High EV prices and interest rates may slow mass-market adoption, especially among lower-income households.

- Grid Capacity and Energy Equity: Rural and underserved urban areas may face charging deserts, requiring targeted infrastructure investment.

- Labor and Workforce Transition: Auto industry unions (e.g., UAW) will negotiate contracts addressing EV transition impacts on jobs, wages, and retraining.

Conclusion:

By H2 2026, the U.S. automotive market will be defined by a robust pivot toward electrification, deeper integration of digital technologies, and policy-driven sustainability goals. While challenges remain in affordability, infrastructure, and equity, the convergence of innovation, regulation, and consumer demand will position the American auto industry at the forefront of a global mobility transformation. Automakers that adapt swiftly to these trends—prioritizing affordable EVs, resilient supply chains, and customer-centric digital experiences—will lead the market into the next decade.

Common Pitfalls Sourcing Automotive Components in the USA (Quality, IP)

Quality Inconsistencies Across Suppliers

One of the primary challenges when sourcing automotive components in the USA is ensuring consistent quality across different suppliers. While the U.S. manufacturing sector is generally reputable, there can be significant variation in quality standards—especially between large Tier 1 suppliers and smaller regional manufacturers. Inadequate process controls, inconsistent raw material sourcing, or lapses in quality assurance protocols can result in defective parts, leading to costly recalls or production line stoppages. Buyers must conduct rigorous supplier audits, demand certifications (such as IATF 16949), and implement ongoing quality monitoring to mitigate these risks.

Intellectual Property (IP) Exposure and Protection Gaps

Sourcing in the USA does not automatically safeguard intellectual property, and companies often face risks related to design theft, reverse engineering, or unauthorized use of proprietary technology. Even with strong U.S. IP laws, enforcement can be slow and expensive. Suppliers may inadvertently (or intentionally) share sensitive design data with third parties, particularly in cases involving subcontracting or shared facilities. To protect IP, buyers should establish clear legal agreements—including robust Non-Disclosure Agreements (NDAs) and ownership clauses—and limit access to critical design information on a need-to-know basis.

Overreliance on Domestic Sourcing Without Due Diligence

A common misconception is that sourcing domestically eliminates supply chain risks. However, assuming U.S.-based suppliers inherently deliver superior quality or compliance can lead to inadequate vetting. Some domestic suppliers may outsource key processes overseas without disclosure, introducing hidden quality and IP vulnerabilities. Buyers must perform thorough supply chain mapping and conduct on-site assessments, regardless of a supplier’s location, to ensure transparency and compliance with automotive industry standards.

Logistics & Compliance Guide for the Automotive Industry in the USA

Overview of the U.S. Automotive Logistics Landscape

The U.S. automotive industry relies on a complex, multi-tiered supply chain involving manufacturers, suppliers, distributors, and dealers. Logistics operations include inbound material handling, production sequencing, outbound vehicle distribution, and after-sales parts delivery. Efficient coordination across rail, truck, and port networks is essential, particularly given the just-in-time (JIT) and just-in-sequence (JIS) manufacturing models widely used in the sector.

Key Regulatory Agencies and Oversight

Several federal agencies regulate automotive logistics and compliance in the U.S. The Department of Transportation (DOT) oversees transportation safety and hazardous materials. The Environmental Protection Agency (EPA) enforces emissions and fuel economy standards. The National Highway Traffic Safety Administration (NHTSA) manages vehicle safety standards and recalls. Additionally, U.S. Customs and Border Protection (CBP) monitors imported vehicles and parts compliance.

Importing Vehicles and Parts: Customs Compliance

All vehicles and automotive components entering the U.S. must comply with CBP regulations. Importers must file accurate entry documentation, including the HS Code classification, country of origin, and value declaration. Vehicles must also meet EPA and NHTSA import eligibility requirements. Non-conforming vehicles may require modification or face denial of entry. A Customs Bond is mandatory for commercial imports.

Federal Motor Vehicle Safety Standards (FMVSS)

Administered by NHTSA, the FMVSS sets performance requirements for all motor vehicles and equipment sold in the U.S. Importers and manufacturers must certify that vehicles and components—such as brakes, airbags, lighting, and tires—comply with applicable FMVSS regulations. Certification involves testing, recordkeeping, and affixing a DOT conformity label to each vehicle.

Environmental and Emissions Regulations

The EPA regulates vehicle emissions under the Clean Air Act. All new vehicles and engines must receive an EPA Certificate of Conformity before sale or import. Manufacturers must also comply with Corporate Average Fuel Economy (CAFE) standards set by NHTSA in coordination with the EPA. Logistics operations involving fuel storage or vehicle testing may require environmental permits.

Hazardous Materials Transportation (DOT Regulations)

Automotive logistics often involve shipping hazardous materials such as batteries, fuels, oils, and adhesives. The DOT’s Hazardous Materials Regulations (HMR), found in 49 CFR, govern packaging, labeling, placarding, documentation, and training. Shippers must classify materials correctly, use approved containers, and ensure drivers are trained and certified under HM-126 requirements.

Hours of Service and Driver Compliance

Commercial drivers transporting automotive goods must comply with the Federal Motor Carrier Safety Administration (FMCSA) Hours of Service (HOS) rules. These regulations limit driving time (e.g., 11 hours after 10 consecutive hours off duty) to prevent fatigue. Electronic Logging Devices (ELDs) are required to automatically record driving time and ensure compliance.

Vehicle Identification Number (VIN) and Titling Requirements

Each vehicle manufactured or imported into the U.S. must have a unique 17-character VIN compliant with ISO 3779 and FMVSS Standard No. 115. The VIN is essential for registration, titling, and tracking recalls. States require VIN verification during vehicle registration, and logistics providers handling vehicle distribution must ensure VIN accuracy and visibility.

Recall Management and Notification Obligations

Manufacturers and importers are required to report safety-related defects to NHTSA and initiate recalls if necessary. Logistics partners may be involved in retrieving or redistributing recalled vehicles and parts. Timely communication and coordination with dealers and distributors are critical to ensure compliance and public safety.

State-Level Regulations and Titling

While federal rules set the baseline, state departments of motor vehicles (DMVs) regulate titling, registration, and emissions testing. Logistics operations crossing state lines must account for variations in state laws, especially regarding emissions (e.g., California’s CARB standards) and commercial vehicle registration (IRP and IFTA for interstate fleets).

Cybersecurity and Data Compliance

With increasing connectivity in modern vehicles, logistics and OEMs must comply with data protection standards. While no federal automotive-specific cybersecurity law exists yet, best practices from NHTSA and U.S. DOT guidance recommend securing vehicle data and supply chain IT systems. Compliance with general regulations like the FTC Act and state privacy laws (e.g., CCPA) may also apply.

Best Practices for Supply Chain Compliance

To maintain regulatory compliance and operational efficiency, automotive logistics providers should: maintain accurate documentation, conduct regular compliance audits, train personnel on DOT/EPA/NHTSA requirements, use certified third-party logistics (3PL) partners, and stay updated on regulatory changes. Investing in transportation management systems (TMS) and compliance software can streamline adherence and reduce risk.

In conclusion, sourcing automotive manufacturers in the USA presents a compelling opportunity for businesses seeking high-quality production, advanced technology, and reliable supply chain logistics. The U.S. automotive manufacturing sector benefits from strong infrastructure, skilled labor, stringent quality standards, and government incentives promoting domestic production and innovation—particularly in electric and autonomous vehicles. While cost considerations such as labor and materials may be higher compared to some offshore alternatives, the advantages in proximity, reduced lead times, intellectual property protection, and alignment with “Buy American” policies often outweigh these factors. Additionally, ongoing reshoring trends and investments in automation are enhancing competitiveness. Therefore, partnering with U.S.-based automotive manufacturers can support long-term operational resilience, compliance, and sustainability goals, making it a strategic choice for companies prioritizing quality, speed to market, and supply chain transparency.