The global semiconductor industry has experienced robust expansion over the past decade, driven by rising demand in consumer electronics, automotive technologies, industrial automation, and data centers. According to a 2023 report by Mordor Intelligence, the semiconductor market was valued at USD 573.8 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 7.4% from 2023 to 2028, reaching an estimated USD 870.2 billion by the end of the forecast period. This growth is further fueled by advancements in 5G, artificial intelligence, and the Internet of Things (IoT), all of which rely heavily on integrated circuits and microchips. As technological innovation accelerates worldwide, certain countries have emerged as dominant players in chip manufacturing, leveraging strategic investments, advanced fabrication facilities, and strong government support. These nations now account for the majority of global semiconductor production capacity, shaping the supply chains that power modern digital infrastructure. The following analysis explores the top eight countries leading this high-stakes industry, based on production volume, market share, and technological capabilities.

Top 8 Biggest Chip Country Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Biggest Chip Country

2026 Market Trends for the Biggest Chip Country (H2 2026)

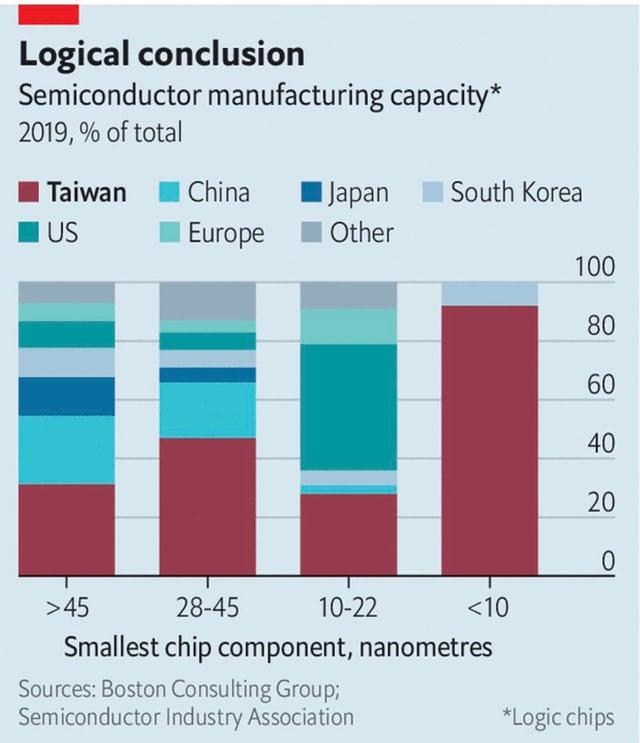

As we move through the second half of 2026, the semiconductor industry continues to evolve rapidly, with significant developments shaping the market landscape. Taiwan remains the undisputed leader in advanced semiconductor manufacturing—the “Biggest Chip Country” in terms of technological sophistication, production capacity, and global influence—driven primarily by Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest dedicated semiconductor foundry.

This analysis explores key trends shaping Taiwan’s semiconductor industry in H2 2026, covering technological advancements, geopolitical dynamics, supply chain resilience, AI-driven demand, and global competition.

1. Dominance in Advanced Node Manufacturing

By H2 2026, TSMC has solidified its leadership in cutting-edge process technologies. The 2nm (N2) node has entered high-volume production, with early adoption by leading clients such as Apple, NVIDIA, AMD, and Amazon’s AWS. This node introduces Gate-All-Around (GAA) transistor architecture at scale, delivering significant improvements in power efficiency, performance, and transistor density.

- N2 and N2P (Performance-enhanced): Initial yields are stable, with 2nm chips powering next-generation AI accelerators and mobile SoCs.

- 3nm Ecosystem Maturity: The 3nm process family (N3E, N3P) now accounts for over 35% of TSMC’s revenue, supporting a broad base of consumer electronics, servers, and automotive applications.

- R&D Push for 1.4nm (A14): Pilot production lines for the 1.4nm process are operational, with risk production expected in 2027.

Taiwan’s ability to maintain a 2–3-year technology lead over global competitors reinforces its critical role in the global tech supply chain.

2. AI and HPC as Primary Growth Drivers

Artificial Intelligence (AI) and High-Performance Computing (HPC) remain the primary demand engines for Taiwanese-made chips.

- AI Chip Demand Soars: Generative AI models, edge AI, and data center expansion continue to drive demand for specialized chips. TSMC is the foundry of choice for NVIDIA’s Blackwell and next-gen Rubin architectures, as well as custom ASICs from Google, Meta, and Microsoft.

- HPC Revenue Share: Over 50% of TSMC’s revenue in H2 2026 comes from HPC-related products, up from 40% in 2023.

- Advanced Packaging Leadership: TSMC’s CoWoS (Chip-on-Wafer-on-Substrate) and SoIC (System on Integrated Chips) packaging technologies are in high demand, though capacity constraints remain a bottleneck. The company has expanded CoWoS capacity by 60% year-on-year, with new facilities in Taoyuan and Kaohsiung coming online.

3. Geopolitical Tensions and Supply Chain Diversification

Geopolitical risks continue to influence investment and production strategies.

- Cross-Strait Relations: Heightened tensions between China and Taiwan have prompted global customers to pressure TSMC for greater supply chain resilience. While Taiwan remains the core production hub, TSMC’s international fabs (Arizona, Japan, and soon Germany) are ramping up.

- U.S.-Taiwan Tech Alignment: The U.S. CHIPS Act and allied export controls have deepened cooperation. American tech firms are increasingly co-developing chip architectures with TSMC to ensure access and reduce geopolitical risk.

- China’s Domestic Push: Despite China’s aggressive investments in SMIC and other domestic foundries, it remains at least two technology nodes behind Taiwan. However, China is gaining ground in mature nodes (28nm and above), reducing its reliance on Taiwanese chips for legacy applications.

4. Sustainability and Energy Constraints

Taiwan’s semiconductor industry faces growing pressure to address environmental concerns.

- Water and Energy Use: Semiconductor fabs are among the largest industrial water consumers. Drought concerns in 2025 prompted TSMC to invest heavily in water recycling (now at 90% reuse) and alternative sources, including desalination plants.

- Carbon Neutrality Goals: TSMC aims for net-zero emissions by 2050. In H2 2026, over 30% of its energy comes from renewable sources, supported by offshore wind partnerships and on-site solar installations.

- Green Packaging Innovations: New eco-conscious packaging materials and processes are being adopted to meet ESG requirements from global clients.

5. Workforce and Talent Challenges

Despite automation, talent remains a critical constraint.

- Engineering Shortage: Demand for semiconductor engineers in Taiwan outpaces supply. The government has expanded scholarships and immigration pathways for foreign talent.

- Knowledge Transfer: As TSMC expands globally, it faces challenges in maintaining its unique manufacturing culture and process know-how across international sites.

6. Global Competition and Policy Responses

While Taiwan leads, competition is intensifying.

- South Korea (Samsung): Samsung has improved yield on its 2nm GAA process but still lags in customer adoption. Its focus remains on memory and select logic partnerships.

- United States (Intel Foundry): Intel 18A process is competitive, but volume production delays have limited market share. U.S. government subsidies are accelerating capacity expansion.

- EU and Japan: Governments are investing heavily in local foundry capabilities, but neither is expected to challenge Taiwan’s dominance in advanced logic before 2030.

Conclusion

In H2 2026, Taiwan remains the epicenter of advanced semiconductor manufacturing, driven by TSMC’s technological leadership, booming AI demand, and strategic global partnerships. However, the industry faces mounting challenges—geopolitical instability, supply chain fragility, environmental constraints, and global competition.

Taiwan’s ability to innovate, scale sustainably, and navigate geopolitical currents will determine whether it maintains its “Biggest Chip Country” status in the long term. For now, the world’s most powerful chips still bear the invisible stamp of Taiwan’s silicon mastery.

Common Pitfalls When Sourcing the Biggest Chip in the Country (Quality, IP)

Sourcing the largest semiconductor or chip from a leading country—often referring to nations like the U.S., South Korea, Taiwan, or China—can present significant opportunities. However, companies must navigate several critical pitfalls related to quality assurance and intellectual property (IP) protection. Understanding these risks is essential to avoid costly setbacks.

Quality-Related Pitfalls

1. Inconsistent Manufacturing Standards

Even within top-tier chip-producing countries, not all manufacturers adhere to the same quality benchmarks. Sourcing from less reputable suppliers may result in substandard chips that fail under stress or have shortened lifespans. It’s crucial to verify compliance with international standards such as ISO 9001 or IATF 16949 (for automotive applications).

2. Counterfeit or Recycled Components

The global demand for high-performance chips has led to a rise in counterfeit products. Some suppliers may pass off recycled, remarked, or cloned chips as new. These components can lead to field failures, safety risks, and reputational damage.

3. Lack of Traceability

Without full supply chain transparency, it’s difficult to confirm the origin and handling history of a chip. Poor traceability increases the risk of receiving defective or non-compliant parts, especially when sourcing through third-party distributors.

4. Insufficient Testing and Validation

Some suppliers may skimp on post-production testing. Without rigorous validation—such as burn-in tests, parametric testing, or reliability screening—defective units may go undetected until deployment.

Intellectual Property (IP) Risks

1. Unauthorized Cloning or IP Theft

In certain regions, weak enforcement of IP laws increases the risk that proprietary chip designs are reverse-engineered or copied without permission. This not only undermines innovation but can flood the market with cheaper, illegal alternatives.

2. Shared Foundry Access

Many chip manufacturers use third-party foundries. If IP protections are not contractually enforced, design data could be exposed to competitors using the same fabrication facilities, leading to potential leaks or misuse.

3. Ambiguous Licensing Agreements

Poorly defined licensing terms can result in unintended IP exposure. Companies may unknowingly grant broader usage rights than intended, or fail to retain ownership of custom-designed components.

4. Export Control and Compliance Issues

Sourcing high-end chips may trigger regulatory scrutiny, especially if the technology is subject to export controls (e.g., U.S. EAR or China’s export laws). Non-compliance can result in legal penalties and supply chain disruptions.

Mitigation Strategies

- Conduct thorough due diligence on suppliers, including audits and certification checks.

- Use trusted distribution channels and avoid gray market sources.

- Implement robust contractual safeguards, including IP clauses and confidentiality agreements.

- Employ independent testing and verification processes before integration.

- Stay informed about geopolitical and regulatory developments affecting chip sourcing.

Avoiding these pitfalls requires a proactive approach focused on quality assurance, legal protection, and supply chain integrity.

Logistics & Compliance Guide for Biggest Chip Country

Note: As of now, there is no officially recognized country called “Biggest Chip Country.” This appears to be a fictional or placeholder name. For the purpose of this guide, we will assume it refers to a hypothetical nation where a major global snack chip manufacturer (“Biggest Chip”) is establishing operations or expanding distribution. The following logistics and compliance framework is designed as a general best-practice guide applicable to multinational food manufacturing and distribution, adaptable to real-world regulatory environments such as the U.S., EU, or other major markets.

Supply Chain Infrastructure

Establish a resilient supply chain network tailored to the geographic and regulatory landscape of Biggest Chip Country. This includes:

- Sourcing Raw Materials: Partner with certified local and regional suppliers for potatoes, oils, seasonings, and packaging materials. Ensure supplier compliance with food safety standards (e.g., GFSI benchmarks like SQF or BRCGS).

- Warehousing & Distribution Centers: Strategically locate climate-controlled facilities near high-demand urban centers and transportation hubs to reduce lead times and fuel costs.

- Transportation Management: Utilize a mix of refrigerated and ambient transport for finished goods. Partner with licensed, insured logistics providers compliant with local transportation regulations, including hours-of-service and vehicle safety standards.

Regulatory Compliance

Adherence to local, national, and international regulations is critical for legal operation and brand integrity.

- Food Safety Regulations: Comply with the national food safety authority (e.g., equivalent to FDA in the U.S. or EFSA in the EU). Implement HACCP (Hazard Analysis and Critical Control Points) plans and maintain full traceability from farm to shelf.

- Labeling Requirements: Ensure all packaging meets local language, nutritional labeling, allergen declaration, and health claim regulations. Include mandatory icons (e.g., recyclable packaging symbols) and barcode standards.

- Import/Export Controls: For cross-border operations, secure necessary permits, file accurate customs declarations, and comply with tariff classifications under the country’s customs code (e.g., HS Code 2009.50 for prepared vegetables).

- Environmental & Sustainability Laws: Follow waste disposal regulations, plastic tax requirements, and carbon reporting mandates. Implement packaging reduction initiatives in line with Extended Producer Responsibility (EPR) schemes.

Quality Assurance & Audits

Maintain consistent product quality and regulatory alignment through continuous monitoring.

- Internal Audits: Conduct quarterly audits of manufacturing plants, warehouses, and co-packers using standardized checklists aligned with ISO 22000 or FSSC 22000.

- Third-Party Certifications: Obtain and renew certifications such as ISO 9001 (Quality Management), ISO 14001 (Environmental Management), and organic/non-GMO project verification where applicable.

- Product Testing: Perform regular microbiological, chemical, and physical testing at accredited labs to verify compliance with national maximum residue limits (MRLs) and contaminant thresholds.

Labor & Operational Compliance

Ensure ethical labor practices and safe working conditions across all facilities.

- Workplace Safety: Comply with national occupational health and safety standards (e.g., OSHA-equivalent regulations). Provide PPE, safety training, and emergency response protocols.

- Labor Laws: Adhere to local employment regulations covering wages, working hours, overtime, and anti-discrimination policies. Maintain accurate employee records and contracts.

- Training Programs: Deliver mandatory compliance training for staff on food hygiene, allergen control, and incident reporting procedures.

Documentation & Record Keeping

Maintain a centralized, digital compliance management system for all operational records.

- Retention Period: Store critical documents (e.g., batch records, shipping logs, certificates of analysis) for a minimum of 5 years or as required by local law.

- Traceability Systems: Implement ERP or blockchain-based traceability tools to enable rapid recall response if contamination is detected.

- Regulatory Filings: Submit required reports to authorities, such as annual food facility registrations, ingredient disclosures, and sustainability disclosures.

Crisis Management & Recall Preparedness

Develop and test a product recall and crisis response plan.

- Recall Team: Assign a cross-functional team with clear roles for communication, logistics, and regulatory reporting.

- Mock Recalls: Conduct biannual mock recalls to validate traceability and response speed.

- Stakeholder Communication: Prepare templates for notifications to regulators, retailers, and consumers in compliance with local recall protocols.

By implementing this logistics and compliance framework, Biggest Chip can ensure efficient, legal, and sustainable operations within Biggest Chip Country, minimizing risk and enhancing consumer trust. Always consult with local legal counsel and regulatory experts to tailor these guidelines to the specific jurisdiction.

In conclusion, when sourcing from the biggest chip manufacturing countries, Taiwan, South Korea, the United States, and China stand out as global leaders. Taiwan, home to TSMC, dominates advanced semiconductor fabrication and is critical to the global supply chain. South Korea, with Samsung and SK Hynix, excels in memory chips and high-performance processors. The United States remains a powerhouse in semiconductor design and innovation, with leading firms like Intel, NVIDIA, and AMD, supported by strong R&D and recent government investments through initiatives like the CHIPS Act. Meanwhile, China is rapidly expanding its domestic semiconductor capabilities, aiming for self-reliance amid geopolitical tensions.

For businesses seeking reliable and high-quality chip sources, partnering with manufacturers in these key countries ensures access to cutting-edge technology, large-scale production capacity, and resilient supply chains. However, geopolitical risks, export controls, and supply chain vulnerabilities highlight the importance of diversification and strategic sourcing. Ultimately, a balanced approach—leveraging the strengths of each region while mitigating risks—will be essential for long-term success in the competitive semiconductor landscape.