The global semiconductor industry continues its robust expansion, driven by surging demand for advanced electronics, 5G infrastructure, artificial intelligence, and electric vehicles. According to a 2023 report by Mordor Intelligence, the computer chip market was valued at USD 571.9 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 7.4% from 2024 to 2029, reaching an estimated USD 877.2 billion by the end of the forecast period. This growth trajectory reflects a structural shift in global technology consumption and production, with semiconductor manufacturers scaling capacity and investing heavily in next-generation fabrication processes. As geopolitical dynamics and supply chain resilience take center stage, the dominance of key players becomes increasingly critical. The following list highlights the top 10 biggest computer chip manufacturers—ranked by revenue, market share, and technological influence—shaping the backbone of modern computing and powering innovation across industries worldwide.

Top 10 Biggest Computer Chip Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Biggest Computer Chip

H2: 2026 Market Trends for the Biggest Computer Chip Companies

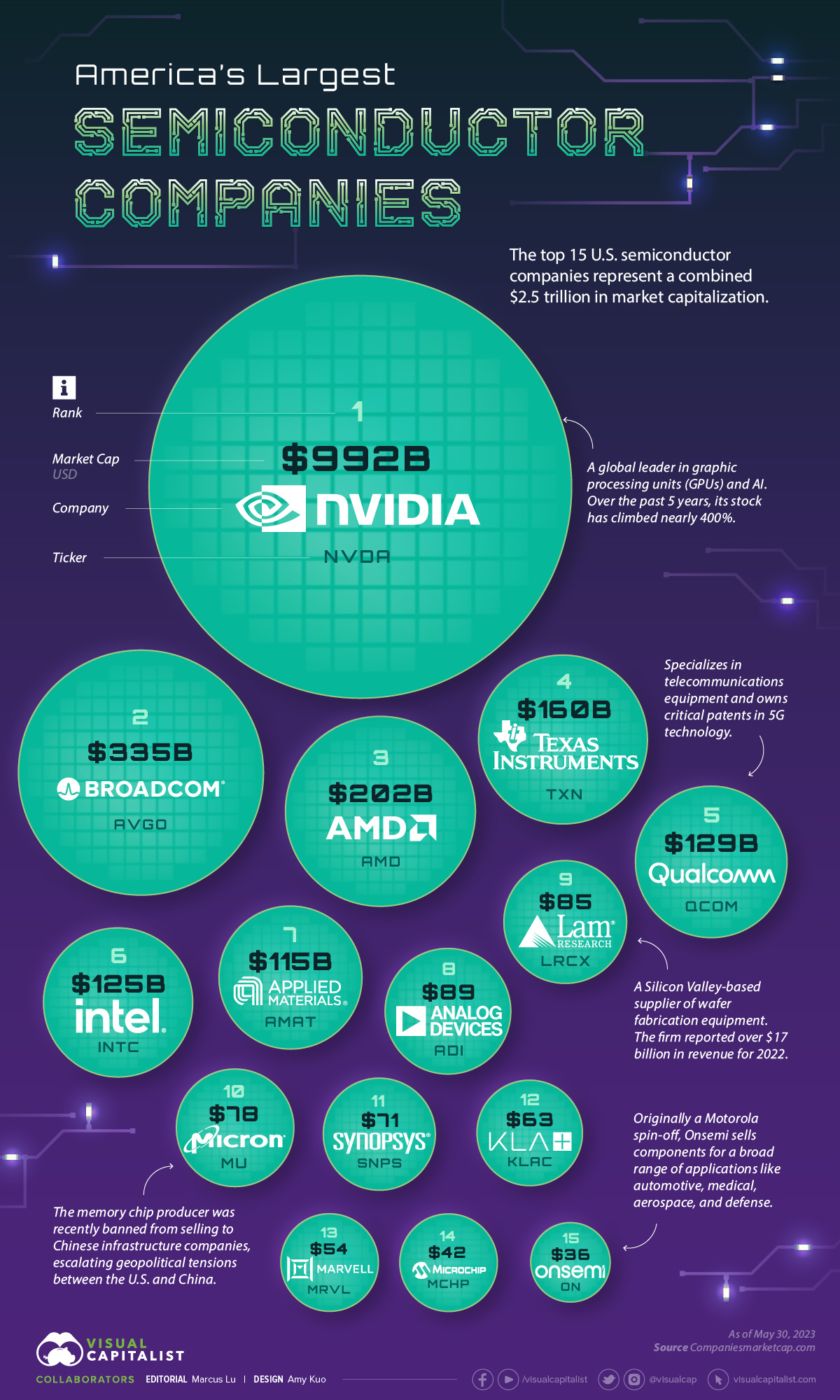

As we approach 2026, the global semiconductor industry is poised for transformative growth, driven by escalating demand for artificial intelligence (AI), data centers, electric vehicles (EVs), 5G/6G infrastructure, and advanced consumer electronics. The “biggest” computer chip companies—such as NVIDIA, Intel, AMD, TSMC, and Samsung Electronics—are expected to dominate market dynamics, but with shifting competitive landscapes and technological inflections. Here’s an in-depth analysis of key market trends shaping the industry in 2026:

-

AI and High-Performance Computing (HPC) Drive Chip Demand

AI workloads will remain the primary growth engine for advanced semiconductor demand. By 2026, AI accelerators—especially GPUs and specialized AI chips from NVIDIA and AMD—will command a significant share of data center spending. Generative AI, large language models (LLMs), and edge AI inference will require increasingly powerful and energy-efficient chips, pushing companies to develop next-gen architectures like chiplets and 3D stacking. -

TSMC and Samsung Lead in Advanced Node Manufacturing

Foundry giants TSMC and Samsung are expected to mass-produce chips using 2nm and even 1.4nm process technologies by 2026. TSMC’s N2 and its successor, N2P (performance-enhanced), will power Apple, NVIDIA, and AMD’s most advanced designs. Samsung’s SF2 process aims to close the technology gap, bolstered by investments in Gate-All-Around (GAA) transistor technology. These advancements will enable higher transistor density, lower power consumption, and improved performance for AI and mobile applications. -

U.S.-China Tech Decoupling Reshapes Supply Chains

Geopolitical tensions will continue to influence chip manufacturing and distribution. The U.S. CHIPS and Science Act and China’s self-sufficiency initiatives are accelerating the regionalization of supply chains. By 2026, we expect increased semiconductor production in the U.S. (e.g., Intel’s Ohio fabs, TSMC’s Arizona facilities) and Europe, reducing reliance on East Asian manufacturing. However, China will push forward with domestic capabilities via SMIC and other players, potentially creating a parallel semiconductor ecosystem. -

Intel’s Comeback Strategy Gains Traction

Intel aims to reclaim its leadership in process technology by 2026 with its Intel 18A node, featuring RibbonFET (GAA) and PowerVia (backside power delivery). If successful, Intel Foundry Services (IFS) will attract major fabless clients, positioning Intel as a credible alternative to TSMC. Concurrently, Intel’s focus on AI chips (Gaudi accelerators) and client CPUs (Core Ultra series) will strengthen its position in data centers and PCs. -

Chiplet Architecture Becomes Industry Standard

To overcome yield and cost challenges in advanced nodes, chipmakers are increasingly adopting chiplet designs—modular silicon components connected via high-speed interfaces like UCIe (Universal Chiplet Interconnect Express). By 2026, AMD, Intel, and NVIDIA will widely utilize chiplets to scale performance while managing complexity. This trend enables heterogeneous integration, combining logic, memory, and I/O dies from different process nodes and vendors. -

Memory and Advanced Packaging Innovations Rise in Importance

With bandwidth bottlenecks limiting chip performance, high-bandwidth memory (HBM4) and 3D-stacked memory will become critical. Samsung, SK Hynix, and Micron are expected to lead HBM4 adoption, essential for AI GPUs and data center accelerators. Simultaneously, advanced packaging technologies—such as Co-Optimization of Chip, Package, and System (COPA) and Foveros—will gain prominence, enabling tighter integration and improved efficiency. -

Sustainability and Energy Efficiency as Key Differentiators

As data centers consume more power, energy-efficient chip design will be a major competitive factor. Companies will emphasize performance-per-watt metrics, leveraging new materials (e.g., 2D semiconductors), power gating, and dynamic voltage/frequency scaling. Regulatory pressure and ESG (Environmental, Social, and Governance) goals will push chipmakers toward greener fabs and sustainable manufacturing practices. -

Automotive and Edge Computing Expand Market Opportunities

The automotive semiconductor market will grow significantly by 2026, fueled by ADAS, autonomous driving, and in-vehicle AI. NVIDIA’s DRIVE platform, Qualcomm’s Snapdragon Digital Chassis, and AMD’s acquisition of Xilinx position these firms strongly in automotive SoCs. Meanwhile, edge computing will demand low-latency, power-efficient chips for IoT, smart cities, and industrial automation.

Conclusion

By 2026, the biggest computer chip companies will navigate a complex landscape defined by technological innovation, geopolitical shifts, and evolving end-market demands. Leadership will hinge on mastery of advanced manufacturing, AI-centric design, and ecosystem integration. Companies that successfully adapt to these trends—particularly in AI acceleration, chiplet architecture, and sustainable innovation—will dominate the next era of computing.

Common Pitfalls When Sourcing the Biggest Computer Chips (Quality and IP Risks)

Sourcing the largest and most advanced computer chips—such as high-performance GPUs, AI accelerators, or cutting-edge SoCs—introduces unique challenges. While size and performance are critical, organizations must also navigate significant risks related to quality assurance and intellectual property (IP) protection. Overlooking these pitfalls can result in supply chain disruptions, legal liabilities, and compromised product integrity.

Quality Assurance Challenges

Largest semiconductor chips, often pushing the limits of process technology and die size, are inherently more susceptible to defects and performance inconsistencies. Ensuring consistent quality requires rigorous validation protocols that many buyers underestimate.

Yield Variability and Defect Density

Large die sizes increase the probability of manufacturing defects due to particle contamination or process inconsistencies. Even minor flaws can render a chip unusable, leading to lower yields. Sourcing from foundries or suppliers without transparent yield data may result in receiving subpar batches, impacting time-to-market and profitability.

Thermal and Power Integrity Issues

Bigger chips generate more heat and require advanced thermal management. Poorly characterized thermal profiles or inadequate power delivery specifications from the supplier can lead to system instability or premature failure in end applications. Buyers must verify thermal design power (TDP) and cooling requirements under real-world conditions.

Inadequate Testing and Validation

Some suppliers may provide chips that pass basic functionality tests but fail under stress or long-term operation. Without access to comprehensive test reports—including burn-in, accelerated life testing, and corner validation—buyers risk integrating unreliable components into critical systems.

Intellectual Property (IP) Risks

The design and fabrication of the largest and most complex chips often involve extensive third-party IP, raising significant legal and compliance concerns during sourcing.

Unverified IP Provenance

Using chips that incorporate unlicensed or improperly sourced IP—such as ARM cores, DSP blocks, or interface controllers—can expose the buyer to infringement claims. This is especially risky when sourcing from second-tier vendors or through indirect distribution channels where IP licensing is not transparent.

Lack of IP Ownership Documentation

Suppliers may claim full rights to a chip design, but without proper documentation—such as IP license agreements, design ownership certificates, or foundry fabrication authorizations—buyers have no legal recourse if disputes arise. This is critical in regulated industries or when seeking product certifications.

Reverse Engineering and Counterfeit Risk

High-value chips are prime targets for cloning or counterfeiting. Sourcing from unauthorized distributors or gray markets increases the risk of receiving re-marked, recycled, or reverse-engineered components that mimic legitimate products but lack reliability and IP legitimacy.

Mitigation Strategies

To avoid these pitfalls, organizations should:

– Partner exclusively with authorized distributors or OEMs.

– Demand detailed quality reports, including wafer sort data and reliability testing.

– Conduct independent audits of IP licensing and design chain transparency.

– Implement supply chain traceability systems and anti-counterfeit verification.

Failing to address quality and IP concerns when sourcing the biggest computer chips can undermine product success and expose companies to operational and legal jeopardy. Due diligence is not optional—it’s a strategic necessity.

Logistics & Compliance Guide for the Biggest Computer Chip

Shipping and managing the world’s largest computer chip presents unique logistical and regulatory challenges due to its size, sensitivity, value, and technological nature. This guide outlines key considerations for handling, transporting, and ensuring compliance throughout the supply chain.

Size and Handling Requirements

The physical dimensions of the largest computer chips—often exceeding standard semiconductor packaging—demand specialized handling. These chips may be integrated into large-scale wafers or advanced packaging substrates that require custom carriers, cleanroom-compatible handling tools, and non-standard automated material handling systems. Manual handling is strongly discouraged due to the risk of electrostatic discharge (ESD), particle contamination, and mechanical stress. Logistics planners must use rigid, ESD-safe containers with custom foam inserts and environmental monitoring capabilities (e.g., humidity and temperature sensors).

Transportation and Packaging

Given their fragility and high value, the biggest computer chips must be shipped in climate-controlled, shock-absorbent packaging. Use of MIL-STD-810G certified containers with real-time GPS and environmental tracking is recommended. Air freight is typically preferred over ground or sea transport to minimize exposure and transit time. All shipments should be double-boxed with inert desiccants and sealed in vacuum or nitrogen-flushed environments to prevent oxidation and moisture damage. Route planning should avoid extreme temperatures, high altitudes, and high-vibration zones.

Export Controls and Regulatory Compliance

Computer chips, especially those at the leading edge of performance and size, are subject to strict export control regulations. In the United States, these fall under the Export Administration Regulations (EAR) administered by the Bureau of Industry and Security (BIS). Depending on the chip’s computational capabilities (e.g., FLOPS, transistor density), it may be classified under ECCN 3A090 or similar categories requiring a license for export to certain countries, particularly those under U.S. sanctions or identified as national security concerns (e.g., China, Russia, Iran).

Similar controls exist under the Wassenaar Arrangement, EU Dual-Use Regulation, and other international frameworks. Compliance requires accurate product classification, end-user screening, and license management. Organizations must maintain detailed records of shipments, end-use certifications, and any license approvals.

Customs and Duties

Customs clearance for high-value semiconductor shipments requires precise documentation, including commercial invoices, packing lists, certificates of origin, and technical specifications. Misclassification can lead to delays, fines, or seizure. Harmonized System (HS) codes such as 8542.31 (integrated circuits) must be applied correctly. Duty drawback programs or free trade agreements (e.g., USMCA, CPTPP) may reduce tariffs where applicable, but eligibility depends on material sourcing and final assembly locations.

Environmental and Safety Regulations

While semiconductor chips are not typically classified as hazardous materials, their packaging may contain regulated substances (e.g., lead under RoHS, perfluorinated compounds). Compliance with REACH (EU), RoHS, and China RoHS is mandatory for market access. Additionally, the transportation of lithium-based power sources used in monitoring devices within the shipment must follow IATA Dangerous Goods Regulations if shipped by air.

Cybersecurity and Intellectual Property Protection

Due to the strategic importance of advanced chips, logistics operations must incorporate cybersecurity measures. GPS trackers, IoT sensors, and shipment data platforms should be encrypted and access-controlled to prevent tracking data breaches. Physical security includes tamper-evident seals and secure warehousing with restricted access. Intellectual property (IP) protection extends to non-disclosure agreements (NDAs) with logistics partners and secure handling protocols to prevent reverse engineering or theft.

Insurance and Risk Management

Given the high unit value—potentially exceeding millions of dollars per chip—comprehensive insurance is critical. Policies should cover all-risk cargo, including damage, theft, and delays. Risk assessments should evaluate geopolitical instability, carrier reliability, and natural disaster exposure along the supply chain. Contingency plans, including alternate routing and rapid replacement protocols, should be established in collaboration with manufacturers and clients.

Conclusion

Successfully managing the logistics of the world’s biggest computer chips requires a holistic strategy integrating advanced packaging, regulatory compliance, secure transport, and risk mitigation. Close coordination between semiconductor manufacturers, logistics providers, and compliance officers ensures that these cutting-edge technologies reach their destinations safely, legally, and on time.

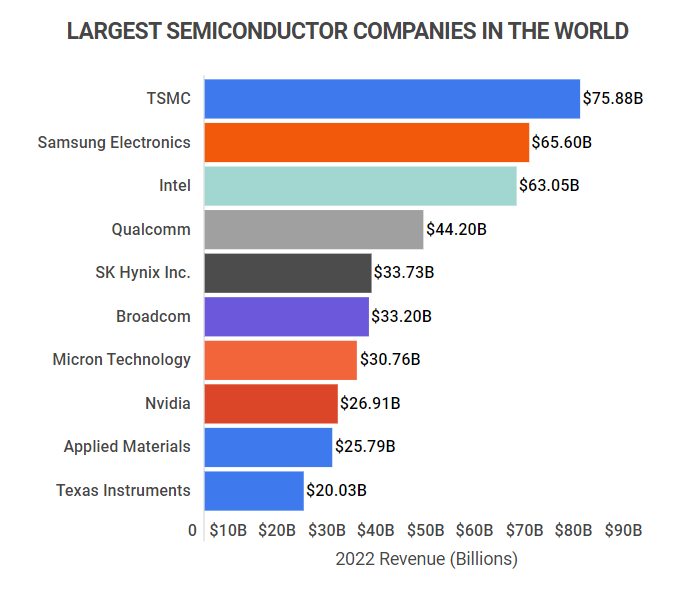

In conclusion, sourcing from the world’s largest computer chip manufacturers—such as Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, Intel, NVIDIA, and Advanced Micro Devices (AMD)—offers significant advantages in terms of technological innovation, production scalability, and reliability. These industry leaders drive advancements in semiconductor technology, enabling faster, more efficient, and energy-conscious computing across sectors including consumer electronics, automotive, artificial intelligence, and data centers.

However, sourcing from these manufacturers also presents challenges, including supply chain constraints, geopolitical risks—particularly in regions like Taiwan and East Asia—high demand leading to limited capacity, and substantial financial investment requirements. Diversifying suppliers, forming strategic partnerships, and investing in long-term procurement agreements can mitigate some of these risks.

Ultimately, aligning sourcing strategies with business goals, technological needs, and risk tolerance is essential. Companies seeking high-performance, cutting-edge chips should prioritize engagement with top-tier manufacturers while maintaining flexibility and exploring alternative suppliers or domestic foundry initiatives to ensure resilience and continuity in an increasingly competitive and volatile global semiconductor market.