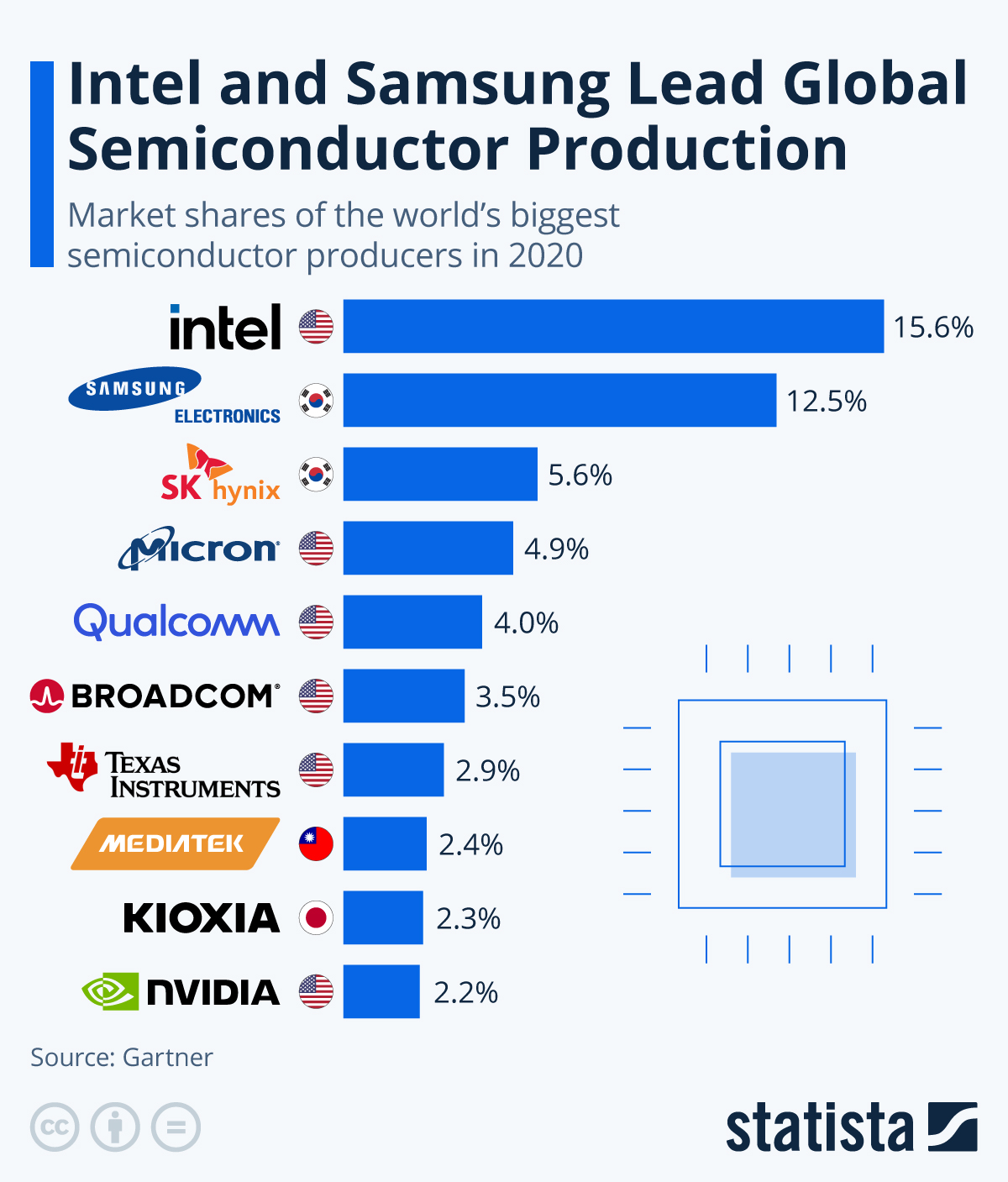

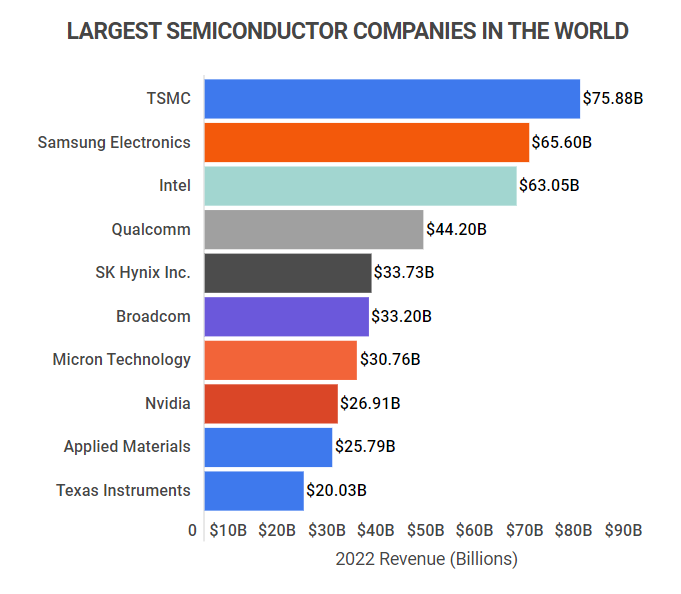

The global semiconductor manufacturing landscape is evolving rapidly, driven by surging demand across industries such as consumer electronics, automotive, artificial intelligence, and telecommunications. According to a 2023 report by Mordor Intelligence, the semiconductor market was valued at approximately USD 574 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 8.7% from 2023 to 2028, reaching an estimated USD 920 billion by the end of the forecast period. This expansion is fueled by the increasing adoption of advanced technologies, including 5G, Internet of Things (IoT) devices, and electric vehicles, all of which require high-performance chips. As innovation accelerates and geopolitical dynamics reshape supply chains, a select group of manufacturers dominate production capacity, technological advancement, and market share. These top players not only control a significant portion of the global foundry and integrated device market but also lead in research and development, process node miniaturization, and manufacturing scale. Based on revenue, market presence, and technical capabilities, the following list outlines the top 10 biggest semiconductor manufacturers shaping the future of technology.

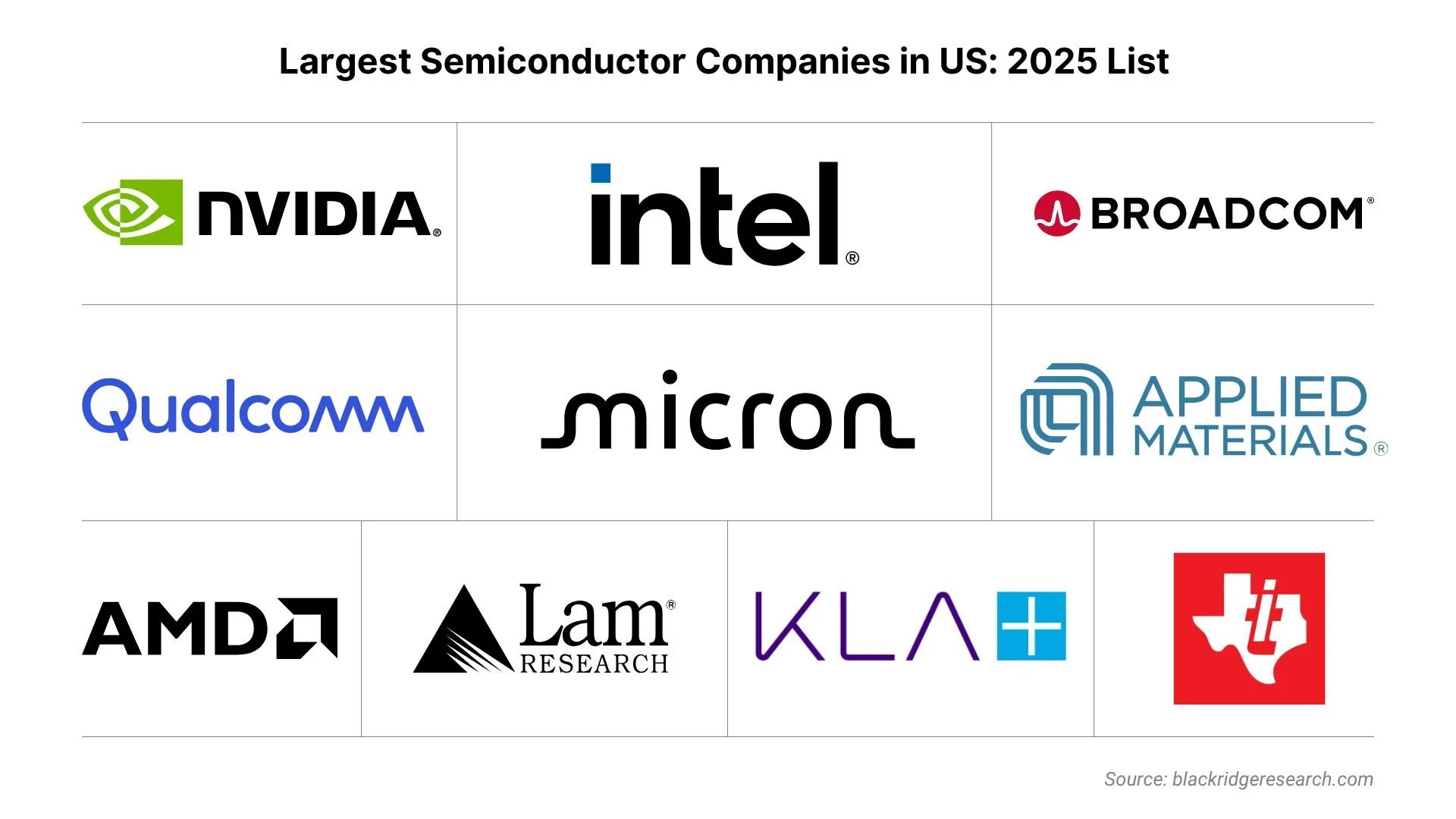

Top 10 Biggest Semiconductor Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Biggest Semiconductor

H2 2026 Market Trends Analysis for the Biggest Semiconductor Companies

As we approach the second half of 2026, the global semiconductor industry continues to evolve rapidly, driven by technological innovation, geopolitical dynamics, and shifting demand across key end markets. The biggest semiconductor companies—such as Taiwan Semiconductor Manufacturing Company (TSMC), NVIDIA, Intel, Samsung Electronics, and Broadcom—are navigating a complex landscape shaped by advances in artificial intelligence (AI), geopolitical fragmentation, supply chain resilience, and the maturation of next-generation technologies.

Below is a detailed analysis of the major market trends influencing the largest semiconductor players in H2 2026:

1. AI and High-Performance Computing (HPC) Drive Demand

Key Trend: AI workloads remain the primary engine of growth.

- NVIDIA continues to dominate the AI accelerator market, with its Blackwell and next-generation B200 and GB200 GPUs in high demand across data centers, cloud providers, and AI startups.

- TSMC’s 2nm (N2) and early 1.4nm (A14) process nodes are fully ramped, enabling AI chipmakers to deliver higher performance with improved power efficiency.

- Custom silicon (ASICs) for AI inference and training is rising, with companies like Google (TPU), Amazon (Trainium/Inferentia), and Microsoft increasingly relying on TSMC and Samsung for advanced packaging and manufacturing.

- Demand for HPC and AI chips is pushing memory bandwidth and chiplet integration to new limits, reinforcing the importance of CoWoS (Chip-on-Wafer-on-Substrate) and Foveros-like packaging.

Impact: TSMC and NVIDIA are best positioned, while Intel gains ground with Gaudi3 and Falcon Shores chips.

2. Geopolitical Fragmentation and Regionalization of Supply Chains

Key Trend: U.S.-China tech decoupling deepens; regional supply chains accelerate.

- The U.S. CHIPS Act and EU Chips Act are yielding tangible results in H2 2026, with Intel, TSMC, and Samsung expanding manufacturing capacity in the U.S. and Europe.

- TSMC’s Arizona fabs are operational, producing 4nm and 3nm chips for Apple and NVIDIA, reducing reliance on Taiwan.

- China continues to advance its domestic semiconductor ecosystem (SMIC, HiSilicon), but remains ~2–3 process nodes behind global leaders. Export controls limit access to EUV tools, slowing progress.

- Japan and South Korea strengthen semiconductor alliances with the U.S. and EU, focusing on materials, equipment, and specialty chips.

Impact: Global leaders diversify manufacturing footprints, increasing capex but enhancing supply chain resilience.

3. Advancements in Process Technology and Packaging

Key Trend: 2nm and beyond nodes go mainstream; 3D and chiplet architectures dominate.

- TSMC’s N2 node, utilizing Gate-All-Around (GAA) transistors, enters high-volume production in H2 2026, offering 10–15% performance gains and 25–30% power reduction over N3.

- Samsung’s SF2 (2nm GAA) is competitive but lags TSMC in yield and customer adoption.

- Intel 20A and 18A (equivalent to 2nm class) gain traction with external foundry clients (e.g., NVIDIA, AWS) and internal products like Sierra Forest and Granite Rapids.

- Chiplet-based designs become industry standard, with UCIe (Universal Chiplet Interconnect Express) enabling cross-vendor integration.

- Advanced packaging (e.g., TSMC’s CoWoS-R, Intel’s Foveros Direct) faces capacity constraints, leading to a “CoWoS bottleneck” that delays some AI chip rollouts.

Impact: TSMC maintains leadership in advanced nodes and packaging, but Intel narrows the gap via IDM 2.0 strategy.

4. Automotive and Edge AI Drive New Growth Verticals

Key Trend: Semiconductors for EVs, ADAS, and edge computing grow steadily.

- Automotive semiconductor revenue grows ~12% YoY in 2026, led by demand for power management ICs, MCUs, and AI SoCs.

- NVIDIA DRIVE Thor and Qualcomm Snapdragon Ride Flex gain adoption among automakers (e.g., Mercedes, BMW, Xiaomi).

- Edge AI accelerators from companies like Hailo, Groq, and Graphcore, often built on TSMC or GlobalFoundries nodes, are integrated into IoT, robotics, and smart infrastructure.

- Silicon carbide (SiC) and GaN power semiconductors see strong adoption in EVs and renewable energy systems, benefiting Wolfspeed, Infineon, and STMicroelectronics.

Impact: Diversification into automotive and edge computing reduces reliance on consumer electronics.

5. Memory Market Recovery and AI-Driven Demand

Key Trend: DRAM and NAND rebound due to AI server demand and inventory normalization.

- AI training clusters require massive memory capacity, boosting demand for HBM4 (High Bandwidth Memory).

- SK Hynix, Samsung, and Micron are in full production of HBM4, with TSMC’s CoWoS enabling integration with AI GPUs.

- DDR5 and LPDDR5X adoption accelerates in PCs and mobile, driven by AI PCs and large language model (LLM) edge inference.

- NAND pricing stabilizes after 2025 oversupply, with strong demand for enterprise SSDs in AI data centers.

Impact: Memory suppliers benefit from AI tailwinds, with SK Hynix particularly strong due to exclusive HBM supply to NVIDIA.

6. Sustainability and Regulatory Pressures Intensify

Key Trend: Environmental, Social, and Governance (ESG) standards shape investment and operations.

- Semiconductor firms face increasing pressure to reduce carbon footprint, especially in energy-intensive fabs.

- TSMC and Intel invest in renewable energy and water recycling to meet EU and U.S. sustainability mandates.

- The U.S. SEC climate disclosure rules and EU Corporate Sustainability Reporting Directive (CSRD) require transparent reporting on emissions and supply chain ethics.

- “Green chips” — energy-efficient designs and low-power architectures — gain favor with enterprise customers.

Impact: Operational costs rise slightly, but sustainability becomes a competitive differentiator.

7. Consolidation and Strategic M&A Activity

Key Trend: Big players acquire niche innovators to bolster AI, automotive, and IP portfolios.

- Broadcom acquires VMware-adjacent infrastructure software firms to enhance data center solutions.

- NVIDIA strengthens its AI software stack through targeted acquisitions in AI inference optimization.

- Intel acquires smaller RISC-V or edge AI startups to diversify beyond x86.

- TSMC remains largely acquisitive in equipment and materials, not chip design.

Impact: M&A fuels innovation but raises antitrust scrutiny, especially in the U.S. and EU.

Conclusion: H2 2026 Outlook for the Biggest Semiconductors

| Company | Key Strengths in H2 2026 | Strategic Challenges |

|—————|—————————————————-|——————————————|

| TSMC | 2nm leadership, CoWoS capacity, AI foundry dominance | Packaging bottlenecks, geopolitical risk |

| NVIDIA | AI GPU monopoly, HBM4 integration, software moat | Competition from custom ASICs, regulation |

| Intel | 18A node progress, foundry clients, AI chips | Execution risk, legacy business drag |

| Samsung | Memory leadership, GAA node development | Foundry yield issues, smartphone slowdown|

| Broadcom | Networking ASICs, AI infrastructure, strong cash flow | Dependence on a few large customers |

Final Takeaway

In H2 2026, the semiconductor industry is defined by AI supremacy, geopolitical realignment, and technological convergence. The biggest players are investing aggressively in advanced nodes, packaging, and vertical integration to maintain leadership. While challenges around capacity, regulation, and competition persist, companies that master the AI transition and global supply chain complexity are poised to lead the next era of computing.

Winner of H2 2026: TSMC and NVIDIA, due to their symbiotic dominance in AI chip manufacturing and design, respectively.

Common Pitfalls in Sourcing the Biggest Semiconductor (Quality, IP)

When sourcing high-performance or cutting-edge semiconductors—especially from leading manufacturers—companies often face significant challenges related to quality assurance and intellectual property (IP) protection. Overlooking these aspects can result in product failures, legal disputes, and reputational damage. Below are key pitfalls to avoid:

Quality-Related Pitfalls

1. Assuming Brand Reputation Guarantees Consistent Quality

Relying solely on a supplier’s market leadership or reputation without conducting independent quality audits is risky. Even top-tier semiconductor manufacturers may have variations across production lines or foundries. Without rigorous incoming inspection and qualification processes, substandard or out-of-spec components can enter the supply chain.

2. Inadequate Supply Chain Transparency

The largest semiconductor companies often use third-party subcontractors or offshore assembly and test (OSAT) facilities. Lack of visibility into these secondary suppliers can lead to quality inconsistencies, counterfeit risks, or non-compliance with industry standards (e.g., AEC-Q100 for automotive).

3. Skipping Long-Term Reliability Testing

Focusing only on initial performance metrics without stress testing for thermal cycles, voltage fluctuations, or long-term endurance can result in field failures. High-volume applications (e.g., automotive, industrial) demand extensive reliability data that may not be provided upfront.

4. Overlooking Lot Traceability and Process Control

Without full wafer-level traceability and real-time process monitoring, identifying the root cause of defects becomes difficult. Leading suppliers should provide detailed lot histories and statistical process control (SPC) data—failure to request this increases quality risks.

IP-Related Pitfalls

1. Ambiguous IP Ownership in Custom Designs

When sourcing application-specific integrated circuits (ASICs) or semi-custom chips, unclear contracts may leave IP rights undefined. Suppliers might retain rights to design methodologies or reusable IP blocks, limiting your ability to switch vendors or modify designs.

2. Insufficient Protection Against Reverse Engineering

High-value semiconductor designs are prime targets for cloning. Failing to implement contractual safeguards, such as non-disclosure agreements (NDAs) and secure design handoff protocols, increases the risk of IP theft—especially when working with global foundries.

3. Unverified Compliance with Licensing Agreements

Many advanced chips incorporate third-party IP (e.g., ARM cores, SerDes interfaces). Sourcing without verifying that the supplier has proper licenses can expose your company to infringement claims, even if unintentional.

4. Inadequate Control Over Firmware and Software Stack

For system-on-chip (SoC) solutions, the accompanying firmware, drivers, and SDKs often contain critical IP. Suppliers may restrict access or updates, creating long-term dependency and limiting differentiation in end products.

Mitigation Strategies

To avoid these pitfalls, implement a robust sourcing strategy that includes:

– Independent quality validation and audit rights in supplier agreements

– Clear IP clauses defining ownership, usage rights, and audit provisions

– Multi-source qualification where feasible to reduce dependency

– Regular cybersecurity and IP risk assessments throughout the product lifecycle

Proactively addressing quality and IP concerns ensures reliable performance and protects innovation when sourcing the most advanced semiconductors.

Logistics & Compliance Guide for Biggest Semiconductor

This guide outlines the essential logistics and compliance protocols for Biggest Semiconductor, a global leader in semiconductor manufacturing. Adherence to these standards ensures operational efficiency, regulatory compliance, and supply chain resilience across international markets.

Supply Chain Structure and Network Design

Biggest Semiconductor operates a highly integrated global supply chain encompassing raw material sourcing, wafer fabrication, assembly, testing, and final delivery. The logistics network is structured around regional hubs in North America, Asia-Pacific, and Europe, each aligned with local manufacturing sites and key customer clusters. Strategic partnerships with tier-1 logistics providers ensure end-to-end visibility and scalability. Dual sourcing and geographically diversified manufacturing reduce dependency risks and support just-in-time (JIT) delivery models.

Transportation and Warehousing Management

All shipments—ranging from high-purity raw materials to finished integrated circuits—must comply with industry-specific handling standards. Temperature-controlled and electrostatic discharge (ESD)-safe transportation is mandatory for sensitive components. Air freight is prioritized for high-value, time-sensitive deliveries, while ocean freight is used for bulk, non-critical shipments. Warehousing facilities are certified to ISO 14001 and ISO 45001 standards, with real-time inventory tracking via RFID and WMS integration. Safety stock levels are dynamically managed using predictive analytics to balance inventory costs with service-level agreements.

Export Controls and Trade Compliance

Biggest Semiconductor strictly adheres to international export control regulations, including the U.S. Export Administration Regulations (EAR), EU Dual-Use Regulation, and Wassenaar Arrangement guidelines. All products are classified with appropriate Export Control Classification Numbers (ECCNs), and export licenses are obtained for controlled technologies. An automated export compliance system screens customers, end-users, and destinations against denied and restricted party lists (e.g., BIS, OFAC, EU Consolidated List). Employee training on export compliance is mandatory annually, with special certification for global sales and logistics teams.

Import Compliance and Customs Clearance

Regional compliance officers oversee import activities in each major market. All shipments include accurate Harmonized System (HS) codes, commercial invoices, packing lists, and certificates of origin. Preferential trade agreements (e.g., USMCA, RCEP) are leveraged to minimize duty liabilities. Automated customs brokerage platforms streamline clearance and ensure audit readiness. Internal audits are conducted quarterly to verify adherence to local customs laws, including valuation, origin determination, and post-clearance obligations.

Environmental, Health, and Safety (EHS) Compliance

All logistics operations follow strict EHS protocols aligned with OSHA, REACH, RoHS, and TSCA regulations. Hazardous materials (e.g., photoresists, solvents) are transported in accordance with IATA, IMDG, and ADR standards. Spill response plans and emergency contact information are maintained at all facilities. Carbon footprint tracking is implemented across the logistics network, with targets for emissions reduction aligned with the company’s net-zero roadmap. Sustainable packaging and reverse logistics for equipment recycling are mandatory practices.

Data Security and IT Compliance

Logistics data systems are protected under ISO/IEC 27001 and NIST cybersecurity frameworks. Supply chain data, including shipment details and customer information, is encrypted in transit and at rest. Access controls follow the principle of least privilege, with multi-factor authentication required for logistics platforms. Third-party logistics providers must undergo cybersecurity audits and sign data processing agreements compliant with GDPR and CCPA.

Regulatory Audits and Continuous Improvement

Biggest Semiconductor conducts bi-annual internal compliance audits across all logistics functions. External audits by regulatory bodies (e.g., BIS, CBP, EU Commission) are supported with full documentation and corrective action plans. A centralized compliance dashboard tracks key performance indicators (KPIs), including on-time delivery, customs clearance time, compliance incident rates, and audit findings. Lessons learned are integrated into continuous improvement initiatives, ensuring alignment with evolving global trade regulations and industry best practices.

Incident Response and Contingency Planning

A global supply chain risk management team oversees contingency planning for logistics disruptions (e.g., port closures, geopolitical events, natural disasters). Business continuity plans include alternate routing, buffer inventory at strategic locations, and pre-qualified backup carriers. Any compliance-related incident (e.g., export violation, customs seizure) triggers an immediate investigation, root cause analysis, and reporting to relevant authorities within required timeframes. Escalation protocols ensure executive oversight for high-risk events.

In conclusion, sourcing from the world’s largest semiconductor manufacturers offers significant advantages in terms of technological leadership, production scalability, reliability, and global supply chain integration. Companies such as Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, and Intel dominate the industry with cutting-edge fabrication processes, substantial R&D investments, and robust quality control systems. Partnering with these industry leaders ensures access to advanced semiconductor solutions, reduces risk of supply disruption, and supports innovation in end applications across sectors like consumer electronics, automotive, telecommunications, and artificial intelligence.

However, challenges such as geopolitical dependencies, supply chain constraints, and high demand must be carefully managed. Diversifying sourcing strategies, fostering long-term partnerships, and investing in supply chain visibility are essential to mitigate risks. Ultimately, aligning with top-tier semiconductor manufacturers not only enhances product performance and competitiveness but also positions businesses to adapt to the rapidly evolving technological landscape.