The global steel manufacturing industry remains a cornerstone of industrial development, with a market size valued at approximately USD 1.3 trillion in 2023 and projected to grow at a compound annual growth rate (CAGR) of 4.5% through 2030, according to Grand View Research. Driven by rising infrastructure investments, urbanization, and increasing demand from the automotive and construction sectors—particularly in Asia-Pacific—steel production continues to consolidate among a select group of industry giants. As technological advancements and sustainability initiatives reshape operational efficiencies, the top manufacturers are leveraging economies of scale, vertical integration, and innovation to maintain competitive advantage. Based on production volume, revenue, and global market influence, the following eight companies represent the largest steel producers worldwide, collectively accounting for a significant share of the global output, which exceeded 1.9 billion metric tons in 2023 (Mordor Intelligence).

Top 8 Biggest Steel In The World Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Biggest Steel In The World

2026 Market Trends for the World’s Largest Steel Producers

As the global steel industry navigates a complex landscape of economic, environmental, and technological shifts, the world’s largest steel companies—such as China Baowu Steel Group, ArcelorMittal, Nippon Steel, HBIS Group, and Shagang Group—are poised to face both significant challenges and transformative opportunities by 2026. Key market trends shaping their strategies include decarbonization, digital transformation, regional demand shifts, and supply chain resilience.

Decarbonization and Green Steel Initiatives

By 2026, environmental regulations and corporate sustainability commitments will heavily influence the operations of top steel producers. The push for net-zero emissions is accelerating investment in green steel technologies. Leading firms are expected to scale up hydrogen-based direct reduced iron (DRI) and carbon capture, utilization, and storage (CCUS) projects. China Baowu and ArcelorMittal have already announced pilot plants, and by 2026, early commercial outputs from such facilities will begin impacting supply chains. Regulatory pressure from the EU’s Carbon Border Adjustment Mechanism (CBAM) will further drive decarbonization, especially for exporters.

Digitalization and Smart Manufacturing

The integration of AI, IoT, and advanced analytics into steel production will be mainstream by 2026. The biggest steelmakers are investing heavily in smart factories that optimize energy use, predict maintenance needs, and improve yield rates. For example, Nippon Steel and Baowu are deploying digital twins to simulate blast furnace operations, reducing downtime and emissions. These digital advancements will enhance operational efficiency and provide a competitive edge in cost and responsiveness.

Shifting Global Demand Patterns

Demand for steel in 2026 will be uneven across regions. While construction and infrastructure in India and Southeast Asia are expected to drive growth, China’s domestic steel demand may plateau or slightly decline due to slower urbanization and property sector adjustments. In contrast, North America and Europe will see steady demand fueled by infrastructure modernization and the energy transition—requiring high-strength and specialized steels for wind turbines, EVs, and grid development. Top producers will adjust their production footprints and export strategies accordingly.

Consolidation and Strategic Partnerships

To achieve economies of scale and share R&D costs—especially for green technology—further consolidation and cross-border partnerships are anticipated by 2026. Joint ventures between major players, such as those seen between ArcelorMittal and Japan’s Nippon Steel, may become more common to co-develop low-carbon production methods or secure access to raw materials like high-grade iron ore and green hydrogen.

Supply Chain Resilience and Raw Material Security

Geopolitical tensions and trade policies will continue to influence raw material access. The largest steel companies are expected to vertically integrate or secure long-term contracts for coking coal, iron ore, and scrap metal. Recycling and scrap-based electric arc furnace (EAF) steelmaking will gain traction, especially in regions with mature steel cycles like Europe and North America, reducing reliance on virgin materials and cutting emissions.

In conclusion, by 2026, the world’s biggest steel producers will be defined not just by volume, but by their ability to innovate sustainably, adapt to regional markets, and lead the transition to a low-carbon future. Success will hinge on strategic agility, technological adoption, and collaboration across the value chain.

Common Pitfalls When Sourcing the Biggest Steel in the World (Quality, IP)

Sourcing the largest or highest-capacity steel products—such as massive steel beams, plates, coils, or custom-fabricated components—presents unique challenges, especially concerning quality assurance and intellectual property (IP) protection. As global demand for heavy-duty steel increases across infrastructure, energy, and industrial sectors, companies must navigate several critical pitfalls to avoid costly delays, legal disputes, and compromised structural integrity. Below are key areas of concern:

Quality Assurance Challenges

One of the most significant risks when sourcing large-scale steel is ensuring consistent and verifiable quality. The bigger the steel component, the more critical it is that it meets exacting standards.

- Inconsistent Material Certification: Suppliers may provide inadequate or falsified mill test certificates (MTCs), leading to the use of substandard steel in critical applications.

- Non-Compliance with International Standards: Large steel products must adhere to standards such as ASTM, EN, JIS, or ISO. Failure to verify compliance can result in structural failures.

- Insufficient Third-Party Inspections: Skipping independent inspections (e.g., by SGS, BV, or TÜV) increases the risk of receiving materials with hidden defects like internal voids, improper alloy composition, or poor weld integrity.

- Transport and Handling Damage: Massive steel components are prone to warping, corrosion, or mechanical damage during shipping and handling, especially if not properly packaged or supported.

Intellectual Property Risks

When sourcing custom-engineered or proprietary steel solutions, especially from international suppliers, intellectual property exposure becomes a major concern.

- Design Theft and Reverse Engineering: Sharing technical drawings, CAD files, or specifications with overseas manufacturers can lead to unauthorized replication or sale of your designs.

- Lack of Legal Recourse in Certain Jurisdictions: Many large steel producers are located in countries with weak IP enforcement, making it difficult to pursue legal action if designs are copied.

- Unprotected Tooling and Molds: Custom molds or dies used in steel fabrication may be duplicated without consent, undermining competitive advantage.

- Ambiguous Contractual Terms: Contracts that fail to clearly assign IP ownership or restrict secondary use of designs leave companies vulnerable to exploitation.

Mitigation Strategies

To avoid these pitfalls:

- Require full traceability and certification for all steel batches.

- Conduct pre-shipment inspections and material testing.

- Use non-disclosure agreements (NDAs) and clearly define IP ownership in contracts.

- Partner with reputable suppliers with verifiable track records and certifications.

- Consider regional sourcing or joint ventures to maintain control over sensitive technology.

By proactively addressing quality and IP concerns, businesses can safely leverage the capabilities of the world’s largest steel producers without compromising integrity or innovation.

Logistics & Compliance Guide for the World’s Biggest Steel Producer

As the largest steel manufacturer globally, operating at an immense scale across multiple continents requires a meticulously structured logistics and compliance framework. This guide outlines the key components necessary to maintain efficiency, regulatory adherence, and sustainability in transporting raw materials, intermediate products, and finished steel goods worldwide.

Supply Chain Network Design

Optimizing the supply chain is critical for minimizing costs and maximizing responsiveness. The world’s biggest steel producer must manage a complex network integrating mining operations, processing plants, distribution centers, and customer delivery points.

- Global Sourcing Strategy: Secure long-term contracts with iron ore, coal, and scrap suppliers in Australia, Brazil, South Africa, and other key regions to ensure raw material continuity.

- Integrated Production Hubs: Locate primary steelmaking facilities near ports or rail corridors to streamline inbound logistics and outbound distribution.

- Regional Distribution Centers (RDCs): Establish RDCs near high-demand markets (e.g., Asia-Pacific, Europe, North America) to reduce lead times and transportation costs for finished products.

Transportation & Freight Management

Efficient movement of bulk materials and finished steel products demands a multimodal transportation strategy.

- Bulk Shipping for Raw Materials: Utilize Capesize and Panamax vessels for cost-effective transport of iron ore and coking coal across oceans. Coordinate with port terminals for rapid unloading and stockyard management.

- Rail and Barge for Domestic Movement: Leverage dedicated rail lines and inland waterways to transport raw materials to plants and finished coils, slabs, and beams to regional hubs.

- Last-Mile Delivery Solutions: Partner with certified logistics providers for road transport of finished goods, especially for just-in-time delivery to automotive, construction, and manufacturing clients.

- Fleet Optimization & Tracking: Implement GPS-enabled fleet management systems and real-time cargo tracking to enhance visibility and reduce delays.

Regulatory Compliance & Trade Controls

Operating across jurisdictions requires strict adherence to international, national, and local regulations.

- Customs & Import/Export Compliance: Maintain accurate Harmonized System (HS) codes for all steel products and raw materials. Ensure timely submission of customs documentation (e.g., commercial invoices, packing lists, certificates of origin).

- Anti-Dumping & Safeguard Duties: Monitor trade policies in key markets (e.g., U.S., EU, India) to avoid penalties related to dumping investigations. Maintain transparent pricing and production cost records.

- Export Controls: Comply with regulations on dual-use materials and technology transfers, particularly in high-strength or specialized steel grades.

- Sanctions Screening: Conduct regular screening of trading partners against OFAC, EU, UN, and other sanctions lists to prevent illicit transactions.

Environmental, Health, and Safety (EHS) Standards

Steel production is energy-intensive and poses environmental and safety challenges that must be proactively managed.

- Emissions Reporting & Carbon Compliance: Adhere to regional carbon pricing mechanisms (e.g., EU Emissions Trading System). Monitor and report CO₂, SOₓ, and NOₓ emissions accurately.

- Hazardous Materials Handling: Follow OSHA (U.S.), REACH (EU), and GHS guidelines for transporting and storing hazardous substances such as acids, lubricants, and slag byproducts.

- Waste Management & Recycling: Implement circular economy practices by recycling steel scrap and managing slag for use in construction materials.

- Transport Safety Protocols: Enforce secure loading/unloading procedures for heavy and sharp steel products. Use certified containers and protective packaging to prevent damage and injury.

Quality Assurance & Product Certification

Global customers demand consistent product quality backed by recognized certifications.

- International Standards Compliance: Ensure products meet ISO 9001 (quality management), ISO 14001 (environmental management), and ISO 45001 (occupational health and safety).

- Industry-Specific Certifications: Obtain certifications such as API (for pipeline steel), ABS (shipbuilding), and EN 10025 (structural steel) as required by end-user sectors.

- Traceability Systems: Implement batch tracking from raw material input to final delivery using digital systems (e.g., blockchain or ERP-integrated logs) for full product traceability.

Risk Management & Business Continuity

Given the scale of operations, robust risk mitigation strategies are essential.

- Supply Chain Resilience: Diversify suppliers and logistics routes to reduce dependency on single sources or chokepoints (e.g., Suez Canal, Malacca Strait).

- Geopolitical Risk Monitoring: Track political instability, trade wars, and regulatory shifts in operating regions. Adjust sourcing and routing accordingly.

- Disaster Recovery Plans: Develop contingency plans for natural disasters, port closures, and cyberattacks on logistics systems.

- Insurance Coverage: Maintain comprehensive cargo, liability, and business interruption insurance across the logistics chain.

Digitalization & Technology Integration

Leveraging digital tools enhances efficiency, visibility, and compliance.

- Integrated Logistics Platforms: Use enterprise resource planning (ERP) and transportation management systems (TMS) to coordinate global shipments and inventory.

- Predictive Analytics: Apply AI to forecast demand, optimize routing, and prevent bottlenecks in port or rail operations.

- Electronic Data Interchange (EDI): Automate customs filings, shipping notices, and invoicing with trading partners and carriers.

- Blockchain for Compliance: Pilot blockchain solutions for tamper-proof documentation of origin, carbon footprint, and chain of custody.

Conclusion

For the world’s biggest steel producer, logistics and compliance are not standalone functions but strategic enablers of global competitiveness. By integrating robust transportation networks with rigorous regulatory adherence and advanced digital systems, the company can maintain operational excellence, meet customer expectations, and uphold its environmental and social responsibilities across every link of the supply chain.

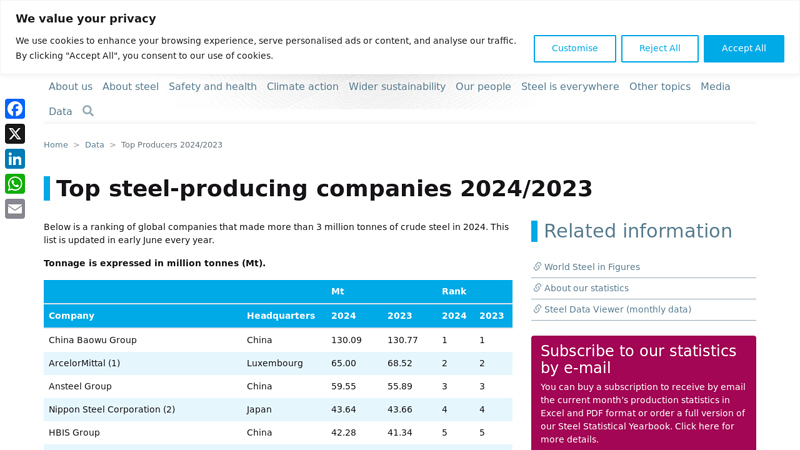

In conclusion, identifying the largest steel manufacturer in the world reveals that China Baowu Steel Group currently holds the top position, both in terms of production volume and global influence. As a result of strategic mergers, technological advancements, and strong government support, China Baowu has consistently surpassed international competitors, producing over 130 million metric tons of steel annually. Its dominance underscores China’s pivotal role in the global steel industry.

When sourcing steel from the world’s leading manufacturer, businesses benefit from economies of scale, reliable supply chains, and access to a wide range of high-quality steel products. However, considerations such as geopolitical factors, trade regulations, environmental standards, and logistics must be carefully evaluated. Diversifying suppliers while maintaining partnerships with industry leaders like China Baowu can ensure a balanced, resilient sourcing strategy in a competitive and evolving market.