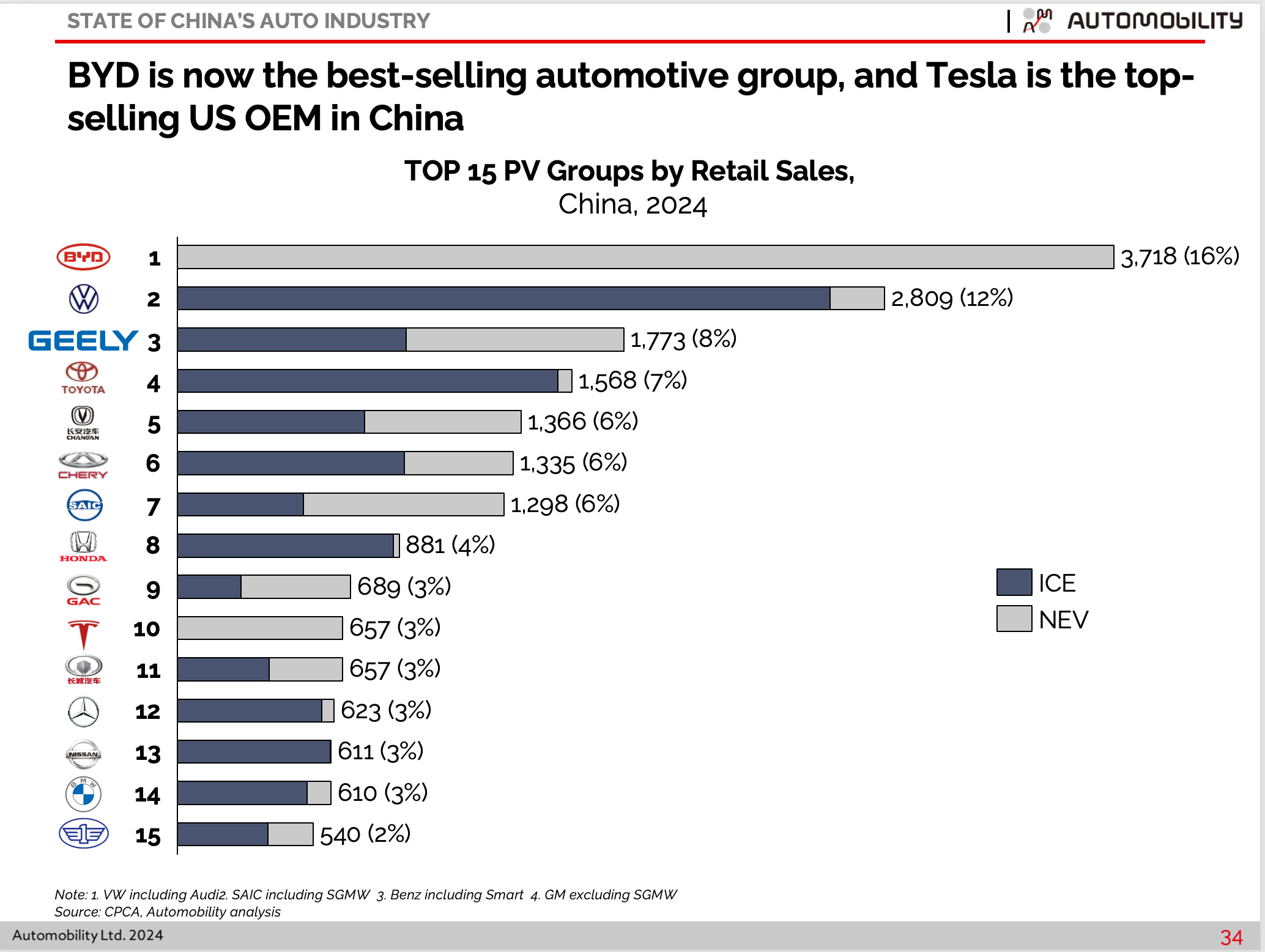

China remains the world’s largest automotive market, with passenger vehicle sales reaching approximately 21 million units in 2023, according to Mordor Intelligence. Fueled by rising urbanization, expanding middle-class demand, and robust government support for new energy vehicles (NEVs), the Chinese auto market is projected to grow at a CAGR of around 5.2% from 2024 to 2030. As of 2023, NEVs accounted for over 35% of total vehicle sales, a share expected to surpass 50% by 2027, reshaping the competitive landscape among manufacturers. This shift has elevated domestic brands and joint ventures alike, redefining market leadership. Based on annual sales volume, the following list details the top 10 car manufacturers in China, reflecting both legacy strength and adaptability in an increasingly electrified and tech-driven industry.

Top 10 Car Sales In China By Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Car Sales In China By

2026 Market Trends for Car Sales in China

Electric Vehicle (EV) Dominance Accelerates

By 2026, electric vehicles are projected to account for over 50% of total car sales in China, solidifying the country’s position as the world’s largest EV market. This shift is driven by aggressive government policies, including extended subsidies, stringent emissions regulations, and local incentives for EV adoption. Chinese automakers such as BYD, NIO, and Xpeng are expected to maintain strong momentum, capturing domestic market share while expanding exports. Battery technology advancements, particularly in solid-state and sodium-ion batteries, will improve range and reduce costs, further boosting consumer demand.

Intensified Competition and Market Consolidation

The Chinese automotive market will witness heightened competition between domestic champions and international brands attempting to adapt. While joint ventures like SAIC-Volkswagen and FAW-Toyota remain significant, their market share is likely to decline as homegrown EV brands gain favor. Smaller EV startups without sustainable business models may face consolidation or exit, leading to a more streamlined industry structure dominated by a few integrated players offering vehicles, software, and energy solutions.

Rise of Intelligent and Connected Features

By 2026, advanced driver-assistance systems (ADAS) and connected car technologies will become standard in mid-to-high-end models. Features such as over-the-air (OTA) software updates, AI-powered voice assistants, and partial autonomous driving (L2+/L3) will serve as key differentiators. Chinese tech giants like Huawei and Baidu, through partnerships and their own intelligent vehicle platforms (e.g., Huawei’s HarmonyOS in Car), will play a growing role in shaping the in-vehicle experience, further blurring the lines between automakers and tech companies.

Downstream Impact on ICE Vehicles and Supply Chain

Sales of internal combustion engine (ICE) vehicles are expected to continue a steady decline, influenced by tightening fuel efficiency standards and city-level restrictions on ICE registrations. This transition will pressure traditional suppliers, prompting a shift toward electrified components and software integration. The domestic battery supply chain, already robust with leaders like CATL and BYD, will expand to meet growing demand, supported by government-backed mineral sourcing strategies, including lithium mining investments abroad.

Regional and Demographic Shifts

Lower-tier cities and rural areas will become increasingly important growth engines due to rising disposable incomes and improved charging infrastructure. Affordable EVs priced between RMB 100,000–150,000 will dominate sales volume in these regions. Meanwhile, premium EVs targeting urban professionals will emphasize luxury, performance, and cutting-edge technology. Additionally, younger consumers’ preference for digital-first purchasing experiences will push OEMs to enhance online sales platforms and direct-to-consumer models.

Export Growth and Global Influence

China is poised to become the world’s largest auto exporter by 2026, with EVs comprising a significant share of overseas shipments. Key markets include Southeast Asia, Europe, Latin America, and the Middle East, where Chinese brands offer competitively priced, high-specification vehicles. Trade dynamics, such as EU anti-subsidy investigations, may pose challenges, but localization strategies—including planned European production facilities—will help mitigate risks and strengthen global foothold.

Policy and Infrastructure Support

Government initiatives will continue to underpin market growth. The 14th Five-Year Plan’s focus on new energy vehicles (NEVs) and smart mobility will drive investment in charging networks, with over 20 million public and private charging points expected by 2026. Support for vehicle-to-grid (V2G) integration and battery-swapping infrastructure will further enhance the EV ecosystem, improving convenience and reducing range anxiety for consumers.

Common Pitfalls Sourcing Car Sales in China by Quality and Intellectual Property (IP)

Sourcing car sales in China—whether for parts, vehicles, or related services—can present significant opportunities, but it also comes with unique challenges related to quality control and intellectual property (IP) protection. Below are common pitfalls businesses encounter in these two critical areas.

1. Inconsistent Quality Standards Across Suppliers

One of the most prevalent issues when sourcing cars or automotive components from China is the variability in product quality. While China hosts world-class manufacturers, many smaller or less-regulated suppliers may not adhere to international quality benchmarks.

- Lack of Standardization: Chinese suppliers may follow GB (Guobiao) standards, which can differ significantly from ISO, SAE, or other international automotive standards.

- Hidden Defects: Components may pass basic inspections but fail under real-world conditions due to substandard materials or poor assembly.

- Inadequate Testing: Some suppliers conduct minimal or no performance, safety, or durability testing, increasing the risk of product failure post-purchase.

To mitigate this, businesses must implement rigorous third-party quality audits, require detailed certifications, and conduct pre-shipment inspections.

2. Misrepresentation of Product Specifications and Origins

Suppliers may misrepresent the origin, grade, or performance of automotive parts or vehicles. For example:

– Selling refurbished or used parts as new.

– Claiming OEM (Original Equipment Manufacturer) quality without authorization.

– Falsifying documentation such as material test reports or compliance certificates.

This misrepresentation not only affects product reliability but also exposes the buyer to legal and reputational risks.

3. Weak Enforcement of Intellectual Property Rights

China has made strides in IP legislation, but enforcement remains inconsistent, especially in the automotive sector where counterfeit parts and reverse-engineered designs are common.

- Counterfeit Components: Unauthorized duplication of branded automotive parts (e.g., sensors, ECUs, lighting systems) is widespread and difficult to trace.

- Design and Patent Infringement: Chinese manufacturers may replicate patented vehicle designs, software, or technology without permission.

- Trademark Violations: Use of logos or branding that mimics well-known automotive brands, leading to consumer confusion and legal liability for distributors.

Buyers risk importing infringing products, which can result in customs seizures, lawsuits, and damage to brand reputation.

4. Lack of IP Clarity in Supplier Agreements

Many sourcing contracts fail to clearly define IP ownership, especially when custom tooling, molds, or software are developed for a project.

- Suppliers may claim ownership of tooling paid for by the buyer.

- Design files or technical data shared with suppliers can be reused or sold to competitors.

- No contractual provisions preventing reverse engineering or unauthorized production.

Without robust IP clauses in contracts, businesses may lose control over proprietary technology and face competition from imitations.

5. Risks Associated with Joint Ventures and Technology Transfer

For companies entering the Chinese market through joint ventures (JVs), there is often pressure to share technology with local partners. This can lead to:

– Unintended IP leakage.

– Development of competing products by former partners.

– Difficulty enforcing confidentiality agreements in local courts.

These risks are particularly acute in the new energy vehicle (NEV) and electric vehicle (EV) sectors, where battery and software technologies are highly valuable.

6. Supply Chain Obfuscation and Subcontracting

Suppliers may outsource production to unauthorized subcontractors to cut costs, leading to:

– Uncontrolled quality deviations.

– Use of non-approved materials or processes.

– Higher risk of IP theft, as technical details are exposed to additional parties.

Without full supply chain transparency, buyers cannot ensure compliance with quality or IP standards.

7. Inadequate Due Diligence on Suppliers

Many sourcing failures stem from insufficient vetting of Chinese partners. Common oversights include:

– Failing to verify business licenses or production capabilities.

– Not checking for past IP disputes or regulatory violations.

– Relying solely on trade show introductions or online marketplaces without on-site audits.

Comprehensive due diligence—including site visits, background checks, and reference verification—is essential to avoid costly mistakes.

Conclusion

To successfully source car sales in China, businesses must proactively address quality and IP risks through stringent supplier vetting, detailed contracts, third-party inspections, and robust IP protection strategies. Partnering with local legal and technical experts can further reduce exposure and ensure compliance with both Chinese regulations and international standards.

Logistics & Compliance Guide for Car Sales in China

Navigating the Chinese automotive market requires a deep understanding of both logistical operations and strict regulatory compliance. Success hinges on aligning supply chain strategies with China’s complex legal and administrative framework.

Understanding China’s Automotive Regulatory Landscape

China maintains one of the world’s most tightly regulated automotive markets. Key regulatory bodies include the Ministry of Industry and Information Technology (MIIT), the State Administration for Market Regulation (SAMR), and the Ministry of Ecology and Environment (MEE). All vehicles sold in China must obtain CCC (China Compulsory Certification), proving compliance with safety, environmental, and quality standards. Additionally, new energy vehicles (NEVs) must meet specific technical requirements and be listed on the official NEV Model Catalog to qualify for subsidies and license plate privileges in major cities.

Import Regulations and Customs Clearance

Importing vehicles into China involves stringent customs procedures. Fully Built-Up (CBU) imports are subject to multiple taxes, including a 15% import tariff, value-added tax (VAT) at 13%, and a consumption tax ranging from 1% to 40% depending on engine displacement. All imported vehicles must undergo inspection by the China Inspection and Quarantine (CIQ) authority and obtain the CCC mark before customs release. Accurate documentation—including bill of lading, commercial invoice, packing list, certificate of origin, and CCC certificate—is critical to avoid delays.

Distribution and Logistics Network

Establishing an efficient distribution network is essential for timely vehicle delivery. Most automakers partner with local distributors or establish wholly foreign-owned enterprises (WFOEs) to manage logistics. Key logistics hubs include Shanghai, Guangzhou, Tianjin, and Chongqing. Using bonded logistics centers (BLCs) or free trade zones (FTZs), such as Shanghai’s Lingang area, can streamline import processes and defer tax payments. Just-in-time (JIT) delivery models are common, requiring coordination with regional distribution centers and last-mile transport providers.

Dealer Licensing and Sales Compliance

Selling vehicles in China requires compliance with the Automobile Sales Management Measures issued by the Ministry of Commerce. While the mandatory factory-dealer exclusivity model has been relaxed, automakers must still register their sales channels with local authorities. Dealers must be registered and adhere to standardized sales practices, including transparent pricing and customer rights protection. Online sales are permitted but must be integrated with physical service networks for delivery and after-sales support.

After-Sales Service and Recall Management

Compliance extends beyond the sale. Manufacturers are legally responsible for warranty fulfillment and mandatory recall management. The SAMR oversees vehicle recalls, requiring prompt reporting of safety defects and submission of corrective action plans. A robust after-sales logistics network, including parts warehousing and service center coordination, is vital. All service records must be maintained in accordance with Chinese data localization laws.

Environmental and Data Compliance

China enforces strict emissions standards (China 6) and promotes NEV adoption through quotas and incentives. Automakers must comply with the Dual Credit Policy, which mandates minimum NEV production or credit purchases. Additionally, data generated by connected vehicles falls under China’s Cybersecurity Law and Personal Information Protection Law (PIPL). Data collected from vehicles must be stored within China, and cross-border data transfers require security assessments.

Strategic Recommendations for Market Entry

Foreign automakers should consider joint ventures with local partners to navigate regulatory complexities and qualify for NEV incentives. Investing in local production can reduce logistics costs and import barriers. Partnering with experienced third-party logistics (3PL) providers familiar with automotive regulations ensures compliance throughout the supply chain. Regular engagement with regulatory authorities and continuous monitoring of policy changes are crucial for long-term success in China’s dynamic auto market.

In conclusion, sourcing car sales in China directly through manufacturers offers significant advantages, including access to authentic vehicles, competitive pricing, favorable warranty and after-sales support, and the ability to customize orders according to market demands. As the world’s largest automotive market, China presents immense opportunities for domestic and international buyers alike. Partnering with reputable manufacturers ensures product quality, supply chain transparency, and compliance with national and international standards. However, success in this endeavor requires thorough due diligence, a clear understanding of regulatory frameworks, strong negotiation capabilities, and strategic logistics planning. By leveraging direct manufacturer relationships and staying attuned to evolving market trends—such as the rapid growth of new energy vehicles (NEVs) and smart mobility solutions—businesses can establish a sustainable and profitable foothold in China’s dynamic automotive sector.