Introduction: Navigating the Global Market for EV

The electric vehicle (EV) landscape has shifted from a consumer niche to a critical industrial imperative. While the foundational technology dates back to the 19th century, the modern convergence of high-density lithium battery technology and urgent decarbonization goals has triggered a mass migration away from internal combustion engines. For enterprises in the USA and Europe, electrification is no longer a trend—it is a supply chain necessity.

However, transitioning to an electric fleet involves more than simply swapping fuel pumps for plugs. Stakeholders face a complex ecosystem that extends far beyond passenger cars, encompassing electric trucks, rail systems, marine vessels, and emerging electric aircraft. The challenge for B2B buyers lies in overcoming historical barriers—such as range anxiety and grid reliance—while ensuring that capital investments in new propulsion technologies yield operational efficiency and regulatory compliance.

This guide serves as a strategic roadmap for navigating the evolving EV sector. In the following sections, we will address:

- Market Scope: A breakdown of EV categories, from Class 8 heavy-duty haulers to specialized industrial transport.

- Technological Viability: Evaluating current energy storage capabilities against operational demands.

- Infrastructure & ROI: Strategies for integrating charging networks and maximizing fleet value in a zero-emission economy.

Top 10 Ev Manufacturers & Suppliers List

1. Top 10: EV Manufacturers | EV Magazine

Domain: evmagazine.com

Registered: 2003 (22 years)

Introduction: From BYD and Tesla to Volkswagen and GM, our top 10 charts EV leaders shaping design, scale and charging access while mapping ……

2. The World’s Top EV Makers by Market Share – Visual Capitalist

Domain: visualcapitalist.com

Registered: 2011 (14 years)

Introduction: Key Takeaways · Tesla Holds Nearly Half the U.S. Market · General Motors Grows to 15% Market Share · Ford and Hyundai Battle for Third Place….

Illustrative Image (Source: Google Search)

3. Largest electric vehicle companies by Market Cap

Domain: companiesmarketcap.com

Registered: 2020 (5 years)

Introduction: List of the top EV automakers by market cap. This list only contains companies that manufacture Electric cars, trucks and speciality vehicles….

4. Top 10 global suppliers to the EV market | Supply Chain Magazine

Domain: supplychaindigital.com

Registered: 2007 (18 years)

Introduction: Top 10 suppliers of EV batteries and components to the global electric vehicle market include CATL, DENSO and Bosch….

5. Top 10 Electric Vehicle Manufacturers in the World

Domain: perfectsenseenergy.com

Registered: 2014 (11 years)

Introduction: Top 10 Electric Vehicle Manufacturers in the World · 1. BYD Auto · 2. Tesla, Inc. · 3. Volkswagen Group · 4. General Motors (GM) · 5. BMW Group….

6. Top 10 Electric Car Suppliers & Exporter Companies in USA

Domain: usimportdata.com

Registered: 2022 (3 years)

Introduction: List of Top US Electric Vehicle Suppliers | US Export Data by Company · 1. Tesla Inc. · 2. General Motors · 3. Ford Motor Company · 4. Rivian ……

Illustrative Image (Source: Google Search)

7. Global Top 20 Electric Car Companies [2025]

![Global Top 20 Electric Car Companies [2025]](https://www.sourcifychina.com/wp-content/uploads/2025/12/blackridgeresearchcom-8331.jpg)

Domain: blackridgeresearch.com

Registered: 2019 (6 years)

Introduction: 1. Global Top 20 Electric Car Companies [2025] (ranked based on EV units sold) · 1.1. BYD Co., Ltd. · 1.2. Tesla, Inc. · 1.3. SAIC-GM-Wuling ……

8. Which purely EV company has the most potential of succeeding …

Domain: reddit.com

Registered: 2005 (20 years)

Introduction: Most pure EV companies are on shaky ground. Rivian, Lucid, Vinfast, Fisker. I wouldn’t bet on their future. Polestar would probably be the best….

Understanding ev Types and Variations

Understanding EV Types and Variations

For B2B stakeholders, fleet managers, and sustainability officers, distinguishing between electric vehicle (EV) architectures is critical for calculating Total Cost of Ownership (TCO) and planning infrastructure. While the term “EV” broadly encompasses any vehicle propelled by electricity—from rail systems to warehouse forklifts—the current commercial market focuses on three primary propulsion technologies: Battery Electric (BEV), Plug-in Hybrid (PHEV), and Fuel Cell Electric (FCEV).

The following table outlines the core operational differences, applications, and trade-offs for these vehicle types.

Illustrative Image (Source: Google Search)

Comparative Overview of EV Architectures

| EV Type | Key Features | Primary B2B Applications | Pros & Cons |

|---|---|---|---|

| Battery Electric Vehicle (BEV) | Fully electric propulsion; energy stored in onboard rechargeable batteries (typically Li-ion). No internal combustion engine (ICE). | Last-mile delivery, light-duty fleet sedans, urban public transit, material handling (forklifts). | Pros: Zero tailpipe emissions, lowest TCO (fuel/maintenance), tax incentives. Cons: Range constraints, dependent on charging infrastructure, longer downtime for refueling. |

| Plug-in Hybrid Electric Vehicle (PHEV) | Combines an ICE with a battery and electric motor. Can be charged via grid but operates as a hybrid once the battery is depleted. | Sales fleets covering large territories, executive transport, regions with immature charging grids. | Pros: Eliminates range anxiety, fuel flexibility, lower upfront cost than some BEVs. Cons: Higher maintenance (dual powertrains), still produces emissions, lower all-electric range. |

| Fuel Cell Electric Vehicle (FCEV) | Uses hydrogen gas to generate electricity onboard via a fuel cell stack. Emits only water vapor. | Long-haul Class 8 trucking, heavy-duty municipal transport (buses), continuous-duty industrial ops. | Pros: Fast refueling (comparable to diesel), high energy density for heavy loads, constant power output. Cons: High vehicle cost, scarce hydrogen infrastructure, lower energy efficiency well-to-wheel. |

| Industrial & Micro-Mobility EVs | Low-speed vehicles, often lead-acid or Li-ion powered. Includes carts, e-bikes, and specialized tugs. | Warehousing, corporate campus logistics, urban cargo delivery, facility management. | Pros: High maneuverability, low operational cost, quiet operation indoors. Cons: Limited speed and range, not suitable for highway use. |

1. Battery Electric Vehicles (BEV)

BEVs represent the definitive shift toward electrification. As noted in historical contexts, early adoption was hindered by lead-acid battery limitations. However, modern advancements in lithium-ion technology have significantly improved energy density and current output, making BEVs viable for mass commercial adoption.

- Technical Profile: BEVs rely entirely on the battery pack for propulsion. They utilize regenerative braking to recapture energy, maximizing efficiency in stop-and-go traffic.

- Business Use Case: BEVs are the optimal choice for predictable routes (e.g., urban delivery loops, postal services) where vehicles return to a central depot for overnight charging. They offer the highest potential for meeting strict corporate ESG (Environmental, Social, and Governance) mandates regarding carbon reduction.

2. Plug-in Hybrid Electric Vehicles (PHEV)

PHEVs serve as a bridge technology for businesses operating in regions with fragmented charging infrastructure. Unlike standard hybrids (HEV) which cannot plug in, PHEVs possess a larger battery capable of 20–50 miles of pure electric driving before the gasoline engine engages.

- Technical Profile: Dual powertrain system (electric motor + ICE).

- Business Use Case: Ideal for mixed-use fleets. For example, a service technician can drive emission-free within a city’s “Low Emission Zone” (common in European markets) but utilize the combustion engine for inter-city travel without downtime for charging.

3. Fuel Cell Electric Vehicles (FCEV)

While less common in the passenger sector, FCEVs are gaining traction in heavy industry. FCEVs address the “energy density” challenge that heavy batteries pose for long-haul transport.

- Technical Profile: Converts compressed hydrogen gas into electricity on-demand. This powers the motor and charges a small buffer battery.

- Business Use Case: Heavy-duty logistics. For Class 8 trucks (semis) hauling maximum payloads, the weight of a battery required for a 500-mile range can be prohibitive. Hydrogen offers a lighter weight-to-energy ratio and refueling times (10–15 minutes) that align with current logistics schedules, minimizing driver downtime.

4. Commercial and Industrial Variations

Beyond standard road vehicles, electrification is mature in specialized B2B sectors:

* Material Handling: Electric forklifts and pallet jacks are industry standards in warehousing due to the requirement for zero emissions in enclosed spaces.

* Last-Mile Micro-Mobility: E-bikes and electric cargo trikes are increasingly used for urban logistics to bypass traffic congestion and parking constraints.

* Mass Transit: Electric rail (trams, monorails) and battery-electric buses are broadly deployed to reduce municipal noise pollution and improve air quality.

Illustrative Image (Source: Google Search)

Key Industrial Applications of ev

Key Industrial Applications of Electric Vehicles (EVs)

The electrification of transport has expanded beyond passenger automobiles into critical industrial sectors. Driven by advancements in lithium-ion battery density and high-output electric motors, commercial entities in the USA and Europe are rapidly integrating EVs to meet decarbonization mandates and optimize fleet operations.

The following table outlines the primary industrial sectors currently deploying electric propulsion technologies.

| Industry Sector | Vehicle Types | Key Applications |

|---|---|---|

| Logistics & Freight | Class 8 Electric Trucks (e.g., Tesla Semi), Light Commercial Vans | Long-haul freight transport, middle-mile logistics, and last-mile urban delivery. |

| Public Transportation | Battery Electric Buses (BEB), Trams, Monorails | Municipal mass transit, inter-city commuting, and airport shuttle services. |

| Maritime & Shipping | Electric Ferries, Tugs, Submersibles | Short-sea shipping, port operations, passenger transport, and underwater infrastructure inspection. |

| Aviation & Aerospace | Fixed-wing Electric Aircraft, Multirotors (Drones) | Short-haul cargo, pilot training, aerial surveillance, and emerging urban air mobility solutions. |

| Warehousing & Material Handling | Electric Carts, Forklifts, AGVs | Indoor material transport, campus logistics, and automated inventory movement. |

| Rail Transport | Electric High-Speed Trains, Light Rail | High-volume passenger and freight movement utilizing overhead lines or electrified rails. |

Strategic Benefits for Industrial Adopters

For B2B decision-makers, the transition to electric propulsion offers distinct operational advantages over internal combustion engines (ICE).

1. Reduced Total Cost of Ownership (TCO)

While the initial capital expenditure (CapEx) for industrial EVs can be higher, the operational expenditure (OpEx) is significantly lower.

* Maintenance: Electric motors possess far fewer moving parts than diesel or gasoline engines, eliminating the need for oil changes, transmission flushes, and exhaust system repairs.

* Fuel Costs: Electricity prices generally offer greater stability and lower cost-per-mile compared to volatile fossil fuel markets.

Illustrative Image (Source: Google Search)

2. Regulatory Compliance and ESG Goals

Strict environmental regulations in the European Union (e.g., the Green Deal) and the United States (e.g., EPA standards) are phasing out ICE vehicles.

* Zero-Emission Zones: EVs grant access to Ultra Low Emission Zones (ULEZ) in major cities where diesel vehicles face heavy fines or bans.

* Decarbonization: Deploying EVs directly contributes to Scope 1 emission reductions, essential for meeting corporate Environmental, Social, and Governance (ESG) targets.

3. Operational Efficiency and Performance

Modern battery technologies provide the energy density required for heavy-duty cycles, while electric motors offer performance benefits unavailable in ICE vehicles.

* Instant Torque: Electric motors deliver maximum torque instantly, ideal for heavy haulage and frequent stop-start operations typical in logistics and transit.

* Noise Reduction: The inherent quietness of electric propulsion allows for night-time deliveries and operations in noise-sensitive residential areas without violating municipal ordinances.

4. Energy Independence and Grid Integration

Industrial fleets can leverage onsite renewable energy generation (solar/wind) to charge vehicles, insulating operations from grid fluctuations. Furthermore, Vehicle-to-Grid (V2G) technology allows fleets to sell stored energy back to the grid during peak demand, turning cost centers into revenue generators.

3 Common User Pain Points for ‘ev’ & Their Solutions

3 Common User Pain Points for EV Adoption & Their Solutions

As businesses in the USA and Europe transition toward electrification—ranging from commercial fleets to logistics—decision-makers face distinct operational hurdles. While the technology has evolved significantly since the early 20th century, the shift from Internal Combustion Engines (ICE) to electric propulsion presents specific challenges regarding range, infrastructure, and asset management.

1. Operational Range Anxiety and Route Logistics

Scenario: A logistics company operating Class 8 electric trucks (similar to the Tesla Semi mentioned in reference) or a municipal transit authority managing electric buses needs to maintain tight delivery schedules and uptime.

The Problem: Despite improvements in energy density, “range anxiety” remains a critical barrier. Unlike ICE vehicles which can refuel in minutes anywhere, EVs rely on energy storage capacities that fluctuate based on load weight, terrain, and weather conditions. For B2B operators, running out of power isn’t just an inconvenience; it is a disruption to the supply chain and a direct revenue loss.

The Solution:

* Advanced Telematics & Route Optimization: Implement AI-driven fleet management software that calculates range based on real-time battery health, cargo weight, and topography.

* Opportunity Charging: Utilize high-power DC fast-charging during scheduled loading/unloading windows rather than relying solely on overnight depot charging.

* Vehicle Selection: Procure vehicles utilizing modern lithium battery chemistries that offer superior energy density compared to legacy lead-acid technologies.

2. Scalability of Charging Infrastructure

Scenario: A corporate campus or fleet depot is transitioning a fleet of light-duty electric cars (e.g., BMW i3) and requires simultaneous charging for 50+ vehicles.

Illustrative Image (Source: Google Search)

The Problem: While a single vehicle can charge from a “standard electrical outlet” or dedicated wall box, scaling this to a fleet level creates massive strain on local grid capacity. Businesses often face high capital expenditures for upgrades and “demand charges” from utility providers if peak energy usage is not managed.

The Solution:

* Smart Charging Management Systems (CMS): Deploy software that balances energy loads, prioritizing vehicles that need immediate dispatch while throttling others to prevent grid overload.

* Microgrids & Storage: Integrate on-site renewable energy (solar) and stationary battery storage to offset grid reliance during peak pricing hours.

* Infrastructure-as-a-Service (IaaS): Partner with third-party providers who finance and maintain the charging hardware, shifting the cost from CapEx to OpEx.

3. Technology Obsolescence and Asset Lifespan

Scenario: A shipping company is investing in electric boats or a logistics firm is purchasing a fleet of electric vans.

The Problem: The source notes rapid “technological advancement in lithium batteries.” B2B buyers worry that vehicles purchased today will suffer from rapid depreciation or that battery degradation will render the asset unusable long before the chassis wears out. Unlike ICE vehicles with established resale values, the long-term residual value of EV assets is harder to predict.

Illustrative Image (Source: Google Search)

The Solution:

* Modular Battery Architecture: Invest in platforms that allow for battery module replacement or upgrades without replacing the entire vehicle.

* Battery Leasing/Swapping: Adopt a “Battery-as-a-Service” model where the battery is leased separately from the vehicle, transferring the degradation risk to the supplier.

* Second-Life Applications: Develop protocols for repurposing degraded vehicle batteries for stationary energy storage, recovering residual value at the end of the vehicle’s lifecycle.

Strategic Material Selection Guide for ev

Strategic Material Selection Guide for EVs

The transition from Internal Combustion Engines (ICE) to Electric Vehicles (EVs) represents more than a change in propulsion; it requires a fundamental overhaul of the Bill of Materials (BOM). As historical constraints regarding “range anxiety” and energy storage limitations are addressed through technological advancements, OEM and Tier 1 suppliers must prioritize materials that balance energy density, thermal efficiency, and supply chain resilience.

For the US and European markets, where regulatory compliance and range expectations are highest, material selection strategies must focus on three core vectors: Energy Storage, Structural Lightweighting, and Propulsion Efficiency.

1. Energy Storage Systems: Beyond Legacy Chemistry

While early electric mobility utilized lead-acid batteries, the modern EV sector relies heavily on Lithium-ion architectures to achieve the energy density required for mass adoption.

Illustrative Image (Source: Google Search)

- Cathode Materials (NMC vs. LFP):

- Nickel Manganese Cobalt (NMC): Offers high energy density, making it the standard for long-range passenger vehicles in the US and EU. However, volatility in cobalt pricing and ethical sourcing concerns are driving research into low-cobalt variations.

- Lithium Iron Phosphate (LFP): Gaining traction for commercial fleets and entry-level EVs due to lower costs, higher thermal stability, and longer cycle life, despite lower energy density compared to NMC.

- Anode Innovation: The shift from pure graphite anodes to silicon-doped graphite is critical for increasing charge rates and capacity, directly addressing the historical barrier of “range anxiety.”

2. Structural Lightweighting

To offset the significant weight of battery packs (often 25-30% of vehicle mass), material substitution in the chassis and body-in-white (BIW) is essential.

- Aluminum Alloys: Extensively used in battery enclosures and crash management systems due to high strength-to-weight ratios.

- Advanced High-Strength Steel (AHSS): Remains dominant in structural cages where cost-efficiency and crash safety are paramount.

- Carbon Fiber Reinforced Polymer (CFRP): While historically limited to luxury segments (e.g., early BMW i3), advancements in manufacturing are making composites viable for specific structural reinforcements to maximize range efficiency.

3. Propulsion and Power Electronics

The efficiency of the electric motor and inverter dictates the vehicle’s overall energy consumption.

- Rare Earth Elements (Neodymium/Dysprosium): Essential for Permanent Magnet Synchronous Motors (PMSM), offering superior torque density. Supply chain centralization remains a critical risk factor for Western manufacturers.

- Silicon Carbide (SiC): Replacing Silicon (Si) in inverters. SiC semiconductors allow for higher switching frequencies and operating temperatures, significantly improving range and charging speeds.

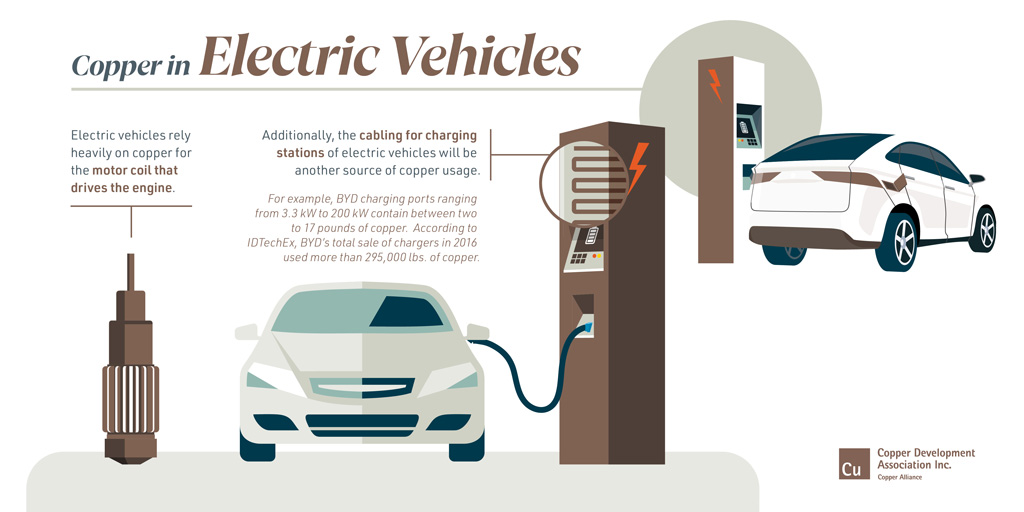

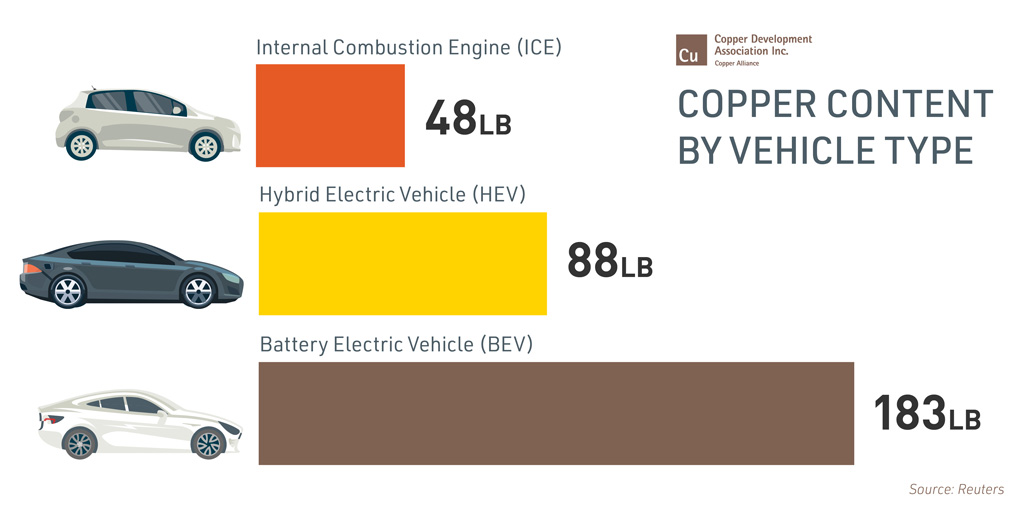

- Copper: EVs require up to 4x the copper of ICE vehicles. High-purity copper is non-negotiable for stator windings and high-voltage cabling to minimize resistance losses.

Comparative Analysis of Strategic Materials

The following table compares key materials based on cost implications, performance impact, and supply chain risk profile for Western markets.

| Material Category | Material Type | Primary Application | Cost Profile | Performance Impact | Supply Chain Risk (US/EU) |

|---|---|---|---|---|---|

| Battery | NMC (Lithium-ion) | Long-range Passenger EVs | High | High Energy Density | High (Cobalt dependency) |

| Battery | LFP (Lithium-ion) | Commercial/Budget EVs | Low | High Durability / Safety | Medium (Refining capacity) |

| Structure | Aluminum 6000 Series | Battery Trays / Body Panels | Medium-High | Significant Weight Reduction | Low |

| Structure | AHSS (Steel) | Safety Cage / Chassis | Low | High Crash Safety | Low |

| Structure | CFRP | Roofs / Reinforcement | Very High | Maximum Weight Reduction | Medium |

| Propulsion | Neodymium | PMSM Motors | High | High Torque / Efficiency | Very High (Geopolitical) |

| Electronics | Silicon Carbide (SiC) | Inverters / Chargers | High | Increased Range / Fast Charging | Medium (Capacity scaling) |

| Conductor | Copper | Wiring / Windings | Medium | Electrical Efficiency | Medium (Demand surge) |

In-depth Look: Manufacturing Processes and Quality Assurance for ev

In-depth Look: Manufacturing Processes and Quality Assurance for EVs

The production of Electric Vehicles (EVs) represents a paradigm shift from traditional Internal Combustion Engine (ICE) manufacturing. While the fundamental chassis assembly shares similarities with legacy automotive processes, the integration of high-voltage battery packs, electric drivetrains, and complex thermal management systems requires specialized workflows.

For B2B stakeholders in the USA and Europe, understanding these phases is critical for supply chain alignment and regulatory compliance.

1. Manufacturing Lifecycle: From Raw Material to Final Assembly

The EV manufacturing process is distinctively divided into battery cell production and vehicle integration. The workflow generally follows three critical phases: Preparation, Forming, and Assembly.

Phase 1: Material Preparation and Mixing

Before physical components are shaped, raw materials must undergo rigorous processing to ensure energy density and structural integrity.

- Battery Chemistry: The process begins with the mixing of electrode slurries. Active materials (lithium, nickel, manganese, cobalt) are mixed with conductive additives and binders to create a homogeneous slurry for cathodes and anodes. Precision in this phase is vital to prevent dendrite formation and ensure battery longevity.

- Chassis Materials: Lightweighting is a priority for EV range efficiency. Manufacturers prepare high-strength steel and aluminum alloys for body-in-white (BIW) structures.

Phase 2: Component Forming and Cell Fabrication

This phase involves the physical shaping of core components.

- Electrode Coating and Calendering: The prepared slurry is coated onto metal foils (copper for anodes, aluminum for cathodes). These are dried and compressed (calendered) to increase energy density.

- Cell Assembly: The coated electrodes are stacked or wound (depending on form factor: cylindrical, prismatic, or pouch), electrolyte is injected, and the cells are sealed.

- Gigacasting: Many leading EV OEMs are adopting “gigacasting” for the vehicle chassis—casting large sections of the vehicle underbody as a single piece to reduce part counts and manufacturing time.

Phase 3: General Assembly and Integration

The convergence of the “skateboard” platform (battery and drivetrain) with the vehicle body.

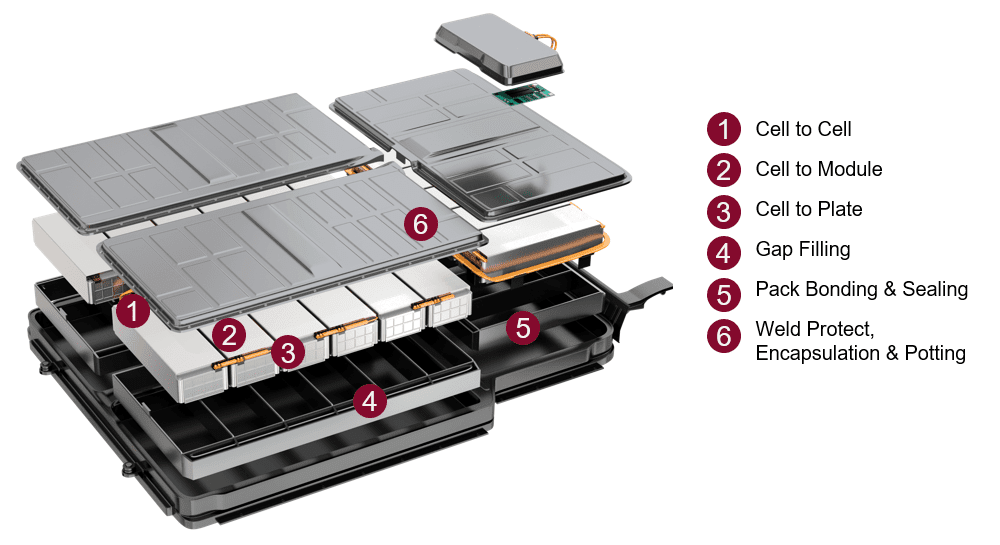

- Module and Pack Assembly: Individual cells are grouped into modules, which are then assembled into a battery pack. This stage includes the installation of the Battery Management System (BMS), busbars, and thermal cooling plates.

- Marriage (Decking): The defining moment in EV assembly where the completed body is lowered onto the powertrain chassis (battery pack and electric motors).

- Fluid Fill and EOL: Unlike ICE vehicles requiring oil and fuel, EVs require specialized dielectric coolants for thermal management systems and brake fluids.

2. Quality Control (QC) and Assurance

Given the high voltage nature of EVs (400V to 800V architectures), QC protocols are stricter than traditional automotive standards.

- Automated Optical Inspection (AOI): Used during electrode coating to detect micron-level defects or contaminants that could cause internal short circuits.

- X-Ray Inspection: Utilized to inspect internal cell alignment and weld quality within battery modules without destructive testing.

- Leak Testing: Critical for liquid cooling systems within the battery pack. Any coolant leakage can lead to thermal runaway; therefore, helium leak testing is standard.

- End-of-Line (EOL) Testing: Includes verifying BMS communication, high-voltage isolation testing, and drive cycle simulation to ensure the vehicle meets range and performance parameters.

3. Regulatory Standards and Compliance (USA & Europe)

To operate in Western markets, manufacturers must adhere to rigorous ISO and IEC standards focusing on safety, quality management, and environmental impact.

| Standard | Focus Area | Relevance to B2B Supply Chain |

|---|---|---|

| IATF 16949 | Quality Management | The global technical specification for quality management systems in the automotive industry. Mandatory for Tier 1 suppliers. |

| ISO 26262 | Functional Safety | Addresses safety-critical risks in electrical and electronic systems. Essential for BMS and autonomous driving features. |

| ISO 6469 | Electrical Safety | Specifies safety requirements for electrically propelled road vehicles, focusing on protection against electric shock. |

| UN 38.3 | Transport Safety | Required certification for transporting lithium batteries. Essential for logistics and supply chain movement across borders. |

| ISO 15118 | Charging Communication | Defines the communication interface between the vehicle and the grid (V2G), crucial for charging infrastructure compatibility in the EU and USA. |

Conclusion

For suppliers and stakeholders, success in the EV sector requires a dual focus: adhering to legacy automotive rigor (IATF 16949) while mastering the specific chemical and electrical safety standards (ISO 26262, ISO 6469) introduced by electrification.

Illustrative Image (Source: Google Search)

Practical Sourcing Guide: A Step-by-Step Checklist for ‘ev’

Practical Sourcing Guide: A Step-by-Step Checklist for Electric Vehicles (EVs)

Sourcing electric vehicles (EVs) for commercial fleets, industrial use, or resale requires rigorous due diligence. Unlike internal combustion engine (ICE) vehicles, EVs present unique challenges regarding battery chemistry, charging infrastructure compatibility, and hazardous material logistics.

Use this checklist to streamline the procurement process for the US and European markets.

Phase 1: Requirement Definition & Technical Specifications

Before engaging suppliers, define the specific operational parameters. The wide range of EVs—from micromobility (e-bikes) to Class 8 trucks—dictates different technical standards.

- Define Vehicle Classification: Clarify if the unit is for on-road use (passenger/freight), off-road industrial use (forklifts/carts), or micromobility.

- Select Battery Chemistry:

- Lithium-Ion (Li-ion/LiFePO4): Standard for modern EVs due to high energy density. Required for long-range and weight-sensitive applications.

- Lead-Acid/AGM: Acceptable only for low-cost, low-speed, or heavy industrial applications where weight is not a constraint.

- Establish Range & Payload Metrics:

- Calculate required range based on “real-world” loaded conditions, not just unladen manufacturer estimates.

- Factor in climate control energy consumption (HVAC reduces range significantly).

- Charging Infrastructure Compatibility:

- USA: J1772 (AC), CCS1 (DC Fast Charge), or NACS (Tesla).

- Europe: Type 2 (Mennekes) and CCS2.

- Note: Ensure the On-Board Charger (OBC) voltage matches the destination grid (110V/220V vs. 230V/400V).

Phase 2: Regulatory Compliance & Certification

Importing non-compliant EVs into the USA or Europe can result in seizure at customs or liability lawsuits. Verify these certifications immediately.

Illustrative Image (Source: Google Search)

| Region | Component | Required Standard/Certification |

|---|---|---|

| USA | Whole Vehicle | FMVSS (NHTSA), EPA (Certificate of Conformity) |

| USA | Battery | UL 2271 (Light EV), UL 2580 (Auto), UN 38.3 (Transport) |

| Europe | Whole Vehicle | WVTA (Whole Vehicle Type Approval), CE Marking (Micromobility) |

| Europe | Battery | UNECE R100 (Safety), RoHS, REACH, Battery Directive 2006/66/EC |

| Global | Shipping | MSDS (Material Safety Data Sheet) for HazMat transport |

Phase 3: Supplier Verification & Quality Assurance

The complexity of the Electric Drivetrain (battery + motor + controller) requires high manufacturing precision.

- Audit the Battery Management System (BMS):

- Request documentation on the BMS provider. The BMS is critical for preventing thermal runaway.

- Verify over-charge, over-discharge, and short-circuit protection protocols.

- Motor Sourcing:

- Confirm if the motor is AC Induction or PM Synchronous (preferred for efficiency).

- Check the IP Rating (Ingress Protection) of the motor and battery pack (minimum IP67 recommended for outdoor vehicles).

- Supply Chain Validation:

- Identify the cell manufacturer (e.g., CATL, Panasonic, LG, or generic). Branded cells offer higher reliability and safety.

- Verify the supplier’s export history to Western markets to ensure familiarity with quality expectations.

Phase 4: Logistics & After-Sales Strategy

Shipping EVs involves Class 9 Dangerous Goods regulations due to lithium batteries.

- Logistics Planning:

- Ensure the freight forwarder is certified to handle UN 3480/3481 (Lithium ion batteries).

- Confirm packaging complies with IATA/IMDG regulations to prevent transit damage.

- Warranty & Spare Parts:

- Negotiate a warranty that specifically covers battery degradation (e.g., warranty valid until capacity drops below 80%).

- Secure a “spare parts kit” with the initial order (controllers, chargers, and BMS units are high-failure items).

- Confirm software diagnostic tools are included or available for local maintenance teams.

Comprehensive Cost and Pricing Analysis for ev Sourcing

Here is a comprehensive cost and pricing analysis for EV sourcing, tailored for a B2B audience in the USA and Europe.

Comprehensive Cost and Pricing Analysis for EV Sourcing

Sourcing Electric Vehicles (EVs) requires a fundamental shift in procurement strategy compared to Internal Combustion Engine (ICE) vehicles. While the Wikipedia source notes that early EVs failed due to “limited energy storage,” modern sourcing is defined by the economics of advanced lithium-ion technology.

Illustrative Image (Source: Google Search)

For B2B buyers in the USA and Europe, understanding the cost composition—heavily skewed toward materials rather than mechanical assembly—is critical for negotiation and budget forecasting.

1. Component Cost Breakdown

Unlike traditional vehicles where the engine and transmission constitute the bulk of complexity, the EV cost structure is dominated by the battery pack and software integration.

| Cost Category | Approx. % of Total Unit Cost | Key Drivers |

|---|---|---|

| Battery Pack | 30% – 40% | Lithium, Cobalt, Nickel commodity prices; Cell manufacturing; BMS (Battery Management Systems). |

| Powertrain & Electronics | 15% – 20% | Inverters, electric motors (AC/DC), semiconductor availability, wiring harnesses. |

| Chassis & Body | 20% – 25% | Lightweight materials (Aluminum, Carbon Fiber) used to offset battery weight. |

| Labor & Assembly | 10% – 15% | Simplified assembly (fewer moving parts) vs. ICE, but higher specialized labor rates for high-voltage systems. |

| Logistics & Indirect | 10% – 15% | Hazardous material shipping (batteries), tariffs, and compliance testing. |

Materials: The Battery Premium

As highlighted in the reference material, the revival of EVs is driven by “technological advancement in lithium batteries.” Consequently, raw materials are the primary volatility factor in pricing.

* Cathode Chemistry: Sourcing vehicles utilizing Nickel-Manganese-Cobalt (NMC) batteries typically commands a premium due to higher energy density.

* Commodity Exposure: Procurement teams must track indices for Lithium Carbonate and Cobalt, as fluctuations here directly impact Tier 1 supplier pricing.

Labor: R&D vs. Assembly

While the physical assembly of an EV is often more automated and less labor-intensive than an ICE vehicle (due to the absence of complex transmissions and exhaust systems), the amortized R&D cost is significantly higher. Manufacturers pass on the costs of software development and platform engineering to the buyer.

Illustrative Image (Source: Google Search)

Logistics: The “Class 9” Factor

Shipping EVs or replacement battery packs entails strict regulatory compliance.

* Hazmat Classification: Lithium-ion batteries are classified as Class 9 Dangerous Goods. This requires specialized packaging, labeling, and certified carriers, increasing freight costs by 20–40% compared to standard automotive parts.

* Weight: EVs are significantly heavier than their ICE counterparts, reducing the number of units per shipping container or truckload, further driving up per-unit logistics costs.

2. Strategic Cost-Saving Tips for Procurement

To mitigate the high upfront capital expenditure (CapEx) associated with EV fleets or inventory, buyers should employ the following strategies:

-

Leverage Battery Chemistry Alternatives:

For fleets operating on defined, shorter routes (e.g., last-mile delivery vans or municipal buses), specify Lithium Iron Phosphate (LFP) batteries. LFP batteries are generally cheaper than NMC, have a longer cycle life, and do not rely on expensive Cobalt or Nickel, reducing exposure to volatile commodity markets. -

Focus on Total Cost of Ownership (TCO):

Shift the internal procurement metric from “Unit Price” to “TCO.”

Illustrative Image (Source: Google Search)

- Maintenance: EVs have fewer moving parts (no oil changes, spark plugs, or transmission fluid), resulting in 40-60% lower maintenance costs.

- Energy: Electricity costs per mile are generally lower than diesel or gasoline, particularly when charging is managed during off-peak hours.

-

Regional Sourcing & Incentives:

- USA: Leverage the Inflation Reduction Act (IRA) credits by sourcing commercial EVs assembled in North America.

- Europe: Align sourcing with EU sustainability mandates to avoid carbon border taxes. Sourcing locally reduces the high logistics costs associated with heavy battery transport.

-

Unbundle Charging Infrastructure:

Do not bundle vehicle procurement with charger installation from a single OEM without auditing. Sourcing “EV Supply Equipment” (EVSE) separately often yields better pricing and interoperability across different vehicle brands.

Alternatives Analysis: Comparing ev With Other Solutions

Alternatives Analysis: Comparing EV With Other Solutions

For B2B fleet managers and logistics operators, the transition to Electric Vehicles (EVs) represents a shift from over a century of Internal Combustion Engine (ICE) dominance. While advancements in lithium battery technology have solved many historical energy density issues, decision-makers must weigh EVs against established and transitional technologies.

Below is a comparative analysis of EVs against their two primary market alternatives: Internal Combustion Engine (ICE) Vehicles and Hybrid Electric Vehicles (HEVs).

Illustrative Image (Source: Google Search)

Comparative Overview

| Feature | Battery Electric Vehicle (EV) | Internal Combustion Engine (ICE) | Hybrid Electric Vehicle (HEV) |

|---|---|---|---|

| Primary Propulsion | Electric Motor (Battery) | Gasoline / Diesel Engine | ICE + Electric Motor |

| Energy Source | Grid Electricity | Fossil Fuels | Fossil Fuels + Regenerative Braking |

| Tailpipe Emissions | Zero | High (CO2, NOx, Particulates) | Reduced |

| Operating Cost (Fuel) | Low (Electricity tariffs) | High (Volatile fuel markets) | Moderate |

| Maintenance | Low (Fewer moving parts) | High (Complex mechanical systems) | High (Dual powertrain complexity) |

| Noise & Vibration | Minimal | High | Variable |

| Refueling/Charging | Hours (Level 2) to Minutes (DC Fast) | Minutes | Minutes |

Alternative 1: Internal Combustion Engine (ICE)

For roughly 100 years, gasoline and diesel engines have been the standard for commercial transport due to high energy density and rapid refueling infrastructure.

- The Case for ICE: The primary advantage of ICE remains operational flexibility. Diesel trucks and vans do not suffer from “range anxiety”—a historical hindrance to EV adoption cited in early automotive history. For long-haul logistics in regions with sparse charging infrastructure, ICE remains the default solution.

- The Case Against ICE: The Total Cost of Ownership (TCO) is increasingly favoring EVs. ICE vehicles have significantly higher maintenance requirements due to thousands of moving parts (transmissions, exhaust systems, cooling). Furthermore, regulatory pressure in the USA and Europe (such as Low Emission Zones) is phasing out ICE access to urban centers, creating a compliance risk for businesses relying solely on fossil fuels.

Alternative 2: Hybrid Electric Vehicles (HEV)

Hybrids utilize both an internal combustion engine and an electric motor, serving as a bridge technology between traditional fossil fuel reliance and full electrification.

- The Case for HEV: Hybrids mitigate the range limitations of current battery technology while offering better fuel economy than pure ICE vehicles. They do not require plug-in infrastructure (unless they are PHEVs), allowing fleets to reduce carbon footprints without altering operational routes or installing depot chargers.

- The Case Against HEV: From a maintenance perspective, Hybrids are the most complex option, as they contain both an internal combustion engine and an electric powertrain. Unlike EVs, which offer the quietness and vibration-free operation inherent to electric motors, Hybrids still generate noise and require fossil fuel. Most critically, they are not “zero-emission vehicles,” meaning they may eventually face similar regulatory exclusions as standard ICE vehicles in strict jurisdiction zones.

Strategic Implication

While ICE vehicles offer immediate familiarity and Hybrids provide a transitional safety net, the B2B trajectory favors full EVs. The superior energy efficiency of electric motors and the long-term reduction in OpEx—driven by lower energy costs and reduced maintenance—position EVs as the superior long-term investment for commercial applications.

Essential Technical Properties and Trade Terminology for ev

Essential Technical Properties and Trade Terminology for EVs

To successfully procure Electric Vehicles (EVs) for fleet operations or distribution in the US and European markets, buyers must master specific technical specifications and trade terminology. This section outlines the critical performance metrics and commercial terms required for informed B2B decision-making.

Illustrative Image (Source: Google Search)

Key Technical Properties

When evaluating EVs—ranging from Class 8 trucks to personal micro-mobility solutions—specifications must be analyzed against operational requirements and regional infrastructure compatibility.

1. Battery Chemistry and Capacity

The battery represents the single largest cost component and determinant of vehicle longevity.

* Capacity (kWh): Kilowatt-hours measure the total energy storage. Higher kWh equates to longer range but increased weight.

* Chemistry Types:

* LFP (Lithium Iron Phosphate): Offers higher cycle life (longevity) and thermal safety. Preferred for commercial fleets and heavy-duty cycles where durability outweighs maximum range.

* NMC/NCA (Nickel Manganese Cobalt/Aluminum): Provides higher energy density. Standard in long-range passenger vehicles and performance applications.

* Voltage Architecture: While 400V is standard, 800V architectures are increasingly common in premium B2B assets, allowing for significantly faster charging times and reduced cabling weight.

2. Range Certification Standards

“Range” is variable based on testing protocols. B2B buyers must identify which cycle is quoted to ensure accurate fleet planning.

* EPA (United States): The Environmental Protection Agency cycle. Generally considered the most conservative and realistic reflection of real-world driving conditions.

* WLTP (Europe): The Worldwide Harmonized Light Vehicles Test Procedure. Usually yields higher range estimates than the EPA cycle; standard for EU compliance.

3. Charging Interface and Speed

Compatibility with regional grids is non-negotiable.

* AC Charging (Level 2): Uses the onboard charger. Standard for overnight depot charging.

* EU Standard: Type 2 (Mennekes).

* US Standard: Type 1 (J1772) or NACS (North American Charging Standard).

* DC Fast Charging (Level 3): Bypasses the onboard charger for rapid replenishment (50kW to 350kW+).

* EU Standard: CCS2 (Combined Charging System).

* US Standard: CCS1 or NACS.

* Legacy/Specialized: CHAdeMO (often found in V2G applications).

Illustrative Image (Source: Google Search)

Commercial and Trade Terminology

Navigating the supply chain requires familiarity with manufacturing models and logistics acronyms specific to the automotive and industrial vehicle sectors.

Manufacturing and Design Models

| Term | Definition | B2B Context |

|---|---|---|

| OEM | Original Equipment Manufacturer | The supplier manufactures the vehicle based on their own existing specifications. The buyer purchases the product “as-is” or with minor branding adjustments. |

| ODM | Original Design Manufacturer | The supplier designs and manufactures a vehicle based on the buyer’s unique specifications. Common for specialized industrial EVs or branded micro-mobility fleets. |

| Homologation | Regulatory Approval | The process of certifying that a vehicle meets the regulatory standards of the target market (e.g., FMVSS in the USA, ECE in Europe). Crucial: Non-homologated vehicles cannot be legally registered for public road use. |

Procurement and Logistics Terms

- MOQ (Minimum Order Quantity): The lowest quantity of units a manufacturer will produce per order.

- Relevance: High for custom ODM projects (e.g., 500+ units); lower for standard OEM purchases.

- CKD (Completely Knocked Down): The vehicle is shipped in parts and assembled in the destination country.

- Relevance: Often used to bypass high import tariffs on finished vehicles (CBU – Completely Built Unit). Requires local assembly infrastructure.

- SKD (Semi Knocked Down): Partially assembled vehicle kits.

- Relevance: A middle ground between CBU and CKD, offering some tariff benefits with lower assembly complexity.

- BMS (Battery Management System): The electronic system that manages a rechargeable battery (cell balancing, temperature monitoring).

- Relevance: In B2B procurement, a high-quality BMS is the primary indicator of safety and asset lifespan.

- BEV vs. PHEV vs. FCEV:

- BEV: Battery Electric Vehicle (100% electric).

- PHEV: Plug-in Hybrid Electric Vehicle (combines ICE and Battery).

- FCEV: Fuel Cell Electric Vehicle (Hydrogen).

Navigating Market Dynamics and Sourcing Trends in the ev Sector

Navigating Market Dynamics and Sourcing Trends in the EV Sector

The electric vehicle (EV) landscape has evolved rapidly from a niche alternative to a central pillar of modern transportation and logistics strategies. For B2B buyers and fleet managers in the USA and Europe, understanding the historical trajectory and current technological capabilities of EVs is essential for making informed sourcing decisions.

The Evolution of EV Viability

While often viewed as a modern innovation, the electric vehicle originated in the late 19th century. Early adoption was driven by the quiet operation and ease of use compared to early gasoline engines. However, the 20th century saw the dominance of internal combustion engines (ICE) due to “range anxiety” and the limitations of contemporary energy storage.

For modern procurement professionals, the resurgence of the EV sector is not merely a trend but a result of specific technological breakthroughs:

* Battery Chemistry Shift: The transition from lead-acid batteries to lithium-ion technology has been the primary catalyst for mass adoption. Lithium batteries offer superior energy density and current output, solving the historical range limitations that hindered early EVs.

* Propulsion Efficiency: Unlike ICE vehicles, EVs utilize grid electricity or onboard rechargeable batteries to achieve propulsion, offering a simplified drivetrain with fewer moving parts, which translates to reduced maintenance costs for commercial operators.

Scope of Sourcing: Beyond Passenger Cars

Sourcing strategies must account for the diverse range of electrified transport modes available today. The definition of an EV now encompasses any motorized vehicle propelled fully or mostly by electric power. Buyers should segment the market as follows:

| Category | Vehicle Types | Commercial Application |

|---|---|---|

| Road Transport | Electric cars, buses (e.g., BYD), Class 8 trucks (e.g., Tesla Semi), personal transporters. | Fleet management, last-mile delivery, heavy logistics, public transit. |

| Rail & Mass Transit | Electric trains, trams, monorails, trolleybuses. | Urban infrastructure, intercity logistics, passenger transit. |

| Specialized & Marine | Electric boats, submersibles, electric carts. | Maritime logistics, tourism, specialized industrial transport. |

| Aviation | Fixed-wing aircraft, multirotors. | Emerging markets for short-haul cargo and urban air mobility. |

Sustainability and Market Trends

The shift toward EVs is driven by the mandate for zero-emission vehicles. In the US and European markets, where sustainability reporting is increasingly rigorous, the adoption of EVs directly supports corporate ESG (Environmental, Social, and Governance) goals.

Key Sourcing Considerations:

1. Energy Storage Specifications: Sourcing decisions should prioritize battery technology specifications (energy density and cycle life) rather than just vehicle aesthetics.

2. Infrastructure Integration: Unlike the standalone nature of ICE vehicles, EV procurement requires parallel investment in charging infrastructure or grid integration strategies.

3. Legacy vs. Innovation: While road transport is transitioning from ICE, other sectors like rail have utilized overhead line power for decades. The current market trend focuses on bringing battery-electric autonomy to sectors previously reliant on continuous grid connection or diesel power.

Frequently Asked Questions (FAQs) for B2B Buyers of ev

Frequently Asked Questions (FAQs) for B2B Buyers of EVs

1. How is an Electric Vehicle (EV) defined in a commercial context?

According to industry standards, an EV is any motorized vehicle propelled fully or mostly by electric power. For B2B buyers, this definition extends beyond passenger cars to include a wide spectrum of transportation modes utilized in supply chains and logistics, including electric trucks (from delivery vans to Class 8 semis), buses, rail vehicles, and emerging technologies in electric marine and aviation sectors. Power is derived either via grid electricity (overhead lines) or onboard rechargeable batteries.

2. How does the Total Cost of Ownership (TCO) compare between Commercial EVs and Internal Combustion Engine (ICE) vehicles?

While the upfront acquisition cost of EVs is often higher due to battery pricing, the long-term TCO is generally lower for EVs. This is due to two main factors:

* Operational Costs: Electricity is historically less volatile and cheaper per mile than diesel or gasoline in both the US and Europe.

* Maintenance: As noted in historical comparisons, electric motors provide a level of ease of operation not achieved by gasoline engines. They have significantly fewer moving parts, eliminating the need for oil changes, transmission repairs, and exhaust system maintenance.

3. How has battery technology evolved to support heavy-duty commercial use?

Early electric vehicles were hindered by the limited energy storage of lead-acid batteries. However, the shift toward lithium-ion battery technology has been a decisive factor for commercial viability. Lithium batteries offer superior energy density and current output compared to legacy technologies. This advancement allows for the heavier payloads and longer ranges required by commercial trucks and mass transit buses without compromising cargo space.

4. Is “range anxiety” still a significant operational risk for logistics fleets?

Range anxiety—the fear of running out of power before reaching a destination—historically hindered mass adoption. However, for modern B2B applications, this risk is mitigated by:

1. High-density batteries: drastic improvements in energy storage.

2. Predictable routes: Unlike private transport, commercial delivery routes are often fixed, allowing for precise energy management.

3. Infrastructure: The expansion of high-speed charging networks across major US and European freight corridors.

5. What types of commercial EVs are currently available beyond standard fleet cars?

The commercial EV market encompasses a diverse range of vehicle classes:

* Road: Electric trucks (light-duty to semi-trucks), buses (transit and school), and personal transporters for last-mile delivery.

* Rail: Electric trains, trams, and monorails (often powered by overhead lines).

* Specialized: Electric boats/tugs for harbors, electric aircraft (fixed-wing and multirotors) for specialized cargo, and industrial electric carts.

6. What are the infrastructure requirements for transitioning a fleet to electric?

Transitioning requires an assessment of grid electricity capacity at your depots. Unlike ICE vehicles that rely on third-party fuel stations, commercial EVs often require on-site charging infrastructure.

* Level 2 Charging: Suitable for vehicles parked overnight (e.g., delivery vans).

* DC Fast Charging: Necessary for heavy-duty trucks or vehicles with short turnaround times.

* Grid Upgrades: Facilities may need upgraded transformers or software to manage peak load times to avoid high demand charges.

7. How do EVs assist in meeting regulatory compliance in the USA and Europe?

Both the US and the EU are aggressively implementing decarbonization targets. EVs are classified as zero-emission vehicles (at the tailpipe). Adopting EVs helps businesses:

* Comply with Low Emission Zones (LEZ) in European cities.

* Meet strict EPA standards and state-level mandates (such as California’s ACT rule) in the US.

* Fulfill corporate ESG (Environmental, Social, and Governance) goals regarding carbon footprint reduction.

8. Are electric motors reliable enough for high-uptime industrial applications?

Yes. Electric propulsion has been the dominant mechanism for mass transit (trains, trolleybuses) for over a century due to its reliability. Electric motors produce high torque instantly and operate with less vibration and noise than combustion engines. This results in less mechanical wear and tear, leading to higher uptime and vehicle availability for fleet operators.

Strategic Sourcing Conclusion and Outlook for ev

Strategic Sourcing Conclusion and Outlook for EV

The evolution of the Electric Vehicle (EV) sector represents a fundamental shift in global supply chains, moving beyond the century-long dominance of internal combustion engines. For B2B procurement and sourcing leaders in the USA and Europe, the resurgence of EVs—driven by advancements in lithium battery technology and superior energy density—necessitates a robust, diversified sourcing strategy.

Successful strategic sourcing now demands agility across a widening spectrum of modalities. While electric cars and trucks dominate current volume, the outlook indicates rapid electrification in sectors previously reliant on fossil fuels, including marine (electric boats), aerospace (fixed-wing and multirotors), and mass transit.

Key Sourcing Imperatives for the Future

To capitalize on the zero-emission transition, organizations must prioritize:

- Technology Scalability: Securing partners capable of supporting high-current output needs for heavy-duty applications (Class 8 trucks and rail).

- Multi-Modal Versatility: expanding supplier networks to accommodate components for non-road vehicles, such as electric aircraft and submersibles.

- Energy Storage Innovation: Moving beyond legacy lead-acid constraints to secure advanced lithium supply chains that mitigate range anxiety.

As the industry matures, value will define itself not just by the adoption of electric propulsion, but by the resilience and sustainability of the underlying component supply chain.

Important Disclaimer & Terms of Use

⚠️ Important Disclaimer

The information provided is for informational purposes only. B2B buyers must conduct their own due diligence.