Introduction: Navigating the Global Market for pay united wholesale mortgage

In the evolving landscape of international finance, sourcing the right solutions for paying United Wholesale Mortgage (UWM) can pose unique challenges for B2B buyers, particularly those in Africa, South America, the Middle East, and Europe. As businesses increasingly seek reliable mortgage options, understanding the nuances of payment processes, fee structures, and loan servicing becomes critical. This guide is designed to equip international buyers with comprehensive insights into various payment methods, loan types, and the intricacies of the mortgage landscape, empowering them to make informed decisions.

Throughout this guide, we will delve into the types of mortgage products offered by UWM, explore applications suited for diverse business needs, and provide strategies for effectively vetting suppliers. We will also address crucial factors such as cost implications, payment schedules, and the benefits of automatic payment systems. By arming B2B buyers with this information, the guide not only simplifies the decision-making process but also enhances the potential for successful partnerships and transactions in the global market.

With a focus on actionable insights and practical strategies, this resource is tailored for businesses looking to navigate the complexities of mortgage payments and services effectively. Whether you’re a seasoned investor or a new entrant in the market, understanding how to efficiently manage your mortgage payments with UWM can significantly impact your financial health and operational success.

Top 10 Pay United Wholesale Mortgage Manufacturers & Suppliers List

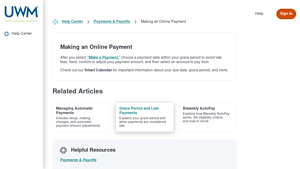

1. United Wholesale Mortgage – Online Payment System

Domain: myuwmloan.com

Registered: 2017 (8 years)

Introduction: United Wholesale Mortgage offers an online payment system that allows users to select a payment date within their grace period to avoid late fees. Users can confirm or adjust their payment amount and select an account to pay from. Additional resources include managing automatic payments, understanding grace periods and late payments, and information on Biweekly AutoPay. Customer support is availab…

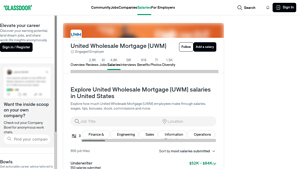

2. United Wholesale Mortgage – Salary Overview

Domain: glassdoor.com

Registered: 2003 (22 years)

Introduction: United Wholesale Mortgage (UWM) offers a range of salaries for various job titles, with the highest-paying position being a Senior Software Developer at approximately $140,476 per year, and the lowest being a Lending Support Specialist at around $50,639 per year. The company has a total of 4,766 salary submissions, with roles spanning across finance, accounting, engineering, sales, information tec…

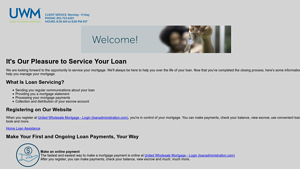

3. United Wholesale Mortgage – Loan Servicing Solutions

Domain: welcome.loanadministration.com

Registered: 1999 (26 years)

Introduction: United Wholesale Mortgage offers loan servicing that includes regular communications about the loan, mortgage statements, processing of mortgage payments, and management of escrow accounts. Customers can register on the UWM website to manage their mortgage, make payments, check balances, and view escrow information. Payment options include online payments, autopay, and mail payments. UWM provides …

Understanding pay united wholesale mortgage Types and Variations

| Type Name | Key Distinguishing Features | Primary B2B Applications | Brief Pros & Cons for Buyers |

|---|---|---|---|

| Standard Monthly Payment | Fixed monthly payments based on loan amount and term | Common for traditional mortgage financing | Pros: Predictable payments; Cons: Less flexibility in payment structure. |

| Biweekly Payment | Payments made every two weeks, resulting in 26 payments/year | Suitable for businesses with steady cash flow | Pros: Reduces interest over time; Cons: Requires consistent cash availability. |

| Automatic Payment (ACH) | Direct debit setup from business accounts | Ideal for businesses seeking convenience | Pros: Ensures timely payments; Cons: Requires account balance management. |

| Interest-Only Payment | Payments cover only interest for a set period | Useful for short-term financing needs | Pros: Lower initial payments; Cons: Principal balance remains unchanged. |

| Graduated Payment | Payments increase over time, ideal for growing businesses | Suitable for startups anticipating growth | Pros: Lower initial payments; Cons: Future payments can become burdensome. |

What Are the Characteristics of Standard Monthly Payments?

Standard monthly payments are the most common structure for mortgage repayments. They involve fixed payments over the loan term, allowing businesses to budget effectively. This payment type is suitable for established companies with predictable cash flows, as it provides stability and certainty. When considering this option, B2B buyers should assess their long-term financial forecasts to ensure they can meet these fixed obligations.

How Do Biweekly Payments Benefit Businesses?

Biweekly payments require businesses to make payments every two weeks, resulting in an extra payment each year. This structure can significantly reduce the total interest paid over the life of the loan, making it an attractive option for companies with consistent cash inflow. However, businesses must ensure they have the liquidity to support this payment schedule, as it can strain finances if not managed properly.

What Are the Advantages of Automatic Payments?

Automatic payments, often set up through an ACH (Automated Clearing House) system, allow businesses to have mortgage payments deducted directly from their bank accounts. This method promotes timely payments and reduces the risk of late fees. For B2B buyers, the convenience of automatic payments is significant, but it requires diligent account management to ensure sufficient funds are available, avoiding overdraft fees.

When Should Businesses Consider Interest-Only Payments?

Interest-only payments are structured so that the borrower pays only the interest for a specified period, usually at the beginning of the loan term. This can be beneficial for businesses seeking to conserve cash in the short term, such as startups or those in transitional phases. However, buyers should be cautious, as the principal balance remains unchanged during this period, leading to larger payments in the future.

How Do Graduated Payments Work for Growing Companies?

Graduated payments start lower and increase at predetermined intervals, making them suitable for businesses expecting growth in revenue. This structure allows companies to manage initial costs while preparing for future financial increases. However, B2B buyers should carefully evaluate their growth projections, as the increasing payment amounts can become a burden if business growth does not materialize as expected.

Key Industrial Applications of pay united wholesale mortgage

| Industry/Sector | Specific Application of pay united wholesale mortgage | Value/Benefit for the Business | Key Sourcing Considerations for this Application |

|---|---|---|---|

| Real Estate Development | Streamlined payment processing for property acquisitions | Reduces transaction times and improves cash flow | Regulatory compliance in different countries, currency exchange rates, and payment security measures. |

| Financial Services | Automated mortgage payment systems for clients | Enhances customer satisfaction and retention | Integration capabilities with existing financial software and local banking regulations. |

| Construction | Financing for construction loans with flexible payment options | Facilitates timely project funding and cost management | Understanding of local market conditions and potential risks in construction timelines. |

| Insurance | Mortgage insurance premium payments through automated systems | Simplifies premium management and ensures timely payments | Knowledge of local insurance regulations and potential currency fluctuations. |

| International Trade | Financing for overseas property investments | Expands investment opportunities and diversifies portfolios | Consideration of international payment methods and transaction fees. |

How is ‘Pay United Wholesale Mortgage’ Applied in Real Estate Development?

In the real estate development sector, ‘pay united wholesale mortgage’ can significantly streamline payment processing for property acquisitions. By facilitating quick and efficient transactions, businesses can reduce the time spent on closing deals, thereby improving cash flow. International buyers, particularly from emerging markets, must consider local regulatory compliance and currency exchange rates, ensuring that payment systems are secure and adaptable to various financial environments.

What Role Does ‘Pay United Wholesale Mortgage’ Play in Financial Services?

For financial services, the automated mortgage payment systems provided by ‘pay united wholesale mortgage’ enhance client experience by ensuring timely payments and reducing administrative burdens. This automation increases customer satisfaction, fostering long-term relationships. B2B buyers in this sector should prioritize integration capabilities with existing financial software and adhere to local banking regulations to ensure seamless operations.

How Does ‘Pay United Wholesale Mortgage’ Support Construction Financing?

In construction, ‘pay united wholesale mortgage’ offers flexible financing options that accommodate the unique payment structures of construction loans. This flexibility allows for better cash flow management and timely project funding, which are crucial for meeting deadlines. International buyers must be aware of local market conditions and potential risks associated with construction timelines to make informed financing decisions.

How is ‘Pay United Wholesale Mortgage’ Utilized in Insurance Premium Management?

The insurance sector benefits from ‘pay united wholesale mortgage’ through automated systems that manage mortgage insurance premium payments. This automation simplifies premium management and ensures that payments are made on time, thus avoiding penalties and lapses in coverage. Buyers should be knowledgeable about local insurance regulations and consider potential currency fluctuations that could impact premium costs.

In What Ways Does ‘Pay United Wholesale Mortgage’ Facilitate International Trade?

In the realm of international trade, ‘pay united wholesale mortgage’ enables financing for overseas property investments, allowing businesses to diversify their portfolios. By providing reliable payment processing, companies can expand their investment opportunities across borders. When sourcing these services, businesses should take into account the international payment methods available and any associated transaction fees to ensure cost-effectiveness.

A stock image related to pay united wholesale mortgage.

3 Common User Pain Points for ‘pay united wholesale mortgage’ & Their Solutions

Scenario 1: Navigating Complex Payment Processes

The Problem: B2B buyers, especially those managing multiple properties or loans, often face difficulties when trying to make payments through the United Wholesale Mortgage (UWM) system. The payment interface can be confusing, particularly for international clients who may not be familiar with U.S. banking practices or mortgage payment protocols. This complexity can lead to errors in payment amounts, missed deadlines, and the potential for late fees, causing frustration and financial strain.

The Solution: To streamline the payment process, it’s essential for buyers to familiarize themselves with the UWM online payment portal. Start by creating a user account on the UWM Servicing Website, where you can manage all aspects of your mortgage. Utilize the “Smart Calendar” feature to set reminders for payment due dates and grace periods, helping to avoid late fees. Additionally, consider enrolling in the Automatic Payment (ACH) program, which allows for monthly payments to be debited directly from your checking or savings account. This not only simplifies the process but also ensures timely payments without the need for manual intervention.

Scenario 2: Understanding Late Payment Policies

The Problem: International buyers may struggle to comprehend UWM’s late payment policies, particularly regarding grace periods and potential penalties. Different countries have varying norms around payment deadlines, and this can lead to misunderstandings. When a payment is not made on time, businesses can incur unexpected charges, affecting their cash flow and overall financial planning.

The Solution: To mitigate the risk of late payments, B2B buyers should take the time to thoroughly review UWM’s policies on late payments and grace periods. This information is typically available on their website under the payments section. Establish a financial calendar that aligns with your payment schedule, including grace periods, to ensure that you are always aware of deadlines. Furthermore, maintain open communication with UWM customer service to clarify any uncertainties around your specific payment terms. By understanding the policies and setting reminders, buyers can avoid unnecessary fees and ensure smooth financial operations.

Scenario 3: Technical Issues with Online Payment Systems

The Problem: Users may encounter technical issues when attempting to log in to the UWM portal, such as trouble with cookies or browser settings that can hinder access to their accounts. These technical difficulties can be particularly challenging for B2B buyers who may be managing multiple accounts or require quick access to payment information. Delays due to technical issues can result in missed payments and subsequent fees, causing operational disruptions.

The Solution: To address potential technical barriers, ensure that your web browser settings allow cookies, as this is a common requirement for accessing UWM’s online services. Before logging in, clear your browser’s cache and ensure that you are using a compatible browser. If issues persist, UWM provides a dedicated customer support line specifically for technical difficulties; don’t hesitate to reach out for assistance. Additionally, consider keeping a backup method for payments, such as manual checks or phone payments, to avoid disruptions. By being proactive about technical requirements and having alternative solutions, buyers can maintain uninterrupted access to their payment systems.

Strategic Material Selection Guide for pay united wholesale mortgage

What Are the Key Materials for Pay United Wholesale Mortgage?

When considering the strategic material selection for payment systems associated with United Wholesale Mortgage (UWM), several materials stand out due to their specific properties and applications. This guide analyzes four common materials, focusing on their key properties, advantages and disadvantages, and implications for international B2B buyers.

What Are the Key Properties of Plastic in Payment Systems?

Plastic materials, particularly high-density polyethylene (HDPE) and polyvinyl chloride (PVC), are widely used in payment systems due to their versatility and cost-effectiveness. These materials exhibit excellent chemical resistance and can withstand a range of temperatures, making them suitable for various environments.

Pros: Plastics are lightweight, easy to manufacture, and can be molded into complex shapes, which is beneficial for creating user-friendly interfaces. They also offer good insulation properties.

Cons: While durable, plastics can be susceptible to UV degradation and may not perform well under extreme temperatures. Additionally, they may not be as environmentally friendly as other materials.

Impact on Application: In payment systems, plastics are often used for cardholders and interface components, ensuring compatibility with various media, including magnetic strips and contactless technology.

Considerations for International Buyers: Compliance with international standards such as ASTM and ISO is crucial. Buyers from regions like Africa and South America may prioritize cost and availability, while those in Europe might focus on sustainability and recyclability.

How Does Metal Compare in Payment Systems?

Metals such as aluminum and stainless steel are commonly used in payment systems for their strength and durability. They provide excellent corrosion resistance and can withstand high temperatures and pressures.

Pros: Metals are highly durable, offering a long lifespan and resistance to wear and tear. They also provide a premium feel, which can enhance customer experience.

Cons: The manufacturing process for metal components can be more complex and costly compared to plastics. Additionally, metals can be heavier, impacting the overall weight of the payment system.

Impact on Application: Metal is often used in the construction of payment terminals and secure enclosures, ensuring robustness and security against tampering.

Considerations for International Buyers: Buyers should consider local regulations regarding metal usage, especially in regions with stringent environmental laws. Compliance with standards like DIN and JIS is also essential.

What Are the Benefits of Glass in Payment Systems?

Glass, particularly tempered or laminated glass, is increasingly used in payment systems for screens and protective covers. It offers excellent clarity and scratch resistance.

Pros: Glass provides a high-end appearance and is easy to clean, which is beneficial for hygiene in high-traffic areas. It also allows for high-resolution displays.

Cons: Glass can be fragile and may require additional support or protective measures to prevent breakage. It is also heavier than plastic alternatives.

Impact on Application: Glass is primarily used in touchscreen interfaces, enhancing user experience while ensuring compatibility with various technologies.

Considerations for International Buyers: Buyers should look for glass that meets safety standards, especially in regions where regulations are strict regarding shatterproof materials.

How Do Composite Materials Enhance Payment Systems?

Composite materials, which combine plastics and metals, are increasingly popular in payment systems. They leverage the strengths of both materials while mitigating weaknesses.

Pros: Composites can be designed to be lightweight yet strong, offering flexibility in design and application. They often provide enhanced thermal and electrical insulation.

Cons: The manufacturing processes for composites can be complex and may lead to higher costs. Additionally, not all composites are recyclable, which can be a concern for environmentally conscious buyers.

Impact on Application: Composites are often used in the structural components of payment systems, providing durability and aesthetic appeal.

Considerations for International Buyers: Understanding the local market’s acceptance of composite materials is vital, especially in regions where traditional materials are preferred.

Summary Table of Material Selection for Pay United Wholesale Mortgage

| Material | Typical Use Case for pay united wholesale mortgage | Key Advantage | Key Disadvantage/Limitation | Relative Cost (Low/Med/High) |

|---|---|---|---|---|

| Plastic | Cardholders, interface components | Lightweight and cost-effective | Susceptible to UV degradation | Low |

| Metal | Payment terminals, secure enclosures | Highly durable and premium feel | Complex manufacturing process | High |

| Glass | Touchscreen interfaces, protective covers | High clarity and easy to clean | Fragile and heavier than plastics | Medium |

| Composite | Structural components in payment systems | Lightweight yet strong | Higher manufacturing costs | Medium |

This guide provides a comprehensive overview of material selection for payment systems associated with United Wholesale Mortgage, helping international B2B buyers make informed decisions tailored to their specific needs and regional considerations.

A stock image related to pay united wholesale mortgage.

In-depth Look: Manufacturing Processes and Quality Assurance for pay united wholesale mortgage

What are the Main Stages in the Manufacturing Process of Pay United Wholesale Mortgage?

In the context of financial services, particularly in wholesale mortgage operations, the “manufacturing” process can be viewed as a systematic flow of activities that ensure the effective delivery of mortgage products and services. This includes several key stages:

-

Material Preparation: This stage involves gathering and processing the necessary documentation and data needed for mortgage applications. Key materials include borrower credit histories, income verification documents, and property appraisals. Ensuring accurate and complete documentation is essential for smooth processing and compliance with regulatory requirements.

-

Forming: In this phase, mortgage applications are formally created and structured. This includes the integration of borrower information into a centralized system, enabling easy access for underwriting and approval processes. Advanced software solutions are often employed to streamline this process, ensuring that data is accurately captured and processed.

-

Assembly: This stage refers to the consolidation of all components necessary for mortgage approval. Underwriters review the assembled information, assessing risk factors and compliance with lending standards. This is a critical phase where decisions are made regarding loan approvals or rejections.

-

Finishing: Once a mortgage is approved, this stage encompasses the finalization of loan documents and the disbursement of funds. It also includes setting up the servicing of the mortgage, which involves ongoing management of the loan account, including payment processing and customer service support.

How is Quality Control Implemented in Wholesale Mortgage Operations?

Quality Control (QC) in the wholesale mortgage sector is vital for maintaining compliance, ensuring customer satisfaction, and minimizing risk. Here are the key elements of QC relevant to this sector:

-

International Standards: Adhering to international quality management standards, such as ISO 9001, is crucial. This standard provides a framework for consistent quality improvement, customer satisfaction, and operational efficiency. Compliance with such standards can reassure international B2B buyers that the processes are robust and reliable.

-

Industry-Specific Standards: In addition to general quality standards, industry-specific regulations and certifications—such as those from the Consumer Financial Protection Bureau (CFPB) and various local lending authorities—play a significant role. Compliance with these guidelines ensures that lending practices are ethical and transparent.

-

Quality Control Checkpoints: Implementing systematic QC checkpoints throughout the mortgage process is essential. These checkpoints include:

– Incoming Quality Control (IQC): Focuses on the quality of materials and documents received from borrowers.

– In-Process Quality Control (IPQC): Involves ongoing assessments during the processing and underwriting stages to ensure adherence to standards.

– Final Quality Control (FQC): Conducts a comprehensive review of all documents and processes before closing the loan.

What Common Testing Methods are Used in Mortgage Quality Control?

Testing methods in mortgage QC are designed to ensure compliance and accuracy throughout the mortgage lifecycle. Some common methods include:

- Document Audits: Regular audits of loan files help verify that all necessary documentation is present and accurate. This is vital for ensuring compliance with lending regulations.

- Underwriting Reviews: Periodic reviews of underwriting decisions can help identify patterns or anomalies that could indicate potential issues in risk assessment.

- Customer Satisfaction Surveys: Gathering feedback from borrowers post-transaction helps gauge the effectiveness of the mortgage process and identify areas for improvement.

How Can B2B Buyers Verify Supplier Quality Control?

For international B2B buyers, especially from regions such as Africa, South America, the Middle East, and Europe, verifying the QC processes of potential mortgage partners is crucial. Here are some actionable strategies:

-

Supplier Audits: Conducting thorough audits of potential suppliers can reveal insights into their QC processes. This includes reviewing their adherence to international standards, internal procedures, and documentation practices.

-

Quality Reports: Requesting detailed quality reports from suppliers can provide transparency into their QC practices. These reports should outline QC metrics, audit results, and corrective actions taken in response to any identified issues.

-

Third-Party Inspections: Engaging third-party quality assurance firms can provide an unbiased assessment of a supplier’s QC processes. These inspections can be particularly valuable for international buyers looking for assurance in unfamiliar markets.

What are the Quality Control and Certification Nuances for International B2B Buyers?

International buyers must navigate various nuances when it comes to QC and certification in the mortgage sector:

- Regulatory Variations: Different countries have distinct regulatory requirements governing mortgage practices. Understanding these nuances is essential for compliance and risk management.

- Cultural Considerations: Cultural differences can impact business practices and expectations regarding quality. B2B buyers should be aware of these factors when assessing potential partners.

- Local Partnerships: Forming alliances with local entities can facilitate better understanding and navigation of local regulations, enhancing the overall quality assurance process.

In summary, the manufacturing processes and quality control measures for pay united wholesale mortgage are critical components for B2B buyers seeking reliable mortgage solutions. By understanding these processes, buyers can make informed decisions and ensure they partner with compliant and quality-focused lenders.

Practical Sourcing Guide: A Step-by-Step Checklist for ‘pay united wholesale mortgage’

In this practical sourcing guide, we outline a structured approach for B2B buyers interested in the payment processes associated with United Wholesale Mortgage (UWM). This checklist aims to facilitate a smooth and informed procurement experience for international buyers, particularly those in Africa, South America, the Middle East, and Europe.

Step 1: Understand Payment Options

Familiarize yourself with the various payment methods offered by UWM. This includes online payments, automatic payments (ACH), and biweekly options. Understanding these choices allows you to select the most convenient and cost-effective method for your organization.

- Online Payments: This option enables you to make payments directly through UWM’s servicing website, providing immediate confirmation.

- Automatic Payments: Setting up automatic payments can help avoid late fees and ensure timely transactions, which is crucial for maintaining good standing.

Step 2: Review Payment Deadlines and Grace Periods

It’s essential to be aware of the payment deadlines and any grace periods provided by UWM. Missing a payment can result in late fees and affect your credit standing.

- Due Dates: Check the due date for payments and mark it on your calendar.

- Grace Periods: Understanding the grace period allows flexibility in case of unforeseen circumstances, helping you avoid penalties.

Step 3: Evaluate Currency and Transfer Fees

As an international buyer, assess the currency exchange rates and any transfer fees associated with making payments. This can significantly impact the total cost of your mortgage payments.

- Exchange Rates: Monitor current rates to choose an optimal time for currency conversion.

- Transfer Fees: Investigate fees from your bank or payment service provider to avoid unexpected costs.

Step 4: Set Up Secure Payment Channels

Ensure that the payment channels you use are secure. This is critical to protect your financial information and prevent fraud.

- Secure Websites: Always use UWM’s official site for transactions and ensure it has an SSL certificate.

- Payment Confirmation: After making a payment, obtain a confirmation receipt for your records.

Step 5: Maintain Accurate Records

Keep meticulous records of all transactions with UWM. This practice can be beneficial for financial management and auditing purposes.

- Transaction History: Regularly check your payment history on the UWM servicing website.

- Documentation: Store receipts and confirmations in a designated folder for easy access.

Step 6: Engage Customer Support When Necessary

Don’t hesitate to reach out to UWM’s customer support for any questions or issues regarding payments. They can provide guidance and resolve concerns efficiently.

- Contact Information: Note the customer service hours and contact methods (phone, email) for prompt assistance.

- Technical Support: If you encounter issues with the online payment portal, reach out to technical support for troubleshooting.

Step 7: Stay Informed on Policy Changes

Regularly check for updates on UWM’s payment policies or any changes in terms and conditions. Staying informed helps avoid surprises that could affect your payment strategy.

- Newsletter Sign-up: Consider subscribing to UWM’s newsletters for the latest news and updates.

- Policy Reviews: Periodically review UWM’s website for any changes to payment procedures or terms.

By following this checklist, B2B buyers can navigate the payment process with United Wholesale Mortgage effectively, ensuring timely and secure transactions while optimizing their overall mortgage management experience.

Comprehensive Cost and Pricing Analysis for pay united wholesale mortgage Sourcing

What Are the Key Cost Components in the Pay United Wholesale Mortgage Process?

When analyzing the cost structure associated with sourcing from United Wholesale Mortgage (UWM), several key components must be considered:

-

Materials: The primary material cost in mortgage sourcing is the financing itself. Rates may vary based on market conditions, borrower qualifications, and loan types. Understanding the interest rates and associated fees is critical for accurate cost forecasting.

-

Labor: This encompasses the personnel involved in loan processing, underwriting, and customer service. Efficient labor management can significantly impact overall costs. Consider the skill levels and expertise required, which may affect pricing.

-

Manufacturing Overhead: Although UWM operates in the financial sector rather than manufacturing, overhead can include technology costs, software licensing for loan management systems, and other administrative expenses. These costs are often indirectly passed on to the buyer.

-

Tooling and Quality Control: In mortgage processing, ‘tooling’ refers to the systems and software used to manage loans. Quality control ensures compliance with regulations and standards, which can incur additional costs but are essential for maintaining service integrity.

-

Logistics: While logistics in mortgage sourcing may not align with traditional definitions, it involves the movement of information and documentation. Timeliness in processing applications and payments is crucial for maintaining borrower satisfaction and minimizing delays.

-

Margin: UWM’s profit margin is influenced by various factors, including market competition, loan volume, and customer retention strategies. Understanding these margins can help buyers negotiate better terms.

How Do Price Influencers Impact Sourcing Decisions with UWM?

Several factors can influence pricing when sourcing from United Wholesale Mortgage:

-

Volume/MOQ: Bulk financing or a higher volume of loans may lead to better rates and terms. For international buyers, understanding minimum order quantities (MOQ) in terms of loan applications can provide leverage during negotiations.

-

Specifications/Customization: Custom loan products tailored to specific markets can affect pricing. Buyers should clearly define their requirements to receive accurate cost estimates.

-

Materials: The choice of financing products (e.g., fixed vs. adjustable-rate mortgages) can influence overall costs. Different products have varying risk profiles, which may be reflected in their pricing.

-

Quality/Certifications: The level of service and compliance with international standards can impact costs. Buyers from regions like Africa and South America should inquire about UWM’s certifications and service quality to ensure they meet local requirements.

-

Supplier Factors: The reputation and reliability of UWM as a supplier can also influence pricing. A well-regarded provider may command a premium, but the assurance of quality service can justify this cost.

-

Incoterms: For international transactions, understanding the Incoterms related to payment processing is essential. This includes who bears the risk and responsibility during the transaction, which can affect overall cost calculations.

What Buyer Tips Can Help Optimize Costs in Sourcing from UWM?

For international B2B buyers, particularly from regions like Africa, South America, the Middle East, and Europe, several strategies can enhance cost efficiency:

-

Negotiation: Engage in active negotiation discussions with UWM representatives. Understanding market conditions and demonstrating commitment can lead to favorable terms.

-

Cost-Efficiency: Focus on the total cost of ownership rather than just the initial price. This includes assessing interest rates, fees, and service quality over the loan’s lifespan.

-

Pricing Nuances: Be aware of regional pricing nuances. Different markets may have varying expectations for loan terms, which can influence how UWM structures its offers.

-

Leverage Relationships: Building a strong relationship with UWM can lead to personalized service and potentially better pricing. Regular communication can also help in understanding upcoming changes in pricing strategies.

Disclaimer for Indicative Prices

It is crucial to note that the prices and cost structures discussed herein are indicative and may vary based on market conditions, loan specifics, and other factors. Always consult with UWM directly to obtain the most accurate and tailored pricing information relevant to your needs.

Alternatives Analysis: Comparing pay united wholesale mortgage With Other Solutions

Exploring Alternatives to Pay United Wholesale Mortgage

In the competitive landscape of mortgage payment solutions, it is essential for international B2B buyers to evaluate various options to determine the best fit for their needs. This analysis will compare ‘Pay United Wholesale Mortgage’ with two viable alternatives: ‘PayPal Business Payments’ and ‘Stripe for Mortgage Payments’. Each solution has its unique features and advantages, making it crucial to consider performance, cost, ease of implementation, maintenance, and best use cases.

| Comparison Aspect | Pay United Wholesale Mortgage | PayPal Business Payments | Stripe for Mortgage Payments |

|---|---|---|---|

| Performance | High reliability for mortgage payments | Fast transactions; widely accepted | High scalability and customization options |

| Cost | No fees for automated payments; standard mortgage fees apply | Transaction fees (2.9% + $0.30 per transaction) | Competitive pricing with volume discounts |

| Ease of Implementation | Simple online setup with mortgage servicing account | Easy integration with existing systems | Requires developer resources for integration |

| Maintenance | Minimal; automated processes reduce manual intervention | Requires account management and fee tracking | Ongoing maintenance for API and feature updates |

| Best Use Case | Ideal for consistent mortgage payments | Suitable for diverse payment needs and online transactions | Best for tech-savvy businesses needing custom solutions |

In-Depth Look at Alternatives

What Are the Advantages and Disadvantages of PayPal Business Payments?

PayPal Business Payments is a well-known solution that allows businesses to send and receive payments easily. Its major advantage is its speed; transactions are processed almost instantly. Additionally, PayPal is widely accepted, making it convenient for businesses with diverse payment needs. However, the transaction fees can accumulate, especially for high-volume transactions, which may not be ideal for businesses primarily focused on mortgage payments.

How Does Stripe for Mortgage Payments Compare?

Stripe is recognized for its robust API, making it an excellent choice for businesses that require custom payment solutions. Its scalability allows businesses to grow without changing platforms, and it provides advanced features such as subscription billing and fraud prevention. However, Stripe typically requires technical expertise for integration, which might be a barrier for businesses lacking in-house development resources. Additionally, ongoing maintenance is necessary to keep the system updated and functional.

Making the Right Choice: Which Payment Solution Is Best for Your Business?

Selecting the right payment solution involves understanding the specific needs of your business and how each option aligns with those requirements. For B2B buyers focused on consistent mortgage payments, ‘Pay United Wholesale Mortgage’ offers streamlined services with minimal fees for automated payments. In contrast, if your business needs flexibility and quick transactions for various payment types, ‘PayPal Business Payments’ may be more suitable. Alternatively, for companies seeking a tailored solution that can grow with them, ‘Stripe for Mortgage Payments’ provides extensive customization but at the cost of requiring technical resources.

Ultimately, the decision should be based on a comprehensive assessment of each alternative’s performance, cost, and operational fit within your existing systems and processes. By carefully evaluating these aspects, international buyers can make informed decisions that enhance their payment processing capabilities and support their business objectives.

Essential Technical Properties and Trade Terminology for pay united wholesale mortgage

What Are the Key Technical Properties of United Wholesale Mortgage Payment Systems?

In the realm of mortgage payments, understanding the essential technical properties associated with United Wholesale Mortgage (UWM) can significantly enhance the efficiency of transactions for international B2B buyers. Here are the critical specifications:

-

Payment Processing Time

This refers to the duration it takes for a payment to be processed and reflected in the mortgage account. Typically, UWM offers real-time processing for online payments, ensuring that funds are applied promptly. For B2B buyers, quick processing times reduce the risk of late fees and improve cash flow management. -

Grace Period

UWM provides a grace period for mortgage payments, allowing borrowers additional time to make payments without incurring late fees. Understanding this period is crucial for international buyers, especially those operating across different time zones, as it can affect payment scheduling and compliance with financial obligations. -

Automatic Payment Options

UWM offers an Automatic Payment (ACH) program, enabling users to set up recurring payments directly from their bank accounts. This feature is particularly beneficial for businesses managing multiple accounts, as it reduces the administrative burden of manual payments and ensures timely transactions. -

Payment Methods Accepted

Understanding the various payment methods accepted by UWM, including online payments, checks, and electronic transfers, is essential for B2B buyers. Each method may have different processing times and fees, impacting financial planning and operational efficiency. -

Mortgage Statements and Reporting

Regular mortgage statements provide detailed insights into payment history, outstanding balances, and escrow accounts. For B2B buyers, leveraging this information can aid in financial reporting and strategic decision-making. -

User Access and Security Features

UWM’s online platform includes robust security measures to protect sensitive payment information. For international buyers, understanding these security protocols is vital to ensure compliance with local regulations and safeguard against fraud.

What Are the Common Trade Terms Related to United Wholesale Mortgage Payments?

Familiarity with industry terminology can facilitate smoother transactions and negotiations. Here are some common terms associated with UWM:

-

OEM (Original Equipment Manufacturer)

While primarily used in manufacturing, in the context of mortgage services, it can refer to the original provider of the software or technology used for payment processing. Understanding OEM relationships can help buyers assess the reliability and support options available. -

MOQ (Minimum Order Quantity)

This term typically applies to product purchases but can also relate to the minimum mortgage amount required for specific loan products. Knowing the MOQ helps B2B buyers gauge their financing options and align them with their business needs. -

RFQ (Request for Quotation)

In the mortgage sector, an RFQ may be used to solicit quotes for specific loan terms or services from UWM. This process is crucial for B2B buyers seeking competitive rates and terms for their financing needs. -

Escrow

Escrow accounts are crucial in mortgage transactions, holding funds for property taxes and insurance. Understanding escrow management is essential for international buyers to ensure compliance with local regulations and to manage cash flow effectively. -

Amortization

This term refers to the process of paying off a loan over time through scheduled payments. For B2B buyers, understanding amortization schedules can aid in financial forecasting and budgeting. -

Loan-to-Value Ratio (LTV)

LTV is a financial term that expresses the ratio of a loan to the value of an asset purchased. This metric is vital for B2B buyers when assessing the risk and feasibility of mortgage financing options offered by UWM.

By grasping these technical properties and trade terms, international B2B buyers can navigate the mortgage payment landscape more effectively, ensuring informed decision-making and strategic financial management.

Navigating Market Dynamics and Sourcing Trends in the pay united wholesale mortgage Sector

How Are Global Economic Drivers Shaping the Pay United Wholesale Mortgage Sector?

The pay united wholesale mortgage sector is currently witnessing significant shifts driven by globalization, technological advancements, and changing consumer preferences. One of the main global drivers is the increasing demand for mortgage services in emerging markets, particularly in Africa, South America, and parts of Europe. These regions are experiencing a surge in urbanization and a growing middle class, which translates into a higher demand for home financing solutions. Furthermore, international buyers are increasingly looking for streamlined, efficient mortgage services that can be accessed digitally.

Current sourcing trends reflect a movement toward automation and the integration of artificial intelligence (AI) in mortgage processing. Technologies such as blockchain are also gaining traction, offering enhanced security and transparency in transactions. For international B2B buyers, this means that partnering with a wholesale mortgage provider that embraces these technologies can lead to more efficient operations, reduced costs, and improved customer satisfaction.

Moreover, the competitive landscape is evolving, with new entrants leveraging innovative platforms to disrupt traditional mortgage processes. This creates opportunities for established players to refine their offerings and for buyers to seek out providers that can deliver tailored solutions to meet specific market needs.

What Role Does Sustainability and Ethical Sourcing Play in the Pay United Wholesale Mortgage Sector?

As global awareness of environmental issues rises, sustainability and ethical sourcing have become critical considerations in the pay united wholesale mortgage sector. The environmental impact of mortgage servicing, particularly in construction and financing, necessitates a shift towards sustainable practices. International buyers are increasingly prioritizing partnerships with firms that demonstrate a commitment to eco-friendly practices and responsible sourcing of materials.

Incorporating ‘green’ certifications and materials into mortgage offerings not only enhances brand reputation but also aligns with the values of environmentally-conscious consumers. For example, mortgages that facilitate energy-efficient home upgrades or that are associated with environmentally sustainable housing projects can appeal to a growing segment of buyers.

Additionally, ethical supply chains are essential for building trust and ensuring compliance with international regulations. Buyers are encouraged to evaluate potential partners based on their sustainability practices and ethical sourcing policies, as these factors can significantly impact long-term business viability and customer loyalty.

How Has the Pay United Wholesale Mortgage Sector Evolved Over Time?

The evolution of the pay united wholesale mortgage sector has been marked by significant technological advancements and shifts in consumer behavior. Historically, mortgage processes were heavily reliant on manual paperwork and in-person interactions, often leading to inefficiencies and delays. The introduction of digital platforms has transformed the landscape, allowing for faster processing times and enhanced customer experiences.

In recent years, the rise of online mortgage providers and fintech solutions has further accelerated this transformation. These innovations have not only streamlined operations but have also expanded access to mortgage services for international buyers. As the sector continues to evolve, staying abreast of these changes will be crucial for B2B buyers seeking to navigate the complexities of the global mortgage market effectively.

In summary, understanding market dynamics, embracing sustainability, and recognizing the historical context of the pay united wholesale mortgage sector are essential for international B2B buyers looking to optimize their sourcing strategies and partnerships.

Frequently Asked Questions (FAQs) for B2B Buyers of pay united wholesale mortgage

-

How do I solve payment processing issues with United Wholesale Mortgage?

To resolve payment processing issues with United Wholesale Mortgage (UWM), first ensure that you have accurate account information and that your payment method is valid. If an online payment fails, check for any alerts regarding server issues or maintenance on the UWM site. For persistent problems, contact UWM’s customer support at 888-464-2432 during their business hours. Document your payment attempts and communications for reference, which can help expedite resolution. -

What is the best payment method for international transactions with UWM?

For international transactions with United Wholesale Mortgage, wire transfers are often the most efficient and secure method. They allow for direct transfers between banks, minimizing delays often associated with checks or other payment forms. Ensure you confirm UWM’s specific wire transfer details and any associated fees beforehand. Additionally, consider using a currency exchange service to lock in favorable rates if your currency differs from the U.S. dollar. -

What are the minimum order quantities (MOQ) when partnering with UWM?

While United Wholesale Mortgage primarily focuses on mortgage services rather than physical products, the concept of MOQ typically applies to tangible goods. If you are engaging in a partnership involving services or digital products, discuss your specific needs directly with UWM. They can provide customized solutions based on your volume requirements or specific business goals. -

How can I verify the legitimacy of United Wholesale Mortgage as a partner?

To verify the legitimacy of United Wholesale Mortgage, consider checking their licensing and regulatory compliance through the National Mortgage Licensing System (NMLS). Additionally, review their financial stability by analyzing credit ratings and industry reviews. Engaging with current or past clients can also provide insights into their reputation and reliability in the wholesale mortgage sector. -

What customization options are available for mortgage solutions at UWM?

United Wholesale Mortgage offers various customization options tailored to meet specific client needs, such as flexible payment schedules and loan types. Businesses can work closely with UWM representatives to discuss specific requirements, including loan amounts, interest rates, and repayment terms. UWM’s technology platform also allows for personalized user experiences, enhancing the mortgage process for your clients. -

What are the typical payment terms for B2B transactions with UWM?

Payment terms for B2B transactions with United Wholesale Mortgage generally vary based on the specific agreement. It is crucial to discuss payment schedules, such as upfront payments or installment plans, during the negotiation phase. Typically, UWM may require payments to be made on a monthly basis, aligning with mortgage servicing standards. Clarifying these terms upfront can prevent misunderstandings later. -

How does UWM handle quality assurance for their mortgage services?

United Wholesale Mortgage employs a rigorous quality assurance process that includes regular audits of their loan servicing operations and customer feedback mechanisms. They strive to maintain compliance with industry regulations and standards, ensuring a high level of service quality. B2B buyers should inquire about specific QA metrics that UWM uses to ensure reliability and service excellence. -

What logistical considerations should I keep in mind when working with UWM?

When working with United Wholesale Mortgage, consider the logistics of communication and documentation. Ensure that all parties are aware of the time zone differences, especially when dealing with international partners. Utilize secure digital channels for document sharing to streamline the process. Additionally, familiarize yourself with the servicing timelines for loan processing and payment schedules to align expectations and improve efficiency.

Important Disclaimer & Terms of Use

⚠️ Important Disclaimer

The information provided in this guide, including content regarding manufacturers, technical specifications, and market analysis, is for informational and educational purposes only. It does not constitute professional procurement advice, financial advice, or legal advice.

While we have made every effort to ensure the accuracy and timeliness of the information, we are not responsible for any errors, omissions, or outdated information. Market conditions, company details, and technical standards are subject to change.

B2B buyers must conduct their own independent and thorough due diligence before making any purchasing decisions. This includes contacting suppliers directly, verifying certifications, requesting samples, and seeking professional consultation. The risk of relying on any information in this guide is borne solely by the reader.

Strategic Sourcing Conclusion and Outlook for pay united wholesale mortgage

In conclusion, strategic sourcing within the context of United Wholesale Mortgage (UWM) offers significant advantages for international B2B buyers. By leveraging UWM’s streamlined payment processes, such as the Automatic Payment (ACH) program, businesses can enhance their cash flow management and reduce the administrative burden associated with traditional payment methods. Additionally, the flexibility of payment options, including online payments and biweekly auto payments, caters to diverse operational needs across various markets.

The value of strategic sourcing extends beyond immediate financial benefits; it fosters long-term partnerships that can lead to improved service delivery and competitive advantages. For B2B buyers from regions such as Africa, South America, the Middle East, and Europe, engaging with UWM can unlock new opportunities for growth and efficiency in mortgage financing.

As we look ahead, it is essential for international buyers to explore these strategic sourcing options with UWM actively. By doing so, they can not only optimize their payment processes but also position themselves for future success in an increasingly interconnected global marketplace. Embrace the potential of UWM’s offerings and take the next step towards elevating your business operations.