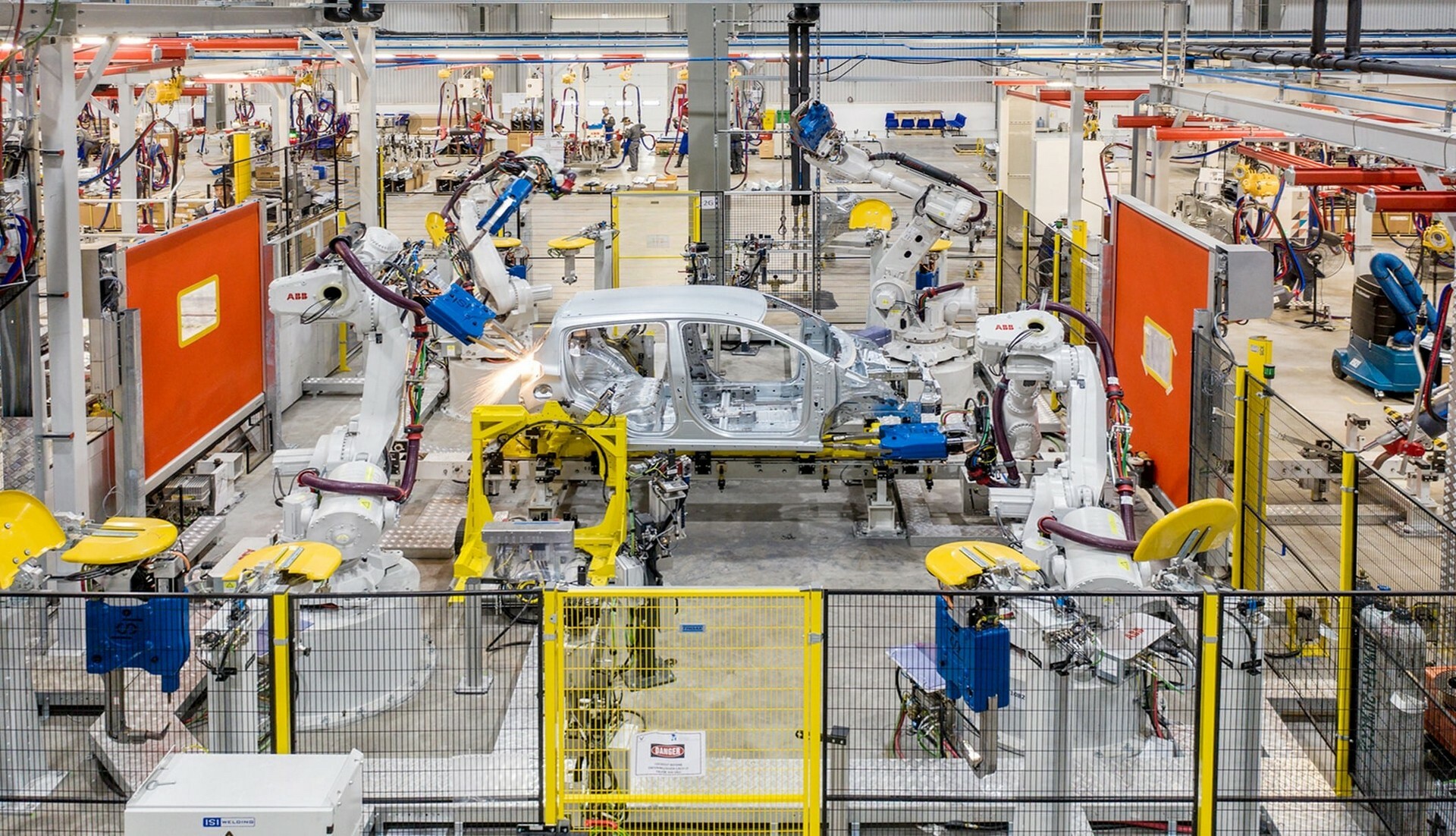

The Indian automotive manufacturing sector has emerged as a global powerhouse, driven by robust domestic demand, government initiatives like ‘Make in India’, and increasing export volumes. According to Mordor Intelligence, the Indian automotive market was valued at USD 115.67 billion in 2023 and is projected to reach USD 181.9 billion by 2029, growing at a CAGR of 7.82% during the forecast period. This expansion is fueled by rising vehicle penetration, rapid urbanization, and a shift toward electric mobility supported by policy incentives. As India solidifies its position as the third-largest automotive market globally—after China and the USA—the industry continues to see significant investments in manufacturing capabilities, R&D, and sustainable technologies. In this dynamic landscape, a select group of homegrown manufacturers are leading the charge, shaping both domestic consumption and international supply chains. The following are the top 10 Indian automotive manufacturers, ranked based on production volume, revenue, market share, and strategic influence in the evolving automotive ecosystem.

Top 10 Indian Automotive Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Indian Automotive

H2: Analysis of Indian Automotive Market Trends for 2026

The Indian automotive market is poised for transformative growth and structural shifts by 2026, driven by government policies, technological advancements, evolving consumer preferences, and a strong push toward sustainability. The H2 (second half) outlook for 2026 reflects a maturing industry embracing electrification, digitalization, and localized manufacturing, with increasing competitiveness and innovation shaping the sector.

1. Accelerated Shift Toward Electrification

By H2 2026, electric vehicles (EVs) are expected to account for a significant share of new vehicle sales, especially in the two-wheeler and passenger car segments. The government’s continued support through the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme, combined with state-level incentives, has catalyzed EV adoption.

- EV Penetration: Two-wheelers are leading the EV transition, with penetration expected to exceed 25% in new sales by H2 2026. For passenger vehicles, EV market share is projected to reach 15–20%.

- Battery Ecosystem Growth: India is witnessing rapid development in lithium-ion cell manufacturing, with gigafactories coming online in Gujarat, Tamil Nadu, and Karnataka. Localization of battery packs and components is improving cost competitiveness.

- Charging Infrastructure Expansion: Public and private investments in charging networks—especially in Tier-1 and Tier-2 cities—are expected to alleviate range anxiety and support long-term adoption.

2. Growth in Premium and SUV Segments

Consumer preferences continue to shift toward premium and utility-focused vehicles. SUVs are projected to dominate over 50% of the passenger vehicle market by H2 2026.

- Domestic Production Surge: Automakers are expanding SUV production capacity domestically to meet rising demand and take advantage of Production Linked Incentive (PLI) schemes.

- Hybrid Models Gaining Traction: Before full electrification, mild-hybrid and strong-hybrid SUVs are serving as transitional products, especially in price-sensitive markets.

3. Strengthening of Domestic Manufacturing and Exports

India is increasingly positioning itself as a global automotive export hub, with H2 2026 likely to see record export volumes.

- “China+1” Strategy: Global OEMs are leveraging India’s skilled workforce, competitive costs, and trade agreements to diversify supply chains, boosting exports of compact cars and commercial vehicles.

- PLI Scheme Impact: The PLI scheme for automotive manufacturing is driving investments in advanced technologies and high-efficiency vehicles, increasing the export potential of made-in-India vehicles to Europe, Latin America, and ASEAN countries.

- Commercial Vehicle Recovery: With infrastructure projects gaining momentum under the National Infrastructure Pipeline, demand for medium and heavy commercial vehicles (MHCVs) is expected to grow steadily in H2 2026.

4. Digitalization and Connected Mobility

By H2 2026, nearly all new vehicles sold in India will feature some level of connectivity and advanced driver assistance systems (ADAS), especially in the mid-to-high-end segments.

- Smart Infotainment and OTA Updates: Consumers are demanding seamless smartphone integration, real-time navigation, and over-the-air (OTA) software updates.

- Telematics and Fleet Management: Adoption in commercial fleets is rising, driven by logistics optimization and regulatory compliance (e.g., FASTag, emission norms).

5. Sustainability and Regulatory Pressures

Stricter emission norms (BS-VI Phase 2 fully enforced by 2023) continue to influence design and technology choices.

- Carbon Neutrality Goals: Automakers are investing in green manufacturing, renewable energy integration, and carbon offset programs to align with India’s 2070 net-zero target.

- Circular Economy Initiatives: Emphasis on EV battery recycling, remanufacturing, and end-of-life vehicle management is growing, supported by upcoming regulatory frameworks.

6. Challenges and Risks

Despite positive momentum, the sector faces headwinds:

- Raw Material Volatility: Lithium, cobalt, and nickel prices remain a concern for EV cost stability.

- Infrastructure Gaps: Uneven charging infrastructure across rural and semi-urban areas could limit mass EV adoption.

- Financing Constraints: High upfront costs of EVs and limited access to affordable financing remain barriers for mass-market consumers.

Conclusion

The H2 2026 outlook for the Indian automotive market is one of dynamic evolution, characterized by robust growth in electrification, increased export competitiveness, and technological innovation. While challenges remain, supportive government policies, growing consumer awareness, and a flourishing startup ecosystem in mobility tech position India as a key player in the global automotive landscape. Automakers that prioritize localization, sustainability, and digital customer engagement will be best positioned to lead in this new era.

Common Pitfalls Sourcing Indian Automotive Components (Quality, IP)

Sourcing automotive components from India offers significant cost advantages and access to a growing manufacturing base. However, international buyers often encounter challenges related to quality consistency and intellectual property (IP) protection. Understanding these pitfalls is crucial for successful and sustainable partnerships.

Quality Inconsistencies and Process Gaps

One of the most persistent challenges is maintaining consistent product quality across batches. While many Indian suppliers are certified to international standards like IATF 16949, implementation can vary significantly. Buyers may face deviations in material specifications, dimensional tolerances, or surface finishes due to inadequate process controls, insufficient training, or lapses in calibration of testing equipment. Additionally, supply chain fragmentation—where Tier 2 and Tier 3 suppliers lack robust quality systems—can introduce hidden risks. Without proactive quality audits and real-time monitoring, defects may go undetected until late stages, leading to production delays or field failures.

Inadequate Intellectual Property Protection

Protecting intellectual property remains a critical concern. India’s IP laws, while aligned with international treaties like TRIPS, face challenges in enforcement, especially at the state and local levels. Suppliers may unintentionally or deliberately replicate designs, share proprietary technical data with third parties, or produce “gray market” parts using bought-in tooling. Lack of clear contractual clauses defining IP ownership, usage rights, and confidentiality can exacerbate risks. Furthermore, reverse engineering by local competitors after sample evaluation is a known issue, particularly when non-disclosure agreements (NDAs) are weak or unsigned.

Cultural and Communication Misalignments

Differences in business culture and communication styles can amplify quality and IP issues. Indirect communication may lead to delayed escalation of production problems, resulting in missed milestones. Hierarchical decision-making in some organizations slows response times during critical quality interventions. Misunderstandings about specifications or acceptance criteria—especially when documentation is not meticulously maintained—can lead to non-conforming deliveries. Building trust through frequent site visits, clear technical documentation, and culturally sensitive management is essential but often underestimated.

Supplier Capability Overestimation

Buyers sometimes overestimate a supplier’s production capacity, technical expertise, or scalability based on initial presentations or certifications. This can lead to over-reliance on a single source without thorough due diligence. Pilot runs may succeed under close supervision, but volume production reveals weaknesses in workforce management, supply chain resilience, or process stability. Failure to conduct rigorous technical audits, including process capability (Cp/Cpk) studies and gauge repeatability and reproducibility (GR&R) analysis, increases the risk of long-term performance gaps.

Mitigation Requires Proactive Engagement

Avoiding these pitfalls demands more than transactional sourcing. Buyers must conduct thorough due diligence, implement strong IP clauses in contracts, perform regular on-site quality audits, and invest in supplier development programs. Establishing joint quality improvement teams and clear escalation paths can bridge operational and cultural gaps, ensuring both quality and IP integrity throughout the sourcing lifecycle.

Logistics & Compliance Guide for Indian Automotive Industry

The Indian automotive sector is a dynamic and highly regulated industry, encompassing vehicle manufacturing, component supply, distribution, and after-sales services. Managing logistics efficiently while ensuring compliance with diverse regulations is critical for operational success, cost optimization, and legal adherence. This guide outlines key logistics and compliance considerations for stakeholders in the Indian automotive ecosystem.

Supply Chain Structure and Logistics Framework

The Indian automotive supply chain typically involves a network of original equipment manufacturers (OEMs), tier-1 to tier-3 suppliers, third-party logistics (3PL) providers, and distributors. Logistics operations include inbound (raw materials and components), outbound (finished vehicles and spare parts), and reverse logistics.

- Inbound Logistics: Focuses on timely delivery of components from suppliers to assembly plants. Just-in-Time (JIT) and Just-in-Sequence (JIS) models are widely adopted, requiring high precision in scheduling and coordination.

- Outbound Logistics: Involves the movement of finished vehicles via rail, road, or roll-on/roll-off (Ro-Ro) vessels to dealerships and customers. Vehicle carriers and Rail-Head Terminals (RHTs) play key roles.

- Warehousing: Strategic placement of central, regional, and local warehouses ensures optimal inventory turnover and supports after-sales parts distribution.

Regulatory Compliance Landscape

Compliance is multi-layered, involving central and state-level regulations across safety, environment, tax, and transport domains.

Automotive Safety and Quality Standards

- Bharat New Car Assessment Program (BNCAP): Mandates crashworthiness and safety features for passenger vehicles. OEMs must ensure design and manufacturing compliance.

- Automotive Industry Standard (AIS): Issued by the Ministry of Road Transport and Highways (MoRTH), AIS covers safety, emissions, and performance (e.g., AIS-145 for electronic stability control).

- Type Approval: All vehicles must undergo type approval under the Central Motor Vehicles Rules (CMVR), 1989, administered by testing agencies like ARAI, ICAT, or VRDE.

Emission and Environmental Regulations

- Bharat Stage (BS) VI Norms: Enforced since April 2020, these are equivalent to Euro VI standards. All vehicles must meet BS-VI emission levels. Non-compliant models cannot be sold or registered.

- Extended Producer Responsibility (EPR): Under the Plastic Waste Management Rules and e-waste regulations, OEMs and importers must manage end-of-life vehicles (ELVs) and recyclable components.

- Energy Efficiency: Compliance with Bureau of Energy Efficiency (BEE) norms may apply to auxiliary systems and electric vehicles (EVs).

Tax and Fiscal Compliance

- Goods and Services Tax (GST): Automotive products are taxed under different GST slabs:

- Passenger vehicles: 28% + GST Compensation Cess (up to 21% depending on engine size and length).

- Commercial vehicles: 28% (no cess).

- Spare parts and tyres: 18% or 28%, depending on category.

- Input Tax Credit (ITC): Must be carefully tracked and claimed, especially in multi-state logistics operations.

- Deferred Payment Schemes: States may offer tax incentives for manufacturing units; compliance with conditions is mandatory.

Transport and Road Regulations

- Permits and Registrations: Vehicles used for commercial transport (e.g., carrier trucks) require national and state permits under the Motor Vehicles Act, 1988.

- Over-dimensional Cargo (ODC) Rules: Movement of large vehicle carriers or industrial equipment requires prior approval from state transport authorities.

- FASTag and Toll Compliance: Mandatory electronic toll collection via FASTag for all commercial vehicles under NHAI regulations.

Customs and Import/Export Compliance

For automotive components and vehicles involved in international trade:

- Import Regulations:

- Components and Complete Built Units (CBUs) are subject to customs duty, IGST, and cess.

- Compliance with Foreign Trade Policy (FTP), including filing of Bill of Entry and obtaining necessary licenses (e.g., for dual-use items).

-

Rules of Origin under FTAs (e.g., India-Japan CEPA) must be met to claim duty benefits.

-

Export Regulations:

- Eligibility for duty drawbacks and export incentives under the Remission of Duties and Taxes on Exported Products (RoDTEP) scheme.

- Adherence to destination country standards (e.g., EU, ASEAN) for homologation.

Labour and Industrial Safety Compliance

- Factories Act, 1948: Applies to manufacturing units with 10+ workers using power, or 20+ without. Mandates safety audits, welfare facilities, and working hour regulations.

- Contract Labour (Regulation and Abolition) Act, 1970: Governs use of contract workers in logistics and manufacturing.

- Occupational Health and Safety: Compliance with standards under the Building and Other Construction Workers Act and state-specific rules.

Data and Digital Compliance

- Vehicle Tracking: GPS tracking is mandatory for all transport vehicles under MoRTH notification (for safety and anti-theft).

- Digital Documentation: E-way bills are required for intra- and inter-state movement of goods valued over ₹50,000. Failure to generate incurs penalties.

- Data Localization: Under IT Act and proposed Digital Personal Data Protection Act, 2023, personal data collected via connected vehicles must be handled per privacy guidelines.

Sustainability and Emerging Trends

- Electric Vehicles (EVs): Subject to FAME-II subsidies (now extended), OEMs must comply with battery safety standards (AIS-048) and secure approval for charging infrastructure.

- Green Logistics: Encouragement of CNG/electric cargo vehicles, solar-powered warehouses, and carbon footprint reporting under initiatives like Science-Based Targets initiative (SBTi).

- Circular Economy: Adoption of remanufacturing and recycling practices compliant with ELV Framework (draft rules under MoRTH).

Best Practices for Compliance and Logistics Efficiency

- Integrated Compliance Management System (ICMS): Use digital platforms to track regulatory changes, deadlines, and submissions.

- Vendor Compliance Audits: Ensure suppliers and logistics partners adhere to quality and safety norms.

- Real-Time Visibility Tools: Implement IoT and GPS tracking for fleet and inventory monitoring.

- Regular Training: Conduct compliance workshops for staff on GST, CMVR, and safety standards.

- Engage with Industry Bodies: Participate in SIAM (Society of Indian Automobile Manufacturers) for policy advocacy and updates.

Conclusion

Navigating logistics and compliance in the Indian automotive sector demands a proactive, integrated approach. With rapid regulatory evolution—especially in electrification, emissions, and digitalization—stakeholders must adopt agile systems to maintain competitiveness and legal integrity. Staying informed, investing in digital tools, and fostering collaboration across the supply chain are essential for long-term success.

Conclusion: Sourcing from Indian Automotive Manufacturers

Sourcing from Indian automotive manufacturers presents a compelling opportunity for global businesses seeking cost-effective, high-quality components and vehicles. India’s robust automotive ecosystem, supported by a skilled workforce, advanced manufacturing capabilities, and a strong supplier base, positions it as a key player in the global automotive supply chain. Favorable government policies, continuous investment in technology, and a growing focus on electric and sustainable mobility further enhance its competitiveness.

Additionally, Indian manufacturers have demonstrated resilience and adaptability, meeting international quality standards and complying with global regulatory requirements. Partnerships with leading global OEMs and Tier-1 suppliers underscore India’s reliability as a manufacturing hub.

However, success in sourcing from India requires due diligence in supplier selection, clear understanding of logistics and lead times, and attention to quality control processes. With strategic planning and strong collaboration, sourcing from Indian automotive manufacturers can offer significant advantages in terms of scalability, innovation, and cost efficiency—making India a vital destination for the future of automotive procurement.