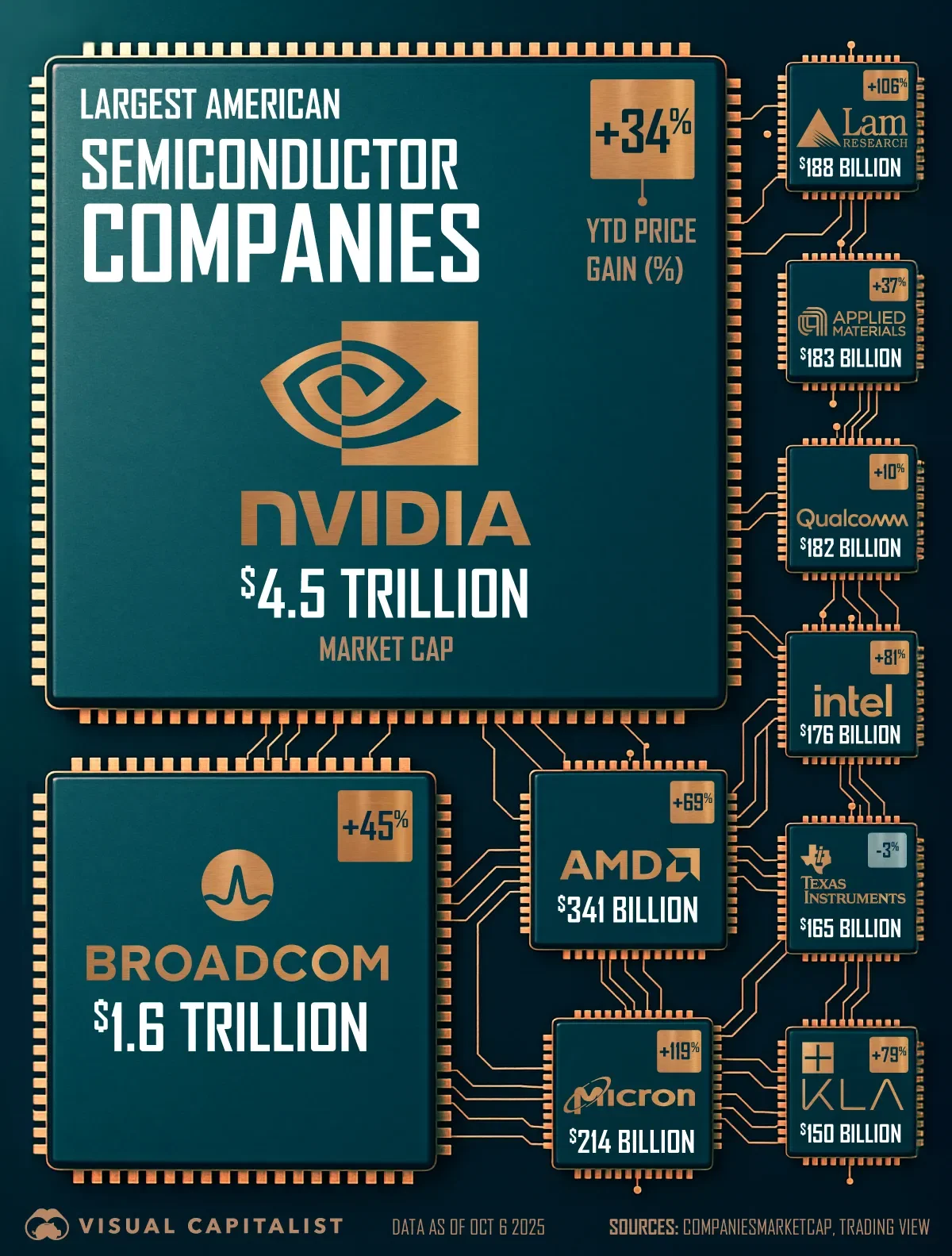

The global semiconductor industry has experienced robust expansion driven by increasing demand across consumer electronics, automotive, industrial automation, and data centers. According to a 2023 report by Mordor Intelligence, the semiconductor market was valued at approximately USD 574 billion in 2022 and is projected to grow at a compound annual growth rate (CAGR) of 8.2% from 2023 to 2028, reaching an estimated USD 928 billion by the end of the forecast period. This growth is fueled by technological advancements, rising adoption of IoT devices, and government initiatives supporting domestic chip production. As demand outpaces supply in key regions, the competitive landscape has become increasingly concentrated among a handful of dominant players. The top eight chip manufacturers now account for over 75% of global semiconductor revenue, leveraging massive investments in R&D, process node innovation, and manufacturing scale to maintain their leadership. These companies not only drive the pace of innovation but also shape the resiliency and direction of global supply chains in an era defined by digital transformation.

Top 8 Largest Chip Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Largest Chip

H2: 2026 Market Trends for the Largest Chipmakers

As we approach 2026, the semiconductor industry—particularly among the largest chipmakers—is undergoing transformative shifts driven by technological innovation, geopolitical dynamics, and surging demand across multiple sectors. The leading players, including TSMC, NVIDIA, Intel, Samsung, and AMD, are redefining their strategies to maintain dominance in this high-stakes environment. Below are the key market trends shaping the landscape for the largest chip companies in 2026.

1. AI and HPC Driving Unprecedented Demand

Artificial Intelligence (AI) and High-Performance Computing (HPC) continue to be the primary growth engines for the largest chipmakers. In 2026, AI-specific chips—especially GPUs and custom accelerators—account for a significant share of revenue among leaders like NVIDIA and AMD. Demand for data center GPUs is soaring as enterprises and cloud providers scale up generative AI models, requiring advanced chips built on cutting-edge nodes (e.g., 3nm and 2nm). TSMC remains the critical foundry partner, with record capacity utilization for AI-related wafer production.

2. Geopolitical Fragmentation and Regionalization of Supply Chains

The U.S.-China tech rivalry intensifies in 2026, accelerating supply chain diversification. The CHIPS and Science Act in the U.S. and similar initiatives in Europe and India drive significant investments in domestic semiconductor manufacturing. Intel and TSMC expand their U.S. fabs (e.g., Intel’s Ohio campus, TSMC’s Arizona facilities), reducing reliance on East Asian production. Meanwhile, China advances its domestic capabilities through SMIC and other state-backed efforts, though still lagging in sub-5nm process technology due to export controls.

3. Advancement in Process Technology and 2nm Proliferation

2026 marks the commercial ramp-up of 2nm-class process nodes. TSMC and Samsung begin volume production using next-generation gate-all-around (GAA) transistor architectures (e.g., TSMC’s N2, Samsung’s SF2), offering improved power efficiency and performance. Apple, NVIDIA, and Qualcomm are early adopters, integrating 2nm chips into next-gen smartphones, data center accelerators, and AI edge devices. This node transition reinforces TSMC’s leadership in advanced foundry services.

4. Growth in Edge AI and Automotive Chips

Beyond data centers, the largest chipmakers are expanding into edge AI and automotive applications. In 2026, demand for AI-powered chips in autonomous driving, robotics, and IoT devices grows rapidly. NVIDIA’s DRIVE platform and Intel’s Mobileye see increased adoption, while Qualcomm strengthens its position in automotive SoCs. These segments provide diversified revenue streams and reduce dependence on consumer PC and smartphone markets.

5. Consolidation and Strategic Partnerships

To manage rising R&D and fabrication costs, major players engage in strategic alliances and selective M&A. Intel expands its foundry services (IFS) partnerships with cloud providers and fabless firms, while AMD explores deeper integration with Xilinx in adaptive computing. Foundry access becomes a strategic asset, with U.S. and European governments facilitating collaborations to bolster domestic capacity.

6. Sustainability and Energy Efficiency as Competitive Factors

With growing scrutiny on data center power consumption, chipmakers prioritize energy-efficient designs. In 2026, ESG (Environmental, Social, and Governance) metrics influence customer procurement decisions. TSMC and Intel invest in green fabs powered by renewable energy, while NVIDIA emphasizes performance-per-watt in its AI chips, becoming a key selling point for hyperscalers.

7. Rise of Chiplet Architectures and Advanced Packaging

Heterogeneous integration and chiplet-based designs become mainstream in 2026. Leading firms leverage advanced packaging technologies like CoWoS (TSMC), Foveros (Intel), and X-Cube (Samsung) to combine specialized dies (CPU, GPU, memory) into single systems. This modular approach improves yield, reduces costs, and enables faster time-to-market—especially critical for AI and high-end networking chips.

Conclusion

By 2026, the largest chipmakers are navigating a complex but opportunity-rich environment. Success hinges on leadership in AI, mastery of advanced nodes, geopolitical agility, and innovation in packaging and power efficiency. TSMC and NVIDIA maintain strong momentum, while Intel and Samsung strive to close gaps. As chips become foundational to global technological sovereignty, the industry’s trajectory reflects broader economic and strategic realignments.

Common Pitfalls Sourcing the Largest Chip (Quality, IP)

Sourcing the largest semiconductor chips—such as advanced AI accelerators, high-performance computing (HPC) SoCs, or cutting-edge GPUs—introduces unique challenges, particularly concerning quality assurance and intellectual property (IP) protection. Missteps in these areas can lead to significant financial, legal, and operational risks. Below are the most common pitfalls to avoid.

Quality-Related Pitfalls

1. Yield and Defect Density Challenges

Larger die sizes inherently reduce manufacturing yield due to increased exposure to process variations and particulate defects. A single defect across a large silicon area can render the entire chip unusable. Relying on suppliers without proven high-yield production capabilities for large dies can result in inconsistent supply and high failure rates in end products.

2. Thermal and Mechanical Stress Issues

Large chips generate more heat and are more susceptible to thermal expansion. Inadequate attention to thermal management in packaging or insufficient stress testing during qualification can lead to early field failures, delamination, or solder joint fatigue—especially under sustained workloads.

3. Inadequate Supply Chain Transparency

Without full visibility into the foundry, assembly, and test chain, it’s difficult to assess quality control rigor. Sourcing through intermediaries or unverified subcontractors increases the risk of counterfeit parts, substandard packaging, or bypassed testing protocols.

4. Insufficient Burn-In and Longevity Testing

Largest chips are often used in mission-critical systems (e.g., data centers, autonomous systems). Skipping or shortening reliability testing—such as extended burn-in, HTOL (High-Temperature Operating Life), or electromigration testing—can result in premature failures and reputational damage.

IP-Related Pitfalls

1. Unsecured or Poorly Defined IP Ownership

When sourcing custom or semi-custom large chips, ambiguous IP agreements can lead to disputes over ownership of design elements, firmware, or process optimizations. Ensure contracts explicitly state which party owns the foundational IP, derivative works, and any enhancements made during development.

2. Risk of IP Leakage During Manufacturing

Large, complex designs contain valuable trade secrets. Using foundries or OSATs (Outsourced Semiconductor Assembly and Test) in regions with weaker IP enforcement raises the risk of design theft or reverse engineering. Lack of secure data transfer protocols and insufficient NDAs compound this risk.

3. Third-Party IP Integration Without Proper Licensing

Large chips often integrate third-party IP blocks (e.g., SerDes, PCIe controllers, AI accelerators). Failing to verify that the supplier has valid, transferable licenses for all embedded IP can expose the buyer to infringement claims—even if unintentional.

4. Inadequate Protection in Multi-Source or Second-Sourcing Arrangements

Planning for supply continuity by qualifying second sources can inadvertently expose sensitive designs. Without strict controls and legal safeguards, sharing GDSII files or test vectors increases the likelihood of IP misuse or competitive exposure.

Mitigation Strategies

- Partner with foundries and OSATs that have a proven track record in large-die production and offer robust IP protection frameworks (e.g., TSMC, Samsung with secure design shuttles).

- Conduct rigorous on-site audits of manufacturing and testing facilities.

- Implement legal agreements that clearly define IP ownership, usage rights, and confidentiality obligations.

- Use hardware security modules (HSMs) and encrypted design flows during tape-out and fabrication.

- Require detailed quality reports, including wafer maps, binning data, and reliability test results.

By proactively addressing these quality and IP pitfalls, organizations can reduce risk and ensure the successful integration of the largest and most advanced semiconductor chips into their products.

Logistics & Compliance Guide for Largest Chip

Overview

This guide outlines the logistics processes and compliance requirements for managing the operations of Largest Chip, a leading semiconductor manufacturer. It ensures efficient movement of materials, adherence to international trade regulations, and alignment with industry standards.

Supply Chain Structure

Largest Chip maintains a global supply chain network involving raw material sourcing, wafer fabrication, assembly, testing, and final product distribution. Key components include:

– Suppliers: Verified vendors of silicon wafers, chemicals, and equipment

– Manufacturing Hubs: Primary facilities in the U.S., Taiwan, and Germany

– Distribution Centers: Strategically located in North America, Europe, and Asia

Transportation & Warehousing

All shipments are coordinated through an integrated logistics management system. Requirements include:

– Use of temperature-controlled and ESD-safe packaging for sensitive components

– Real-time GPS tracking for high-value shipments

– Partnering with certified logistics providers compliant with ISO 28000 (Security Management)

– Warehouse operations follow 5S methodology and OSHA safety standards

Import & Export Compliance

Largest Chip complies with all international trade laws, including:

– EAR (Export Administration Regulations): Classification of chips under ECCN 3A001.b.1

– ITAR (International Traffic in Arms Regulations): Exemption verification for non-defense-related products

– Customs-Trade Partnership Against Terrorism (C-TPAT): Certified member for U.S. imports

– RoHS and REACH: Compliance with EU environmental directives for hazardous substances

Sanctions & Restricted Party Screening

All transactions undergo automated screening against global denied party lists, including:

– OFAC (U.S. Treasury)

– BIS Entity List

– EU Consolidated List

– UN Sanctions List

Screening is conducted at order entry, shipment, and vendor onboarding stages.

Documentation Requirements

Required documentation for every shipment includes:

– Commercial invoice with HS codes and value declaration

– Packing list with itemized contents

– Certificate of Origin

– Export Control Classification Number (ECCN) statement

– Dangerous Goods Declaration (if applicable)

Cybersecurity & Data Protection

Logistics data systems adhere to:

– NIST Cybersecurity Framework

– GDPR for EU customer data

– CCPA for California-based transactions

– Regular third-party audits and penetration testing

Sustainability & ESG Compliance

Largest Chip is committed to sustainable logistics through:

– Carbon footprint tracking via SmartWay program

– Use of recyclable and minimal packaging materials

– Preference for sea freight over air freight when feasible

– Annual public ESG reporting aligned with GRI Standards

Incident Response & Audits

- All logistics disruptions are reported within 2 hours to the Global Operations Center

- Internal compliance audits conducted quarterly

- External audits by third-party firms annually

- Non-conformance reports (NCRs) resolved within 30 days

Training & Accountability

All logistics and procurement staff must complete:

– Annual export compliance training (led by Legal & Compliance)

– IATA Dangerous Goods Regulations (if handling hazardous materials)

– Cybersecurity awareness certification

Managers are held accountable through KPIs tied to compliance and on-time delivery.

Contact Information

For logistics inquiries: [email protected]

For compliance questions: [email protected]

24/7 Operations Support Hotline: +1-800-555-CHIP (2447)

In conclusion, sourcing from the world’s largest semiconductor manufacturer offers significant advantages in terms of production scale, technological innovation, supply chain reliability, and global support. Partnering with a leading chipmaker ensures access to cutting-edge fabrication processes, high-quality components, and greater capacity to meet large-volume demands—critical factors in today’s competitive and rapidly evolving electronics market. However, careful due diligence is essential to address potential challenges such as geopolitical risks, long lead times, and supply prioritization during high-demand periods. A strategic sourcing partnership should therefore balance the benefits of scale and technology with risk mitigation, diversification, and long-term supply agreements to ensure resilience and continuity in the supply chain.