The global electric vehicle (EV) market is undergoing rapid transformation, fueled by increasing environmental awareness, government incentives, and advancements in battery technology. According to a report by Mordor Intelligence, the electric vehicle market was valued at USD 481.38 billion in 2023 and is projected to reach USD 1.19 trillion by 2029, growing at a compound annual growth rate (CAGR) of 16.3% during the forecast period. This surge in demand has catalyzed intense competition among manufacturers, leading to significant expansions in production capacity, R&D investment, and global market presence. As the industry scales, a select group of automakers have emerged as dominant players, accounting for the majority of EV sales worldwide. Based on production volume, market share, and technological innovation, the following are the top 10 largest electric vehicle manufacturers shaping the future of sustainable mobility.

Top 10 Largest Electric Vehicle Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

![Global Top 20 Electric Car Companies [2025]](https://www.sourcifychina.com/wp-content/uploads/2025/12/global-top-20-electric-car-companies-2025-515.png)

Expert Sourcing Insights for Largest Electric Vehicle

H2: 2026 Market Trends for the Largest Electric Vehicle Manufacturers

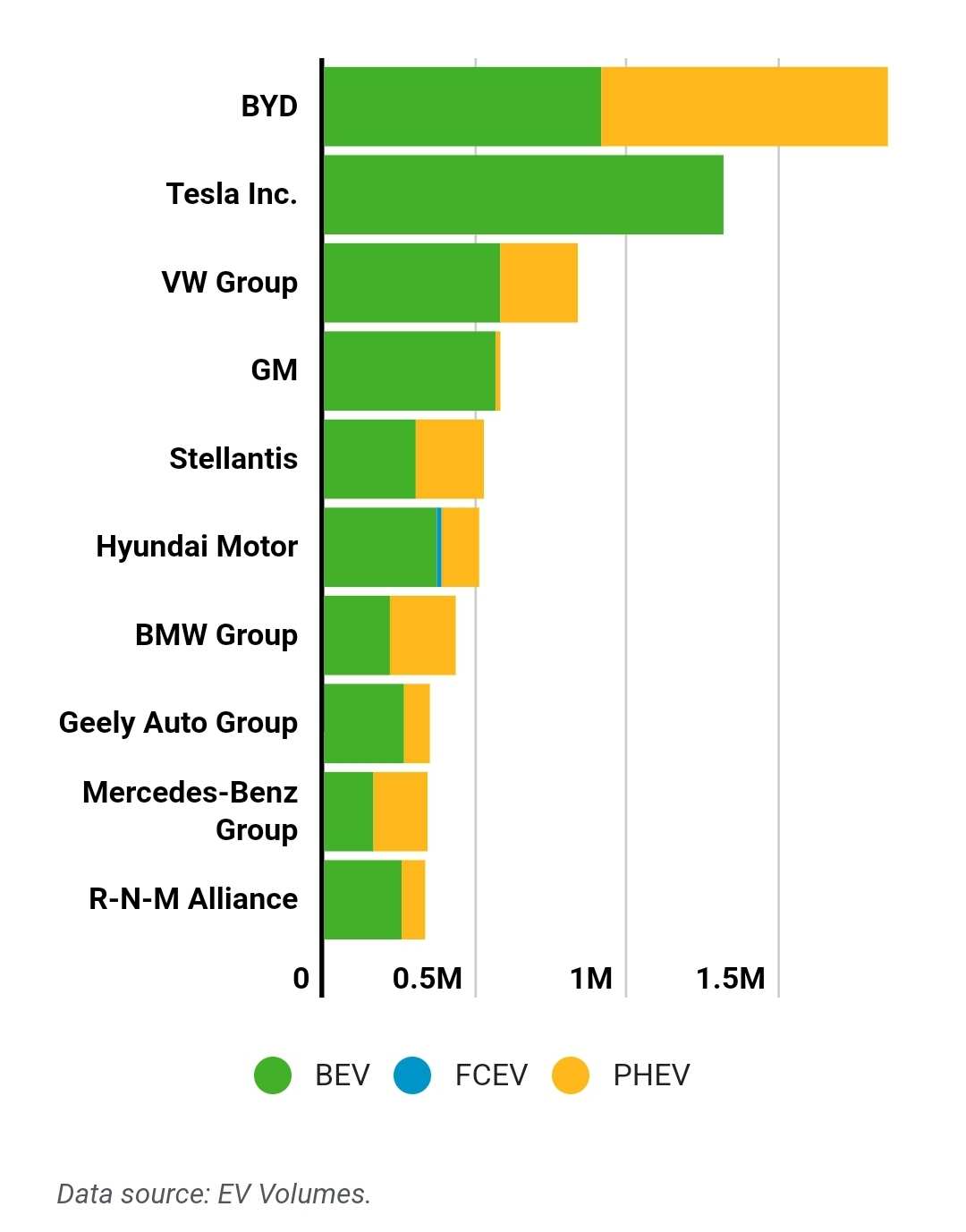

By 2026, the global electric vehicle (EV) market will be dominated by a few key players, with significant shifts driven by technological advancements, policy landscapes, and evolving consumer demands. The largest EV manufacturers – including Tesla, BYD, Volkswagen Group, Hyundai-Kia, and emerging Chinese giants like NIO and Xpeng – will navigate a complex environment characterized by intense competition, supply chain maturation, and the critical push for affordability and range.

1. Intensifying Competition & Market Consolidation:

* Chinese Dominance: BYD is projected to solidify its position as the world’s largest EV producer by volume by 2026, leveraging vertical integration (batteries, semiconductors), a vast domestic market, and aggressive global expansion (especially in Europe and Southeast Asia). Other Chinese OEMs (NIO, Xpeng, Li Auto) will increasingly target premium segments globally.

* Tesla’s Scale & Innovation Focus: Tesla will remain a volume leader and technology benchmark, but its growth rate may moderate compared to earlier years. Its focus will shift towards scaling next-generation platforms (potentially the $25k model), enhancing Full Self-Driving (FSD) capabilities (though Level 4 autonomy remains unlikely by 2026), and expanding its energy storage business.

* Legacy Automaker Push: Volkswagen Group, Hyundai-Kia, and Stellantis will have fully rolled out their dedicated EV platforms (MEB, E-GMP, STLA) by 2026. Success will hinge on their ability to achieve cost parity with ICE vehicles, build compelling software experiences, and establish reliable charging networks. Expect significant model proliferation from these groups.

* Consolidation: The market will likely see consolidation, particularly among smaller or less well-funded Chinese EV startups struggling with profitability and intense price competition.

2. Battery Technology & Cost: The Core Battleground:

* LFP Dominance: Lithium Iron Phosphate (LFP) batteries will become the dominant chemistry for standard-range and mid-priced EVs due to lower cost, improved safety, and longer cycle life. BYD’s Blade Battery and CATL’s innovations will drive this trend. Tesla, Ford, and others will heavily utilize LFP.

* Solid-State Progress (But Not Mass Production): While solid-state batteries promise significant range and safety improvements, widespread commercialization in mass-market vehicles is unlikely by 2026. Expect limited pilot production or use in niche/high-end models by pioneers like Toyota or Nissan, but liquid lithium-ion (especially LFP and advanced NMC) will remain king.

* Cost Reduction & Local Sourcing: Intense pressure to reduce battery pack costs below $100/kWh (already achieved by leaders like BYD) will continue. This will be achieved through improved cell design, manufacturing scale, and crucially, localized supply chains to mitigate geopolitical risks and import tariffs (especially in the US and EU).

3. Charging Infrastructure & Software: The Experience Imperative:

* Ultra-Fast Charging Standardization: 800V architectures enabling 10-80% charging in under 20 minutes will become more common across premium and mainstream segments. However, true global standardization (beyond CCS/ChaoJi/NACS) remains a challenge.

* Software-Defined Vehicles (SDV): The battle will shift from pure hardware to software. Largest manufacturers will invest heavily in:

* Over-the-Air (OTA) Updates: Enabling continuous feature improvements, bug fixes, and performance enhancements.

* Digital Cockpits & AI: More intuitive, personalized user interfaces and voice assistants powered by AI.

* Subscription Services: Monetization through features like advanced driver assistance, enhanced navigation, or entertainment (facing potential consumer pushback).

* Integrated Ecosystems: Success will depend on creating seamless ecosystems encompassing the vehicle, charging (own networks like Tesla Supercharger, Electrify America, or partnerships), energy (home charging/solar/batteries), and mobility services.

4. Affordability & Market Expansion:

* Price Pressure: Intense competition, particularly from China, will drive significant price reductions across segments. Achieving price parity with comparable ICE vehicles will be a key milestone for mass adoption in many regions by 2026.

* Focus on Small & Compact EVs: The largest manufacturers will expand their offerings in the small and compact EV segment to capture budget-conscious consumers and fleets, crucial for penetration in Europe and emerging markets.

* Emerging Markets Growth: India, Southeast Asia, Latin America, and parts of Africa will see accelerating EV adoption, driven by local manufacturing (e.g., Tata in India), favorable policies, and demand for affordable two/three-wheelers and small cars. BYD and other Chinese OEMs are well-positioned here.

5. Geopolitical & Regulatory Landscape:

* Protectionism & Localization: US (IRA) and EU (CBAM, upcoming EV battery regulations) policies will strongly incentivize local manufacturing and sourcing of batteries and critical minerals. This will accelerate investment in North American and European battery gigafactories by both domestic and foreign OEMs (e.g., BYD, CATL, LG).

* Emissions Regulations: Stricter CO2 fleet emission targets in the EU, China, and North America (e.g., California’s ZEV mandate) will continue to force rapid electrification, benefiting established large players with diverse EV portfolios.

* Supply Chain Security: Diversification of battery mineral supply chains (lithium, cobalt, nickel, graphite) away from single-source dependencies will be a major strategic focus, involving investments in mining, recycling, and alternative chemistries.

Conclusion for 2026:

By 2026, the landscape for the largest EV manufacturers will be defined by scale, cost leadership, and software sophistication. BYD and Tesla will likely lead in volume, while competition from legacy automakers and premium Chinese brands will be fierce. Battery cost reduction, primarily through LFP and localized production, will be paramount. Success will increasingly depend on mastering the complete customer experience – from affordable vehicle pricing and seamless charging to engaging, upgradable software. Geopolitical forces will shape where and how these giants manufacture and source components. While solid-state breakthroughs may be on the horizon, the 2026 market will still be built on the rapid evolution and optimization of current lithium-ion technology, intense price competition, and the race to build the most compelling and integrated EV ecosystem.

Common Pitfalls in Sourcing the Largest Electric Vehicles (Quality, IP)

Sourcing the largest electric vehicles—such as electric buses, heavy-duty trucks, mining haul trucks, or large delivery vans—presents unique challenges. Beyond standard procurement risks, companies must navigate complex issues related to quality assurance and intellectual property (IP) protection. Failing to address these properly can lead to operational disruptions, legal disputes, financial losses, and reputational damage.

Quality-Related Pitfalls

Overlooking Real-World Performance Validation

Many large EVs are marketed with impressive specifications under ideal conditions, but real-world performance in extreme climates, heavy payloads, or rugged terrains can differ drastically. Buyers often rely solely on manufacturer claims or lab test data without conducting independent field trials. This can result in underperforming vehicles, unexpected maintenance costs, and reduced uptime.

Inadequate Supply Chain Audits for Critical Components

The quality of large EVs heavily depends on key components like battery cells, motors, and power electronics—often sourced from third-party suppliers. Failing to audit these sub-tier suppliers increases the risk of counterfeit parts, inconsistent manufacturing standards, or component failures. Without traceability and quality control down the supply chain, systemic quality issues may emerge post-deployment.

Neglecting Long-Term Durability and Maintenance Support

Large EVs require long operational lifecycles (10+ years). Buyers may not assess the manufacturer’s track record in after-sales service, spare parts availability, or software updates. A lack of service infrastructure—especially in remote areas—can render fleets unusable. Additionally, battery degradation over time may not be accurately projected, affecting total cost of ownership.

Intellectual Property-Related Pitfalls

Insufficient IP Due Diligence During Procurement

When sourcing large EVs, especially from emerging or regional manufacturers, buyers may not verify whether the vehicle design, software, or core technologies infringe on existing patents. This exposes the buyer to third-party IP litigation, even if they were unaware of the infringement. Proper vetting of IP ownership and freedom-to-operate (FTO) opinions is essential but often overlooked.

Ambiguous Ownership of Customized Solutions

In cases where vehicles are customized for specific operational needs (e.g., unique body designs, fleet management integrations), the ownership of resulting IP is frequently not clearly defined in contracts. Vendors may retain rights to modifications, limiting the buyer’s ability to modify, scale, or transfer the technology in the future.

Vulnerability to Trade Secret Leakage

During technical evaluations, site visits, or co-development phases, buyers may disclose sensitive operational data or proprietary requirements. Without robust non-disclosure agreements (NDAs) and data security protocols, this information could be misused or shared with competitors, especially when working with suppliers in jurisdictions with weak IP enforcement.

Reliance on Proprietary Software Without Licensing Clarity

Large EVs increasingly depend on embedded software for battery management, diagnostics, and telematics. Buyers may assume full access and control, only to discover restrictive licensing terms that limit data access, prohibit third-party repairs, or require ongoing fees. This can create vendor lock-in and hinder long-term fleet flexibility.

Conclusion

Sourcing the largest electric vehicles demands rigorous attention to both quality and intellectual property risks. Proactive due diligence, clear contractual terms, independent validation, and ongoing supplier oversight are critical to avoiding costly pitfalls. Organizations should involve technical experts, legal counsel, and supply chain auditors early in the procurement process to ensure sustainable, compliant, and high-performing EV deployments.

Logistics & Compliance Guide for the Largest Electric Vehicle

Overview of the Largest Electric Vehicle Logistics Chain

Transporting and managing the logistics of the largest electric vehicles (EVs), such as electric buses, heavy-duty trucks, or specialized mining haul trucks, requires meticulous planning and adherence to global and regional compliance standards. This guide outlines key considerations for handling the movement, storage, and regulatory compliance associated with large-scale electric vehicles throughout their lifecycle—from manufacturing to deployment and end-of-life management.

Transportation and Handling

Specialized Transport Requirements

Due to their size, weight, and sensitive components (especially high-voltage battery systems), the largest EVs often require specialized transport solutions. Standard flatbed trailers may not suffice; lowboy trailers, modular extendable platforms, or multi-axle heavy haulers are typically needed. Securement must follow Department of Transportation (DOT) or equivalent international standards to prevent shifting during transit.

Route Planning and Permits

Routes must be carefully evaluated for bridge weight limits, overhead clearance, turning radius, and road conditions. Oversize/overweight permits are often required and vary by jurisdiction. Advance coordination with local authorities ensures smooth passage and avoids costly delays.

Battery Safety During Transit

Lithium-ion batteries are classified as hazardous materials under international transport regulations (e.g., IMDG for sea, ADR for road in Europe, 49 CFR in the U.S.). EVs with installed batteries may require:

– UN38.3 testing certification for battery systems

– Proper labeling and documentation

– Fire suppression systems on transport vehicles

– Avoidance of extreme temperatures during transit

Regulatory Compliance

International and National Standards

Compliance with EV-specific regulations is essential across regions:

– United States: DOT, NHTSA, and EPA standards; adherence to FMVSS (Federal Motor Vehicle Safety Standards)

– European Union: UNECE Regulations (e.g., R100 for EV safety), CE marking, and type-approval under EU Framework Regulation (EU) 2018/858

– China: CCC certification and GB standards for EV safety and battery performance

– Global: ISO 6469 (electric vehicle safety), IEC 62114 (EV components)

Electromagnetic Compatibility (EMC) and Cybersecurity

Large EVs must comply with EMC standards to avoid interference with other electronic systems. Additionally, modern EVs with connected systems must meet evolving cybersecurity regulations like UNECE R155 and R156, which mandate risk assessments and software updates throughout the vehicle’s lifecycle.

Charging Infrastructure and Deployment Logistics

Site Preparation and Grid Integration

Deploying the largest EVs (e.g., electric mining trucks or articulated buses) demands robust charging infrastructure. Key considerations include:

– On-site transformers and substations to handle high-power (e.g., 350 kW to 1+ MW) charging

– Coordination with utility providers for grid upgrades

– Compliance with electrical codes (e.g., NEC in the U.S., IEC 60364 internationally)

Charging Equipment Certification

All charging stations and connectors must be certified to relevant standards:

– CCS, CHAdeMO, or GB/T depending on region

– IEC 61851 (EV charging systems)

– UL 2594 or EN 61980 for wireless power transfer (if applicable)

End-of-Life and Battery Recycling

Battery Take-Back and Recycling Compliance

EV manufacturers and operators must comply with battery recycling mandates such as:

– EU Battery Directive (updated as EU Battery Regulation 2023)

– U.S. EPA guidelines and state-specific rules (e.g., California’s SB 244)

– China’s regulations on traceability and recycling quotas

Battery management systems (BMS) should enable tracking from cradle to grave, supporting compliance with extended producer responsibility (EPR) laws.

Second-Life Applications and Repurposing

Used EV batteries may be repurposed for energy storage. Logistics must ensure safe disassembly, transportation, and re-certification of battery packs for second-life use, in accordance with safety and environmental regulations.

Documentation and Record-Keeping

Compliance Documentation

Maintain comprehensive records including:

– Certificate of Conformity (CoC)

– Battery test reports (UN38.3, MSDS)

– Transport permits and route approvals

– Maintenance logs and software update histories

– Recycling and disposal certifications

Digital compliance platforms can streamline audits and ensure traceability across the supply chain.

Conclusion

Logistics and compliance for the largest electric vehicles demand a multidisciplinary approach integrating transport engineering, regulatory expertise, and environmental stewardship. As global EV adoption grows, staying ahead of evolving standards and investing in compliant, scalable logistics solutions will be critical for operational success and sustainability.

In conclusion, sourcing from the largest electric vehicle (EV) manufacturers offers significant advantages in terms of technological innovation, production scale, supply chain reliability, and access to cutting-edge battery and software systems. Companies such as Tesla, BYD, Volkswagen Group, and General Motors are leading the global transition to sustainable transportation through substantial investments in R&D, strategic partnerships, and vertical integration. Sourcing from these industry leaders not only ensures high-quality components and vehicles but also positions businesses to benefit from long-term advancements in EV performance, affordability, and infrastructure support. However, it is essential to conduct thorough due diligence, considering geopolitical factors, supply chain diversification, and evolving regulatory landscapes. By strategically aligning with top EV manufacturers, organizations can enhance their sustainability goals, reduce carbon footprints, and remain competitive in the rapidly growing electric mobility market.