The global lithium market is experiencing unprecedented expansion, driven by surging demand for electric vehicles (EVs), energy storage systems, and portable electronics. According to a report by Mordor Intelligence, the lithium market was valued at approximately USD 7.1 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of over 12.5% from 2024 to 2029. This rapid growth is largely attributed to the accelerating transition toward clean energy and the increasing adoption of lithium-ion batteries across industries. As demand intensifies, a select group of manufacturers now dominate the global lithium supply chain, controlling a majority of extraction, refining, and production capacity. These companies not only shape the availability and pricing of lithium worldwide but also play a pivotal role in enabling the scalability of next-generation technologies. The following list highlights the top seven largest lithium manufacturers based on production volume, market share, and strategic influence, offering insight into the key players driving the future of energy storage and electrification.

Top 7 Largest Of Lithium Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Largest Of Lithium

H2 2026 Market Trends for the Largest Lithium Producers

As the global push toward electrification intensifies, the lithium market is poised for significant shifts in the second half of 2026. For the largest lithium producers—such as Albemarle, SQM, Ganfeng Lithium, Tianqi Lithium, and Pilbara Minerals—H2 2026 is expected to be defined by a complex interplay of supply dynamics, technological advancements, and evolving demand patterns.

Supply Rebalancing and Pricing Volatility

By H2 2026, the lithium market is projected to transition from a period of oversupply (which characterized much of 2024–2025) toward a more balanced state. Major producers will have completed capacity expansions, particularly in Chile (SQM, Albemarle), Australia (Pilbara, Tianqi), and China (Ganfeng). However, disciplined production management and the closure of high-cost operations may tighten supply. Lithium carbonate equivalent (LCE) prices are expected to stabilize between $18,000–$25,000/ton, up from 2025 lows but below 2022 peaks. This rebound will improve margins for low-cost producers with vertically integrated operations.

Demand Growth Driven by EVs and Energy Storage

Electric vehicle (EV) sales are forecast to grow at 18–22% year-on-year in H2 2026, especially in emerging markets like India, Southeast Asia, and Latin America. China remains the largest market, with strong policy support for NEVs (New Energy Vehicles). Simultaneously, grid-scale and residential energy storage systems (ESS) will become a major demand driver, accounting for nearly 30% of lithium consumption. This diversified demand base will reduce reliance on the passenger EV sector, offering more predictable revenue streams for top producers.

Strategic Shifts Toward Vertical Integration and Partnerships

The largest lithium companies are increasingly securing downstream partnerships with battery makers (e.g., CATL, LG Energy Solution, Northvolt) and automakers (e.g., Tesla, BMW, Ford). In H2 2026, we expect more long-term supply agreements (LTSAs) with take-or-pay clauses, ensuring stable demand. Additionally, major producers are investing in lithium conversion facilities and battery recycling to capture more value along the supply chain. Ganfeng and Albemarle, for instance, are expanding hydroxide refining capacity to meet demand for NMC (Nickel-Manganese-Cobalt) cathodes.

Technological and Environmental Pressures

Pressure to reduce the environmental impact of lithium extraction—especially in water-stressed regions like the Atacama Desert—will accelerate adoption of direct lithium extraction (DLE) technologies. SQM and Albemarle are piloting DLE projects, which could significantly improve recovery rates and reduce brine depletion. Regulatory scrutiny in South America and Australia will push producers toward greater ESG (Environmental, Social, Governance) transparency, affecting investment decisions and social license to operate.

Geopolitical and Trade Dynamics

Geopolitical tensions will continue to influence market access and trade flows. U.S. and EU policies favoring onshoring of battery materials (e.g., Inflation Reduction Act, Critical Raw Materials Act) will incentivize partnerships between Western automakers and non-Chinese lithium suppliers. However, Chinese firms like Ganfeng and Tianqi maintain strong footholds in Africa (e.g., Zimbabwe, Congo) and South America, giving them strategic leverage. Trade restrictions or tariffs could fragment the market, prompting producers to diversify geographic exposure.

Conclusion

In H2 2026, the largest lithium producers will operate in a more stable but highly competitive environment. Success will depend on cost leadership, technological innovation, supply chain integration, and adaptability to shifting regulatory landscapes. While price volatility may persist, the long-term fundamentals for lithium remain strong, driven by global decarbonization goals. Companies that have invested in sustainable extraction, recycling, and downstream capabilities will be best positioned to capture value in the evolving energy transition economy.

Common Pitfalls When Sourcing the Largest of Lithium (Quality, IP)

When sourcing lithium—especially high volumes required for sectors like electric vehicles or energy storage—companies often focus on securing the “largest” supply, prioritizing scale over other critical factors. However, this approach can lead to significant risks related to quality consistency and intellectual property (IP) protection. Below are key pitfalls to avoid:

Overlooking Quality Variability Despite Volume

One of the biggest risks in sourcing large quantities of lithium is assuming that scale equates to consistent quality. Lithium sourced from different mines or processed through varying methods can differ significantly in purity, chemical composition, and suitability for specific applications (e.g., battery-grade vs. industrial-grade).

- Pitfall: Accepting bulk lithium without stringent quality control agreements or third-party verification.

- Consequence: Inconsistent battery performance, increased rejection rates, or costly reprocessing.

- Best Practice: Implement strict quality assurance protocols, including certificates of analysis (CoA), batch testing, and on-site audits of suppliers.

Ignoring Origin and Processing Transparency

Lithium from different geographic sources (e.g., South American brines vs. Australian hard rock) involves different extraction methods and environmental impacts. Sourcing the largest volume from a low-cost supplier may compromise traceability and ethical sourcing standards.

- Pitfall: Failing to audit the supply chain for environmental, social, and governance (ESG) compliance.

- Consequence: Brand damage, regulatory penalties, or supply chain disruptions.

- Best Practice: Require full chain-of-custody documentation and prioritize suppliers with transparent, sustainable practices.

Underestimating Intellectual Property Risks

When integrating lithium into advanced technologies (e.g., solid-state batteries), the processing techniques, formulations, or cell designs may involve proprietary IP. Sourcing lithium from partners without clear IP agreements can expose companies to legal disputes or loss of competitive advantage.

- Pitfall: Not defining IP ownership in supplier contracts—especially for co-developed materials or processes.

- Consequence: Loss of patent rights, trade secret exposure, or inability to scale proprietary technologies.

- Best Practice: Include robust IP clauses in supplier agreements, specifying ownership, confidentiality, and permitted use of jointly developed innovations.

Relying on Single or Geopolitically Risky Suppliers

Pursuing the largest volume may lead to over-dependence on a single supplier or region, increasing vulnerability to geopolitical instability, export restrictions, or logistical bottlenecks.

- Pitfall: Concentrating supply from one country or mining operation without diversification.

- Consequence: Supply chain disruption, price volatility, or forced reliance on lower-quality alternatives.

- Best Practice: Diversify sourcing across multiple regions and maintain buffer inventories or alternative suppliers.

Failing to Align Technical Specifications with End Use

Not all lithium is created equal. Battery manufacturers require lithium carbonate or hydroxide with ultra-low impurity levels. Sourcing large volumes of substandard material can undermine product performance.

- Pitfall: Accepting off-spec material due to volume discounts or urgent demand.

- Consequence: Reduced battery cycle life, safety issues, or failure to meet regulatory standards.

- Best Practice: Define precise technical specifications upfront and enforce them through contractual penalties for non-compliance.

Conclusion

While securing large volumes of lithium is essential for scaling operations, prioritizing size over quality and IP safeguards can compromise product integrity, innovation, and long-term competitiveness. A strategic sourcing approach balances volume with rigorous quality controls, transparent supply chains, and strong IP protections.

Logistics & Compliance Guide for the Largest of Lithium

Handling the largest forms of lithium—whether in bulk quantities, high-capacity batteries (such as those used in electric vehicles or energy storage systems), or large-scale industrial lithium compounds—requires strict adherence to safety, logistics, and regulatory compliance standards. This guide outlines key considerations for the safe and compliant transport, storage, and handling of large lithium shipments.

Regulatory Framework and Classification

Lithium and lithium-based products are subject to international and national regulations due to their hazardous properties, particularly flammability and reactivity. Key regulatory bodies include:

- International Air Transport Association (IATA) – For air transport of lithium batteries and materials.

- International Maritime Organization (IMO) – For sea freight via the IMDG Code.

- U.S. Department of Transportation (DOT) – Regulates domestic and international transport within U.S. jurisdictions.

- European Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) – For road transport in Europe.

- UN Recommendations on the Transport of Dangerous Goods – Provide the global foundation for classification.

Lithium metals and lithium-ion batteries are typically classified under:

– UN 3090 – Lithium metal batteries (and battery packs)

– UN 3480 – Lithium-ion batteries (and battery packs)

Large-format batteries (e.g., EV traction batteries) often fall under these classifications and require full hazardous materials (hazmat) compliance.

Packaging and Containment Requirements

For large lithium shipments, packaging must:

– Prevent short circuits and physical damage.

– Contain thermal runaway risks (especially for lithium-ion).

– Withstand vibration, pressure changes, and environmental exposure.

Specific requirements include:

– Use of rigid outer packaging with internal cushioning.

– Individual protection for each battery or cell (insulation, spacing).

– Proper venting for large battery systems to prevent pressure buildup.

– Compliance with IEC 62133, UN 38.3 testing for lithium batteries (mandatory for air transport).

Large industrial lithium compounds (e.g., lithium carbonate, hydroxide) must be stored in sealed, corrosion-resistant containers to prevent moisture absorption and reactivity.

Transportation Modes and Restrictions

Air Transport

- Passenger Aircraft: Generally prohibited for large quantities of lithium metal batteries (UN 3090).

- Cargo Aircraft: Permitted with weight limits, state-of-charge restrictions (typically ≤30% for lithium-ion), and full documentation.

- Strongly regulated under IATA Dangerous Goods Regulations (DGR), including labeling, marking, and crew notification.

Sea Freight

- Governed by the IMDG Code.

- Requires proper stowage (away from heat sources and incompatible materials).

- Large battery containers must be marked with Class 9 hazard labels and UN numbers.

- Documentation includes Dangerous Goods Declaration and container packing certificates.

Road and Rail

- ADR (Europe) and DOT 49 CFR (U.S.) apply.

- Vehicles must display proper placards (Class 9 for miscellaneous dangerous goods).

- Drivers require hazmat endorsement and training.

- Segregation from flammable materials and oxidizers is mandatory.

Storage and Handling Protocols

- Facilities must be dry, well-ventilated, and temperature-controlled (ideally 15–25°C).

- Fire suppression systems should include Class D fire extinguishers (for lithium metal fires) and non-conductive agents.

- Segregation from water, acids, and oxidizing agents is critical—lithium reacts violently with moisture.

- Handling equipment must be non-sparking and grounded to prevent static discharge.

- Personnel require training in lithium-specific hazards, emergency response, and PPE usage.

Documentation and Compliance

Essential documentation includes:

– Safety Data Sheets (SDS) – Updated and compliant with GHS.

– Transport Documents – Clearly stating UN number, proper shipping name, hazard class, and packing group.

– Dangerous Goods Declaration – Required for air and sea.

– Special permits or approvals – For prototype or damaged batteries, or non-standard packaging.

For large shipments, advance notification to carriers and authorities may be required.

Incident Response and Emergency Preparedness

- Emergency plans must address thermal runaway, fire, and chemical exposure.

- Spill kits for lithium compounds should include dry sand or Class D extinguishing media—never use water on lithium metal fires.

- Training drills for staff handling large lithium materials.

- Reporting of incidents to regulatory authorities as required (e.g., DOT, ECHA).

Sustainability and End-of-Life Considerations

- Used or defective lithium batteries are classified as hazardous waste.

- Transport for recycling must follow hazardous waste regulations (e.g., Basel Convention for international movement).

- Proper labeling as “Used Lithium Batteries” or “Defective” with applicable UN numbers.

Conclusion

Managing the logistics of the largest forms of lithium demands rigorous compliance, specialized handling, and proactive risk management. By adhering to international standards, investing in proper training, and maintaining meticulous documentation, companies can ensure the safe and legal transport and storage of large-scale lithium materials. Always consult the latest regulatory updates and engage certified dangerous goods professionals when planning large lithium shipments.

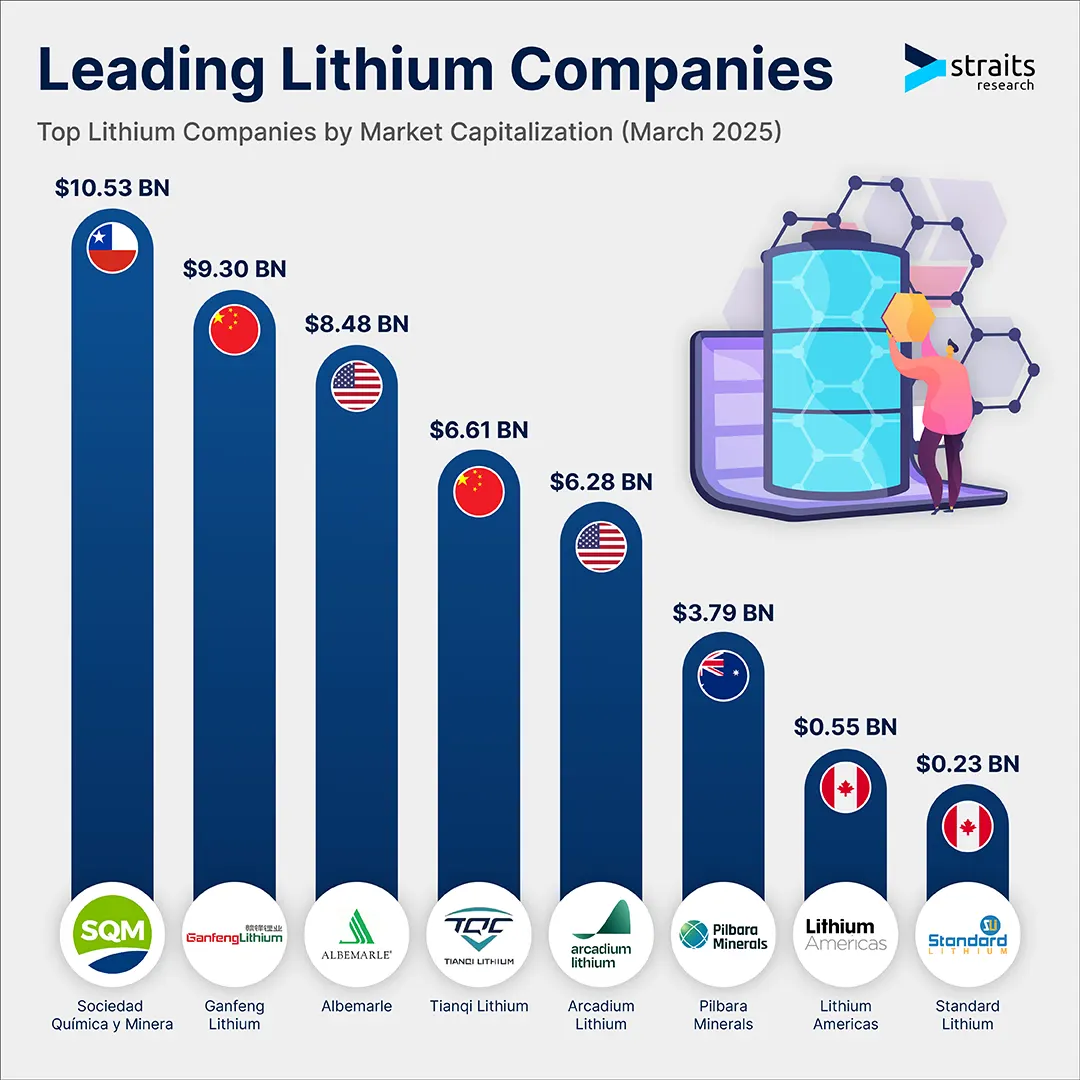

In conclusion, sourcing from the largest supplier of lithium requires a strategic evaluation that goes beyond size and production volume. While companies like Albemarle Corporation, SQM (Sociedad Química y Minera de Chile), and Ganfeng Lithium currently lead global lithium supply, selecting the optimal partner involves considering factors such as supply chain reliability, sustainability practices, geopolitical risks, pricing stability, and long-term contractual flexibility. Additionally, geographic diversification and investments in environmentally responsible extraction methods are becoming increasingly critical in light of growing demand from the electric vehicle and renewable energy sectors. Therefore, while aligning with a top-tier lithium supplier offers advantages in scale and market influence, a balanced sourcing strategy should emphasize resilience, ethical sourcing, and partnership alignment with future technological and regulatory trends.