The global financing services market is undergoing rapid transformation, driven by increasing digitalization, rising demand for alternative lending solutions, and growing fintech innovation. According to Grand View Research, the global fintech market size was valued at USD 110.4 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 19.8% from 2023 to 2030. Similarly, Mordor Intelligence forecasts the financial services market to grow at a CAGR of over 7.5% during the period 2023–2028, fueled by expanding access to credit, regulatory support, and technological advancements such as AI-driven underwriting and blockchain-based transactions. Within this evolving landscape, a select group of manufacturers and service providers have emerged as leaders—companies that not only offer scalable financing solutions but also integrate data analytics, automation, and customer-centric platforms to serve businesses and consumers worldwide. These top nine financing services manufacturers represent the vanguard of innovation, capturing significant market share through strategic partnerships, product diversification, and global reach—positioning them at the forefront of the next era in financial services.

Top 9 Financing Services Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Financing Services

2026 Market Trends in Financing Services

As we approach 2026, the global financing services sector is undergoing a profound transformation driven by technological innovation, shifting consumer expectations, regulatory evolution, and macroeconomic dynamics. Key trends are reshaping how capital is accessed, managed, and deployed across individuals and businesses.

Accelerated Digital Transformation and Embedded Finance

Financial institutions are aggressively investing in digital platforms, artificial intelligence, and cloud infrastructure to enhance customer experience and operational efficiency. By 2026, embedded finance—where financial services are seamlessly integrated into non-financial platforms such as e-commerce, automotive, and SaaS—will become mainstream. This trend enables point-of-sale lending, insurance, and payment solutions directly within consumer workflows, blurring traditional industry boundaries and creating new revenue streams.

Rise of AI-Driven Risk Assessment and Personalization

Artificial intelligence and machine learning are revolutionizing credit underwriting and customer service. Alternative data sources—such as cash flow patterns, social behavior, and transaction history—are being leveraged to assess creditworthiness, particularly for underserved segments. AI-powered chatbots and virtual financial advisors offer personalized product recommendations and real-time support, improving accessibility and customer engagement while reducing operational costs.

Sustainable and ESG-Linked Financing Gains Momentum

Environmental, Social, and Governance (ESG) criteria are becoming central to lending and investment decisions. By 2026, a significant portion of corporate financing will be tied to sustainability performance, with green loans, sustainability-linked bonds, and impact investing experiencing robust growth. Regulatory pressure, investor demand, and corporate net-zero commitments are driving financial institutions to develop transparent ESG frameworks and reporting standards.

Expansion of Alternative Lending and Decentralized Finance (DeFi)

Traditional bank lending faces increasing competition from fintech lenders, peer-to-peer platforms, and blockchain-based DeFi protocols. These alternatives offer faster, more flexible financing—particularly for SMEs and gig economy workers. While regulatory scrutiny of DeFi remains a challenge, hybrid models combining decentralized technology with compliant structures are expected to gain traction, especially in cross-border transactions and asset tokenization.

Regulatory Evolution and Cybersecurity Prioritization

Regulators worldwide are adapting frameworks to address digital innovation, data privacy, and systemic risks. Open banking regulations are expanding beyond Europe and the UK, promoting data sharing and competition. Simultaneously, as cyber threats grow in sophistication, financial institutions are prioritizing cybersecurity investments and resilience planning, making robust digital security a competitive differentiator.

Persistent Macroeconomic Uncertainties

Interest rate volatility, inflationary pressures, and geopolitical tensions will continue to influence financing costs and risk appetites in 2026. Lenders are adopting more dynamic pricing models and stress-testing portfolios against multiple economic scenarios. This environment favors agile, data-driven institutions capable of adjusting strategies rapidly.

In conclusion, the 2026 financing services landscape will be defined by innovation, inclusivity, and resilience. Institutions that embrace digital transformation, prioritize customer-centric solutions, and align with sustainability goals will be best positioned to thrive in an increasingly competitive and interconnected financial ecosystem.

Common Pitfalls in Sourcing Financing Services: Quality and Intellectual Property Concerns

When sourcing financing services—whether through third-party lenders, fintech platforms, or financial intermediaries—organizations often focus heavily on interest rates and speed of funding while overlooking critical risks related to service quality and intellectual property (IP). These oversights can lead to long-term financial, legal, and operational consequences.

Poor Service Quality and Lack of Transparency

One of the most frequent pitfalls is engaging financing partners that deliver substandard service. This may manifest as delayed disbursements, poor customer support, or opaque fee structures. Providers with inadequate operational infrastructure may fail to meet service level agreements, leading to cash flow disruptions. Additionally, a lack of transparency in terms and conditions—such as hidden penalties or variable interest rate mechanisms—can undermine financial planning and result in unexpected costs.

Inadequate Due Diligence on Provider Credibility

Organizations often rush into agreements without thoroughly vetting the financial health, regulatory compliance, or reputation of financing service providers. This increases the risk of partnering with entities prone to insolvency, regulatory violations, or unethical practices. A provider’s failure to comply with financial regulations (e.g., anti-money laundering or consumer protection laws) can also expose the client to indirect liability.

Intellectual Property Risks in Financing Agreements

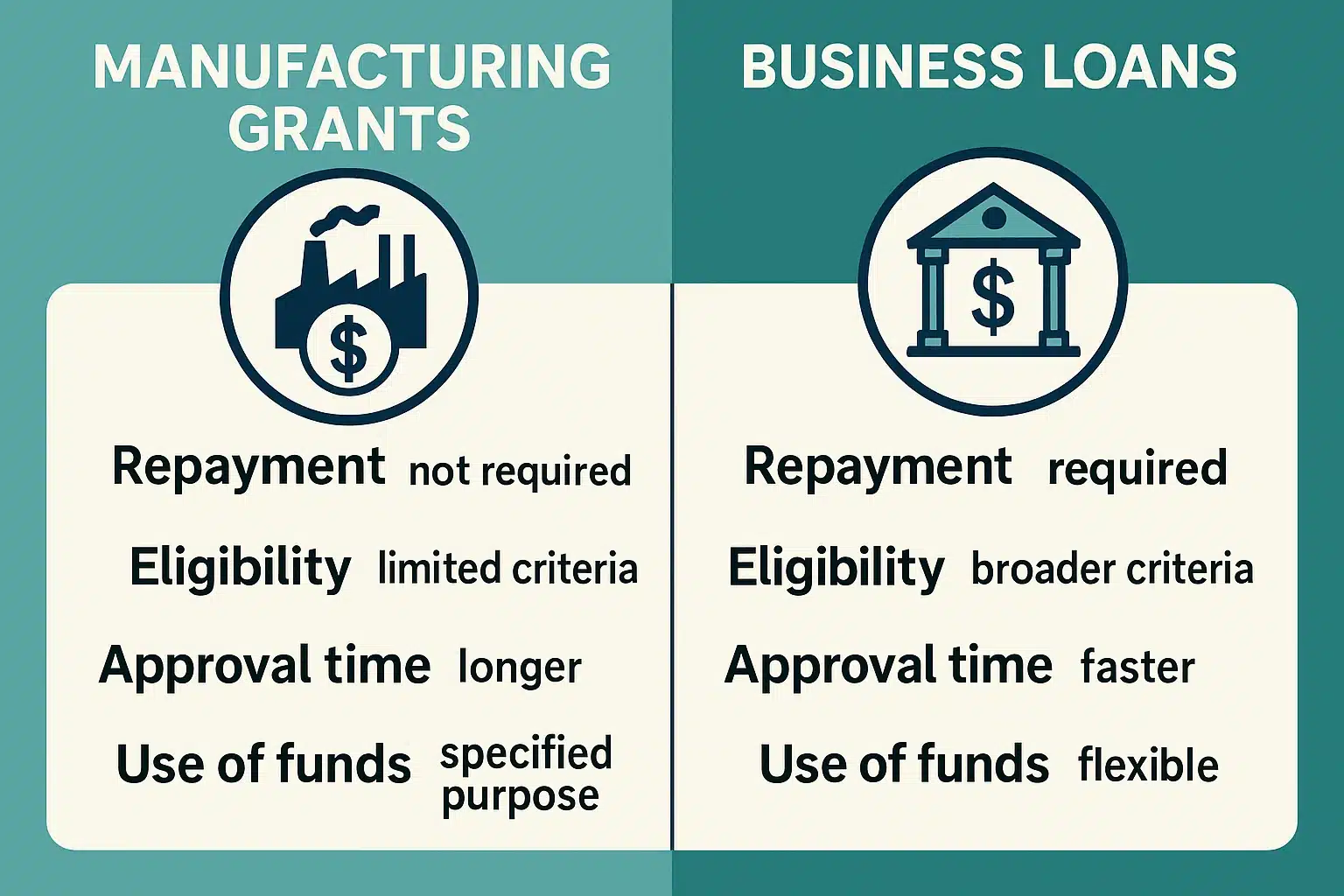

A less obvious but significant risk involves intellectual property. Some financing arrangements, especially in venture debt or revenue-based financing, may include clauses that grant lenders security interests in company assets—including IP. If not carefully reviewed, these agreements can place core innovations, trademarks, or proprietary technology at risk in the event of default. In extreme cases, lenders might gain control over IP, undermining a company’s competitive advantage.

Ambiguous IP Ownership in Co-Development Scenarios

When financing is tied to collaborative projects—such as innovation grants or joint development funding—ambiguities in IP ownership can arise. Financing contracts may inadvertently assign rights to newly developed IP to the lender or third-party funder unless explicitly negotiated otherwise. Without clear contractual terms, businesses may lose control over valuable innovations created using funded resources.

Data Privacy and Confidentiality Breaches

Financing services often require access to sensitive financial and operational data. Providers with weak data governance practices may expose client information to breaches or unauthorized use. Inadequate contractual safeguards around data handling and confidentiality increase the risk of intellectual property leakage or competitive harm.

Mitigation Strategies

To avoid these pitfalls, organizations should conduct comprehensive due diligence on financing partners, insist on transparent and auditable service standards, and involve legal experts to review all contractual terms—especially those related to IP, data rights, and default provisions. Clear definitions of IP ownership, limitations on collateral, and robust data protection clauses are essential to safeguarding long-term business interests.

Logistics & Compliance Guide for Financing Services

This guide outlines key logistics and compliance considerations for organizations offering financing services. Adhering to these standards ensures operational efficiency, regulatory adherence, and risk mitigation.

Regulatory Compliance Framework

All financing operations must comply with applicable local, national, and international regulations. Key areas include anti-money laundering (AML), know your customer (KYC), consumer protection laws, data privacy (e.g., GDPR, CCPA), and financial reporting standards. Institutions must establish a robust compliance program, including regular audits, staff training, and documented policies.

Licensing and Authorization

Financing service providers must obtain and maintain all required licenses and authorizations from relevant financial regulatory bodies (e.g., SEC, FCA, FinCEN). Operating without proper licensing can result in penalties, legal action, and reputational damage. License requirements vary by jurisdiction and service type (e.g., lending, leasing, factoring).

Customer Due Diligence (CDD) and KYC Procedures

Implement comprehensive KYC processes to verify customer identities before initiating services. Collect and validate government-issued IDs, proof of address, and financial statements where applicable. Conduct ongoing monitoring to detect suspicious activity and update customer information periodically.

Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF)

Establish an AML/CTF program that includes risk assessment, transaction monitoring, suspicious activity reporting (SAR), and recordkeeping. Use automated systems to flag high-risk transactions and ensure staff are trained to recognize red flags. Report suspicious activities to the appropriate financial intelligence units.

Data Security and Privacy

Protect customer financial and personal data through encryption, secure storage, access controls, and cybersecurity protocols. Ensure compliance with data protection laws by obtaining informed consent, limiting data use, and providing transparency about data handling practices. Conduct regular security audits and vulnerability assessments.

Contractual and Disclosure Requirements

Provide clear, transparent terms and conditions for all financing agreements. Disclosures must include interest rates, fees, repayment schedules, default consequences, and consumer rights. Contracts should be legally enforceable and compliant with consumer finance regulations such as Truth in Lending (TILA) or equivalent.

Risk Management and Internal Controls

Develop internal controls to mitigate operational, credit, and fraud risks. Implement segregation of duties, approval workflows, and audit trails. Conduct regular risk assessments and stress testing for loan portfolios. Maintain adequate insurance coverage and contingency plans.

Recordkeeping and Audit Trail

Retain all customer records, transaction logs, compliance documents, and communications for the legally mandated period (typically 5–7 years). Ensure records are accurate, complete, and securely stored. Prepare for internal and external audits with organized documentation and reporting systems.

Cross-Border and International Compliance

When operating across jurisdictions, comply with international regulations such as FATF recommendations, OFAC sanctions, and local financial laws. Perform enhanced due diligence on cross-border transactions and monitor for sanctioned entities. Use global watchlist screening tools.

Reporting and Regulatory Filings

Submit required reports to regulatory authorities on time, including loan disclosures, suspicious activity reports, and financial statements. Maintain a compliance calendar to track reporting deadlines and ensure accuracy in submissions.

Adherence to this logistics and compliance guide ensures that financing services operate ethically, legally, and sustainably while protecting both the institution and its customers.

Conclusion: Sourcing Manufacturer Financing Services

Sourcing manufacturer financing services is a strategic move that can significantly enhance operational efficiency, cash flow management, and scalability for businesses involved in manufacturing or product development. By partnering with reliable financiers, companies can overcome capital constraints, invest in essential equipment and inventory, and accelerate time-to-market without depleting internal resources.

Key benefits include improved liquidity, flexible repayment terms aligned with production cycles, and access to expertise in supply chain financing. However, success in sourcing these services depends on thorough due diligence—evaluating lenders’ credibility, understanding the terms and costs involved, and ensuring alignment with long-term business goals.

Ultimately, effective manufacturer financing supports sustainable growth, strengthens supplier relationships, and enhances competitive advantage. Businesses that proactively identify and integrate the right financing solutions position themselves for resilience and scalability in dynamic market environments. Therefore, manufacturer financing should be viewed not just as a funding tool, but as a core component of strategic supply chain and operations planning.