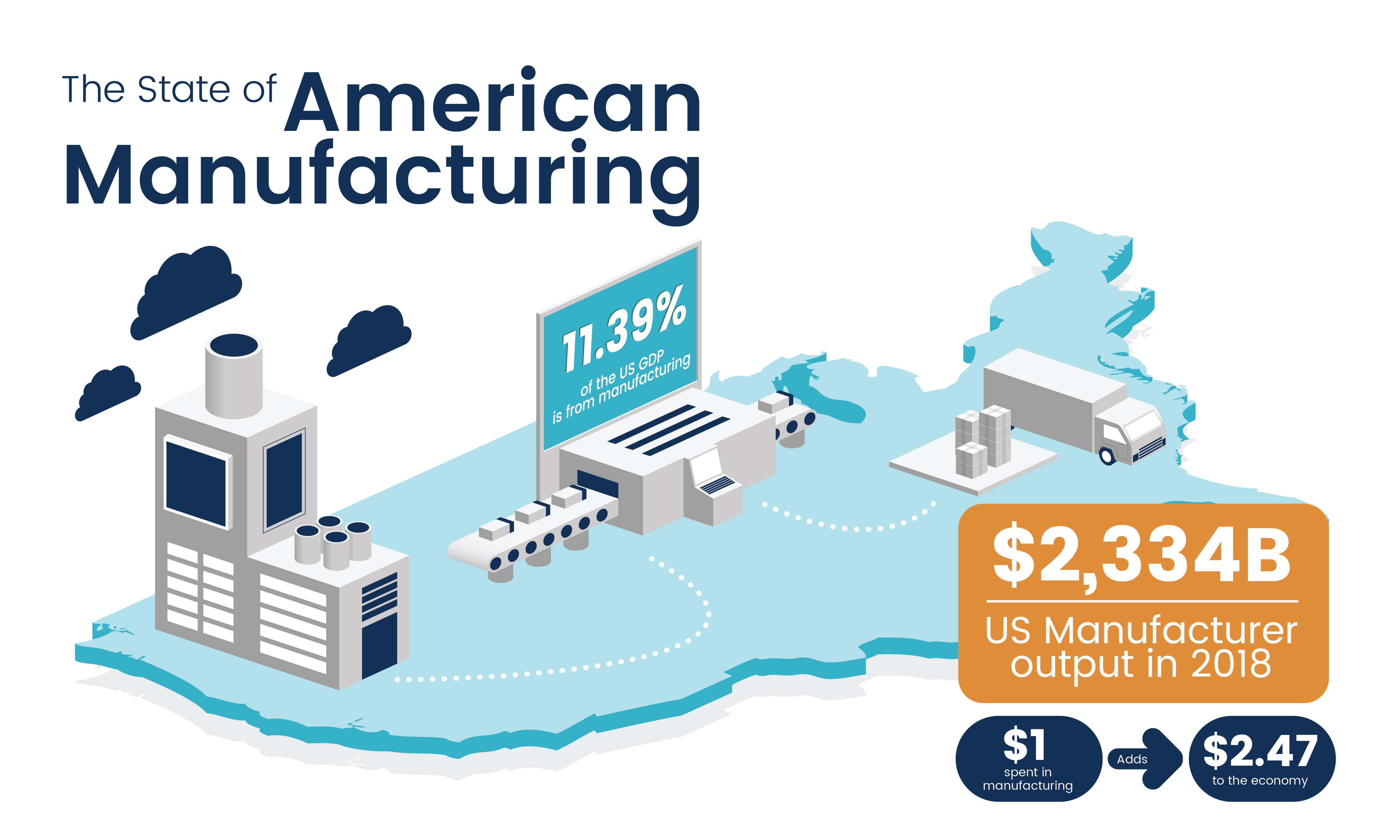

The U.S. manufacturing sector continues to demonstrate resilience and growth, driven by advancements in automation, reshoring initiatives, and strong domestic demand. According to Grand View Research, the U.S. manufacturing market was valued at approximately $2.3 trillion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 3.1% from 2023 to 2030. Similarly, Mordor Intelligence forecasts steady growth, citing increased investments in smart manufacturing technologies and supply chain localization as key drivers. As the industry evolves, a select group of manufacturers are leading innovation, efficiency, and scale across critical sectors—from aerospace and automotive to medical devices and industrial equipment. Based on market share, revenue performance, production capacity, and technological advancement, here are the top 10 manufacturers in the United States shaping the future of industrial output.

Top 10 In The Us Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for In The Us

2026 U.S. Market Trends: Key Projections and Shifts

As the U.S. economy approaches 2026, businesses, investors, and policymakers are closely monitoring a confluence of macroeconomic, technological, and social forces poised to reshape the marketplace. While forecasting involves inherent uncertainty, several robust trends are expected to define the commercial landscape in the coming years.

Economic and Inflation Dynamics

By 2026, the U.S. economy is projected to stabilize following the volatility of the early 2020s. The Federal Reserve is expected to maintain a data-driven approach, with interest rates likely settling into a “higher for longer” range compared to pre-pandemic norms. Inflation should moderate toward the Fed’s 2% target, but structural factors—such as supply chain reconfiguration and wage pressures in tight labor markets—may keep core inflation slightly elevated. Consumers will likely remain cautious, favoring value-oriented brands and private labels, especially in essential goods sectors.

Labor Market Evolution

The labor market is anticipated to remain competitive, with automation and AI driving a shift in workforce demand. High-skilled roles in technology, healthcare, and renewable energy will see strong growth, while routine administrative and manufacturing jobs face continued automation pressure. Employers will increasingly focus on upskilling, hybrid work models, and employee well-being to attract and retain talent. The gig economy will expand, supported by regulatory and benefit innovations.

Technology and AI Integration

Artificial intelligence is expected to be deeply embedded across industries by 2026. From generative AI in customer service and content creation to machine learning in supply chain optimization, businesses that leverage AI effectively will gain significant competitive advantages. Investment in cybersecurity, quantum computing readiness, and edge computing will accelerate, driven by the need for speed, privacy, and resilience.

Sustainability and ESG Imperatives

Environmental, Social, and Governance (ESG) factors will become standard business practice rather than optional initiatives. Regulatory pressures, including potential federal climate disclosure rules, and investor expectations will compel companies to demonstrate measurable sustainability progress. The clean energy transition—fueled by the Inflation Reduction Act—will drive growth in solar, wind, battery storage, and electric vehicle infrastructure, creating new markets and supply chain opportunities.

Consumer Behavior and Retail Transformation

Consumers in 2026 will demand hyper-personalization, convenience, and ethical transparency. E-commerce will continue growing, but with a renewed emphasis on seamless omnichannel experiences. Brick-and-mortar retail will focus on experiential offerings and localized services. Direct-to-consumer (DTC) brands will face increased competition, pushing innovation in customer engagement and supply chain efficiency.

Healthcare Innovation and Access

The healthcare sector will undergo significant transformation, driven by telehealth expansion, AI-powered diagnostics, and personalized medicine. Aging demographics will increase demand for long-term care and age-tech solutions. Cost containment will remain a priority, fostering growth in value-based care models and digital health platforms.

In summary, the 2026 U.S. market will be defined by adaptation—balancing economic resilience with technological disruption, evolving workforce needs, and rising sustainability expectations. Organizations that embrace agility, digital transformation, and ethical innovation are best positioned to thrive in this dynamic environment.

Common Pitfalls Sourcing in the US: Quality and Intellectual Property Risks

Sourcing products from the United States can offer benefits such as shorter lead times, strong regulatory compliance, and proximity. However, businesses—especially international buyers—can encounter significant challenges related to product quality and intellectual property (IP) protection. Understanding these pitfalls is critical to ensuring a successful sourcing strategy.

Quality Control Misconceptions

Many buyers assume that manufacturing in the US automatically guarantees superior product quality. While the US has stringent regulations and advanced manufacturing capabilities, this doesn’t eliminate quality risks. Pitfalls include inconsistent production standards across different suppliers, variability in raw material sourcing, and lack of rigorous in-process inspections. Relying solely on a supplier’s reputation without implementing independent quality audits or defined acceptance criteria can lead to defects, delays, and customer dissatisfaction.

Inadequate Supplier Vetting

A common mistake is failing to conduct thorough due diligence on US-based suppliers. Some companies operate with limited capacity, outdated equipment, or inexperienced staff, despite being located in a developed market. Without visiting facilities, reviewing certifications (e.g., ISO), and validating production capabilities, buyers may end up with underperforming partners. This is especially true in niche or highly specialized industries where supplier options are limited.

Intellectual Property Exposure

While the US has robust IP laws, enforcement relies heavily on proactive measures by the rights holder. A major pitfall is assuming that simply operating in the US safeguards your IP. Unauthorized use, reverse engineering, or supplier overproduction can occur if contracts lack clear IP clauses. Without non-disclosure agreements (NDAs), work-for-hire provisions, and explicit ownership language in manufacturing agreements, companies risk losing control of proprietary designs, formulas, or technology.

Weak Contractual Protections

Many sourcing agreements with US suppliers lack comprehensive terms around quality specifications, delivery timelines, and IP ownership. Verbal agreements or vague purchase orders are insufficient. Without detailed contracts that include penalties for non-compliance, audit rights, and clear resolution mechanisms, disputes become harder to resolve and can result in costly litigation or lost business.

Overreliance on Domestic Trust

Buyers, particularly from abroad, may place undue trust in US suppliers due to the country’s legal and business reputation. This complacency can lead to reduced oversight and monitoring. Regular performance reviews, on-site audits, and third-party testing remain essential—even when sourcing domestically—to ensure ongoing compliance with quality and contractual obligations.

Conclusion

Sourcing in the US offers advantages, but it is not immune to quality and IP risks. Businesses must treat US suppliers with the same level of scrutiny as international vendors—implementing strong contracts, conducting due diligence, and safeguarding intellectual property through legal and operational controls. Proactive risk management is key to avoiding costly setbacks and ensuring long-term success.

Logistics & Compliance Guide for Operating in the United States

Overview of U.S. Logistics Infrastructure

The United States features one of the most advanced and comprehensive logistics networks globally, supported by an extensive system of highways, railroads, airports, seaports, and distribution centers. Key logistics hubs include Los Angeles/Long Beach (largest U.S. port complex), Chicago (rail and freight hub), Memphis (air cargo, especially FedEx), and Atlanta (intermodal and highway connectivity). Understanding regional infrastructure is critical for optimizing transportation routes, minimizing transit times, and controlling costs.

Transportation Modes and Carrier Selection

Businesses can leverage multiple transportation modes:

– Trucking (FTL/LTL): Most common for domestic freight; requires working with licensed motor carriers compliant with FMCSA regulations.

– Rail: Cost-effective for bulk or long-distance freight; major providers include BNSF and Union Pacific.

– Air Freight: Ideal for high-value or time-sensitive shipments via carriers like FedEx, UPS, or commercial airlines.

– Ocean Freight: Primarily for international imports/exports; U.S. Customs and Border Protection (CBP) clearance is mandatory.

Always verify carrier licensing (MC number), insurance coverage, and compliance with Department of Transportation (DOT) standards.

Import Regulations and Customs Clearance

All goods entering the U.S. must clear U.S. Customs and Border Protection (CBP). Key requirements include:

– Entry Filing: Submit entry documentation (e.g., CBP Form 7501) through a licensed customs broker.

– Customs Bonds: Required for formal entries (values over $2,500 or regulated goods). Single-entry or continuous bonds are available.

– HTSUS Classification: Accurately classify products using the Harmonized Tariff Schedule of the United States to determine duties and eligibility for trade agreements.

– Origin and Marking: Goods must be properly marked with country of origin; rules of origin apply under USMCA and other trade pacts.

– Importer Security Filing (ISF): “10+2” rule requires importers to submit shipment data 24 hours before loading at origin.

Domestic Regulatory Compliance

Ensure adherence to federal and state regulations affecting logistics operations:

– Department of Transportation (DOT) Regulations: Govern vehicle safety, hours-of-service (HOS) for drivers, and hazardous materials transport (via Hazmat regulations under 49 CFR).

– Environmental Protection Agency (EPA): Regulates emissions and fuel standards; applicable to fleet operations.

– State-Level Requirements: Vary by state—examples include California’s CARB regulations, weight limits, and intrastate carrier licensing.

– Food and Drug Administration (FDA): Applies to food, pharmaceuticals, and medical devices; requires compliance with FSMA (Food Safety Modernization Act) for storage and transport.

Warehouse and Inventory Management

Warehousing operations must comply with:

– Occupational Safety and Health Administration (OSHA): Standards for workplace safety, including forklift operation, hazard communication, and fire prevention.

– Storage Regulations: Temperature-controlled environments for perishables or pharmaceuticals must meet FDA or USDA standards.

– Inventory Recordkeeping: Maintain accurate logs for audit purposes; use warehouse management systems (WMS) to track stock and ensure traceability.

Trade Compliance and Restricted Parties Screening

Avoid violations by:

– Screening Against Denied Parties Lists: Regularly check entities against OFAC’s SDN list, BIS’s Denied Persons List, and other federal restricted party databases.

– Export Controls: Governed by the Export Administration Regulations (EAR) and International Traffic in Arms Regulations (ITAR); apply when shipping sensitive technology or defense-related items.

– Record Retention: Maintain shipping, customs, and compliance records for a minimum of five years (CBP requirement).

Tax and Duty Management

Understand tax obligations related to logistics:

– Duties and Tariffs: Pay assessed duties based on HTSUS classification and country of origin; explore duty drawback programs for re-exports.

– Sales and Use Tax: Varies by state; nexus rules determine where tax collection is required. Economic nexus laws may apply based on sales volume.

– State Fuel and Freight Taxes: Carriers may be subject to IFTA (International Fuel Tax Agreement) reporting for fuel use across states.

Technology and Documentation Standards

Leverage technology to ensure accuracy and compliance:

– Electronic Data Interchange (EDI): Use standard formats (e.g., EDI 214 for shipment status, EDI 940/945 for warehouse orders) to streamline communication.

– Automated Manifest System (AMS): Required for electronic submission of cargo data to CBP before arrival.

– Track and Trace Systems: Implement GPS and IoT-enabled solutions for real-time shipment visibility and proof of delivery (POD).

Risk Management and Contingency Planning

Prepare for disruptions through:

– Insurance Coverage: Secure cargo, liability, and warehouse insurance.

– Incident Response Plans: Establish protocols for customs delays, cargo theft, natural disasters, or compliance audits.

– Vendor Audits: Regularly assess third-party logistics (3PL) providers for operational and compliance performance.

Conclusion

Successfully navigating U.S. logistics and compliance requires understanding federal regulations, selecting reliable partners, maintaining accurate documentation, and leveraging technology. Staying informed of regulatory updates from agencies like CBP, DOT, and FDA ensures long-term operational efficiency and legal compliance. Engaging qualified legal counsel or compliance consultants is recommended for complex supply chain operations.

In conclusion, sourcing manufacturers in the United States offers numerous strategic advantages for businesses seeking quality, reliability, and responsiveness. Domestic manufacturing provides shorter lead times, greater supply chain transparency, enhanced quality control, and easier communication due to shared time zones and language. It also supports faster time-to-market, reduces shipping costs and carbon footprint, and aligns with increasing consumer and regulatory demand for locally made products.

While labor and production costs may be higher compared to overseas alternatives, the long-term benefits—such as reduced risk, intellectual property protection, and operational agility—often outweigh the initial investment. Additionally, government initiatives and reshoring trends are bolstering the U.S. manufacturing sector, making it a more competitive and sustainable option.

Ultimately, sourcing from U.S. manufacturers can strengthen supply chain resilience, improve product quality, and enhance brand reputation. Businesses that prioritize control, speed, and sustainability should strongly consider domestic manufacturing as a core component of their sourcing strategy.