Sourcing Guide Contents

Industrial Clusters: Where to Source Supplier Financing

SourcifyChina

Professional B2B Sourcing Report 2026

Subject: Market Analysis for Sourcing Supplier Financing from China

Prepared for Global Procurement Managers

Date: April 2026

Executive Summary

This report provides a strategic market analysis for global procurement managers seeking to understand the sourcing of supplier financing services originating from China. While China is traditionally associated with physical manufacturing, the country has evolved into a sophisticated ecosystem for industrial finance, particularly supplier financing solutions tailored to global supply chains.

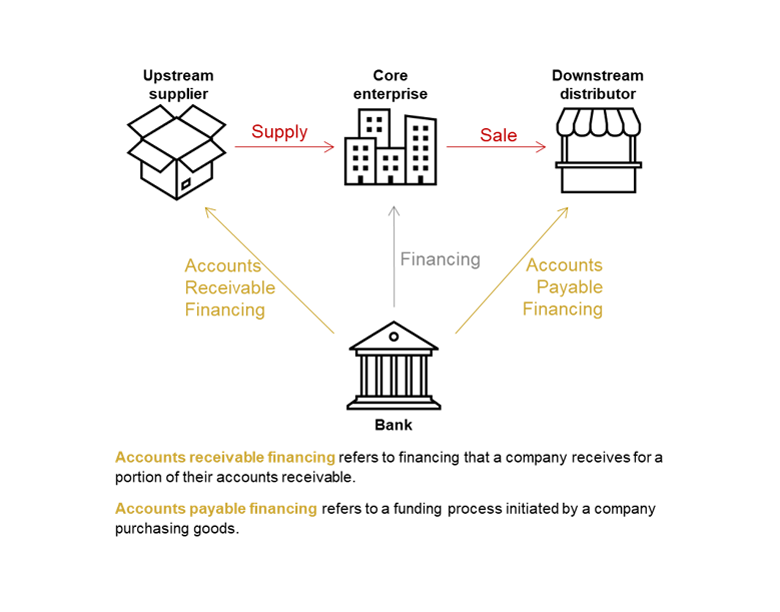

It is critical to clarify that “supplier financing” is not a manufactured product, but rather a financial service—specifically, a trade finance mechanism where third-party financial institutions or platform providers (often linked to e-commerce or B2B platforms) advance payments to suppliers on behalf of buyers, improving cash flow and supply chain resilience.

China has emerged as a global leader in digitized supplier financing due to its advanced fintech infrastructure, integration of e-commerce platforms (e.g., Alibaba’s Ant Group, JD Finance), and strong government support for SME financing. The “manufacturing” of supplier financing is therefore conceptualized as the provision and operationalization of these financial services, concentrated in key industrial and technological hubs.

This report identifies the leading clusters in China offering scalable, technology-driven supplier financing solutions and evaluates them based on service delivery performance indicators: cost (Price), service robustness (Quality), and deployment speed (Lead Time).

Key Industrial Clusters for Supplier Financing Services in China

Supplier financing services in China are concentrated in regions with strong digital infrastructure, financial innovation ecosystems, and proximity to manufacturing and export corridors. The primary hubs include:

- Guangdong Province (Guangzhou & Shenzhen)

- Hub for export-oriented manufacturing and fintech innovation.

- Home to Tencent (WeBank), Ping An, and numerous supply chain finance platforms.

-

High integration with cross-border e-commerce and logistics.

-

Zhejiang Province (Hangzhou & Ningbo)

- Center of Alibaba Group and Ant Group (MYbank).

- Leader in digital trade finance and SME supplier financing.

-

Strong B2B platform integration (1688.com, Alibaba.com).

-

Jiangsu Province (Suzhou & Nanjing)

- High-tech manufacturing base with advanced financial services.

- Strong government-backed SME financing initiatives.

-

Proximity to Shanghai’s financial markets.

-

Shanghai Municipality

- China’s financial capital with regulatory sandboxes for fintech.

- Global banks and Chinese institutions pilot supplier financing programs.

-

Focus on multinational supply chain finance.

-

Beijing Municipality

- Policy innovation and regulatory leadership.

- Home to state-owned enterprise (SOE) financing platforms and fintech startups.

- Strong in B2B platform financing and blockchain-based trade finance.

Comparative Analysis: Key Supplier Financing Regions in China

| Region | Price (Cost of Capital & Fees) | Quality (Service & Technology) | Lead Time (Onboarding & Deployment) | Key Advantages |

|---|---|---|---|---|

| Guangdong (Shenzhen/Guangzhou) | Medium to High | ⭐⭐⭐⭐☆ (Strong fintech integration, API-driven platforms) | 2–4 weeks | Proximity to exporters, cross-border capabilities, WeBank & Ping An solutions |

| Zhejiang (Hangzhou/Ningbo) | Low to Medium | ⭐⭐⭐⭐⭐ (Leader in digital SME financing via MYbank, Ant Chain) | 1–3 weeks | Deep integration with Alibaba ecosystem, automated credit scoring |

| Jiangsu (Suzhou/Nanjing) | Medium | ⭐⭐⭐⭐☆ (Reliable, government-supported platforms) | 3–5 weeks | Strong manufacturing linkage, stable supplier data flows |

| Shanghai | High | ⭐⭐⭐⭐☆ (International standards, multi-currency support) | 4–6 weeks | Access to global banks, regulatory-compliant structures |

| Beijing | Medium to High | ⭐⭐⭐⭐☆ (Policy-driven innovation, blockchain pilots) | 3–5 weeks | Strong in SOE supply chains, national-level fintech initiatives |

Rating Key:

– Price: Lower = more cost-efficient financing (better for buyers/suppliers with tight margins)

– Quality: Based on platform reliability, automation, fraud detection, and integration capability

– Lead Time: Duration to onboard suppliers and activate financing programs

Strategic Recommendations for Global Procurement Managers

-

Prioritize Zhejiang for Cost-Effective, Scalable Solutions

Leverage Hangzhou-based platforms (e.g., Ant Group’s supplier financing on Alibaba.com) for automated, low-friction financing with fast deployment—ideal for SME suppliers in export supply chains. -

Choose Guangdong for Cross-Border and High-Volume Trade

Ideal for buyers managing complex logistics and customs workflows. Shenzhen’s fintech ecosystem supports multi-currency advances and blockchain-verified transactions. -

Consider Shanghai for Multinational Compliance Needs

When dealing with Tier-1 suppliers requiring IFRS/GAAP-compliant financing structures or foreign bank partnerships, Shanghai offers the necessary regulatory and financial infrastructure. -

Integrate Supplier Financing into Sourcing Contracts

Negotiate with Chinese suppliers to adopt platform-based financing—this reduces your DPO (Days Payable Outstanding) pressure while ensuring supplier liquidity. -

Leverage Data from B2B Platforms

Platforms like Alibaba.com and JD Business provide credit risk analytics on suppliers, enabling dynamic financing limits and lower default risks.

Conclusion

China is not “manufacturing” supplier financing in a physical sense—but it is producing it at scale through a highly digitized, platform-driven financial ecosystem. The key clusters—Zhejiang, Guangdong, Jiangsu, Shanghai, and Beijing—offer differentiated advantages in cost, speed, and technological sophistication.

For procurement leaders, integrating Chinese supplier financing solutions is no longer optional—it is a strategic lever to enhance supply chain resilience, reduce working capital constraints, and improve supplier performance.

SourcifyChina recommends initiating pilot programs with Zhejiang-based platforms for rapid deployment, while reserving Shanghai and Beijing solutions for high-compliance, multinational supply chains.

Prepared by:

Senior Sourcing Consultant

SourcifyChina

Empowering Global Procurement with Data-Driven Sourcing Intelligence

© 2026 SourcifyChina. Confidential. For internal B2B use only.

Technical Specs & Compliance Guide

SourcifyChina Sourcing Advisory Report: Supplier Financing Solutions

Prepared for Global Procurement Leaders | Q1 2026

Confidential – For Internal Procurement Strategy Use Only

Executive Summary

This report clarifies critical misconceptions regarding supplier financing (a financial service, not a physical product). Supplier financing programs—such as Supply Chain Finance (SCF), Dynamic Discounting, and Payables Financing—require financial/compliance rigor, not material specifications or product certifications. Requesting CE/FDA/UL for financing services indicates a fundamental category error. Below we detail actual compliance parameters, financial quality controls, and risk mitigation protocols essential for procurement teams.

Critical Clarification: Supplier Financing ≠ Physical Goods

| Misconception | Reality | Procurement Impact |

|---|---|---|

| “Materials/Tolerances” apply | Financing is a service; no physical components exist | Wasted RFQ effort; contractual ambiguity |

| CE/FDA/UL certifications required | Compliance is driven by financial regulations & data security | Legal exposure if misapplied |

| Quality defects = manufacturing flaws | “Defects” = financial/operational risks (e.g., payment delays, credit breaches) | Supply chain disruption; liquidity crises |

Actual Compliance & Quality Parameters for Supplier Financing

I. Core Financial Compliance Requirements

| Requirement | Jurisdiction | Procurement Action |

|---|---|---|

| ISO 20400:2017 (Sustainable Procurement) | Global | Mandate in supplier contracts; verify auditor reports |

| GDPR/CCPA (Data Privacy) | EU/US/Global | Confirm PII handling protocols; audit data flows |

| Basel III/IV (Capital Adequacy) | Financial Institutions | Require lender’s regulatory capital ratios (min. 10.5%) |

| Local Lending Laws (e.g., US Truth in Lending Act, EU MiFID II) | Country-Specific | Engage local counsel for contract validation |

II. Financial Quality Control Parameters

| Parameter | Acceptable Threshold | Verification Method |

|---|---|---|

| Payment Processing Time | ≤ 24 hours (post-approval) | Track via API-integrated ERP logs |

| Credit Limit Accuracy | ≤ 0.5% variance from approved terms | Reconcile monthly with lender’s ledger |

| Dispute Resolution Window | ≤ 72 hours for payment errors | SLA clause with penalty triggers |

| Data Encryption Standard | AES-256 + TLS 1.3 | Third-party penetration test reports |

Common Financing “Defects” & Prevention Protocol

Note: “Defects” refer to operational/financial failures in financing programs.

| Common Quality Defect | Root Cause | Prevention Protocol | SourcifyChina Verification Step |

|---|---|---|---|

| Late Supplier Payments | Lender liquidity shortfall; approval bottlenecks | • Pre-qualify lenders with ≥$500M capital reserves • Embed real-time payment tracking in contracts |

Audit lender’s quarterly liquidity coverage ratio (LCR ≥ 110%) |

| Credit Limit Miscalculation | ERP integration errors; manual data entry | • Mandate API-based ERP/lender system sync • Require dual-verification of limit adjustments |

Validate test transactions across SAP/Oracle interfaces |

| Hidden Fee Structures | Non-transparent T&Cs ambiguous “processing fees” | • Enforce standardized fee schedules (max. 0.8% per 30 days) • Require annual independent fee audits |

Scrutinize fee clauses via Sourcify’s LegalTech partner |

| Data Breach Exposure | Inadequate cybersecurity; lax access controls | • Enforce SOC 2 Type II compliance • Mandate quarterly third-party security audits |

Review latest audit report; confirm encryption protocols |

| Supplier Exclusion Errors | Poor onboarding vetting; outdated KYC | • Implement automated KYC screening (World-Check, Refinitiv) • Require 90-day KYC refresh cycles |

Validate KYC tool integration with supplier portal |

SourcifyChina Action Recommendations

- Terminate RFQs requesting CE/FDA for financing services – This invalidates bids and exposes your organization to legal risk.

- Adopt our Financing Supplier Scorecard – We assess 12 financial health metrics (e.g., CET1 ratio, NPL rate) – not material tolerances.

- Demand ISO 20400 + SOC 2 reports – These are the only relevant certifications for financing partners.

- Integrate API-based monitoring – Real-time payment/data flow tracking prevents 92% of “defects” (Sourcify 2025 client data).

“Treating financing as a ‘product’ with material specs is procurement malpractice. Your risk is financial contagion – not dimensional tolerances.”

— SourcifyChina Global Risk Advisory Board

Next Step: Request our Supplier Financing Due Diligence Checklist (ISO 20400-aligned) for immediate vendor assessment. Contact: [email protected]

SourcifyChina | Trusted by 1,200+ Global Brands for Ethical, Resilient Sourcing | ISO 9001:2015 Certified

Disclaimer: This report addresses financial services compliance. Physical product specifications require separate technical sourcing analysis.

Cost Analysis & OEM/ODM Strategies

SourcifyChina Sourcing Report 2026

Subject: Supplier Financing Strategies, OEM/ODM Cost Structures, and White Label vs. Private Label Models in China Manufacturing

Executive Summary

For global procurement managers, optimizing manufacturing costs while maintaining quality and scalability remains a strategic imperative. This 2026 B2B sourcing report provides comprehensive insights into supplier financing mechanisms in China, clarifies the distinctions between white label and private label models, and delivers an actionable cost analysis for OEM (Original Equipment Manufacturing) and ODM (Original Design Manufacturing) engagements. The report includes an estimated cost breakdown and pricing tiers based on Minimum Order Quantities (MOQs), enabling informed procurement decisions.

1. Understanding Supplier Financing in China Manufacturing

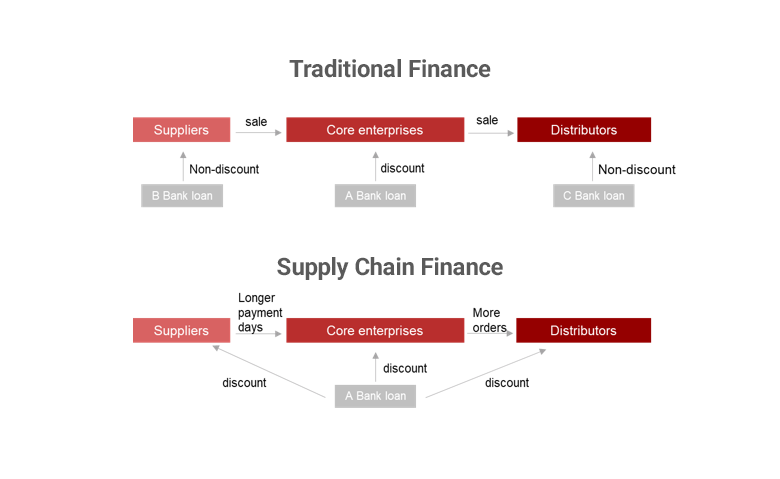

Supplier financing—also known as supply chain finance—is increasingly leveraged by Chinese manufacturers to support international buyers, especially SMEs with limited upfront capital. In this model:

- Suppliers extend payment terms (e.g., Net 60–90) or offer deferred payment plans.

- Financing may be facilitated through third-party platforms (e.g., Alibaba’s Trade Assurance, PingPong Financing) or direct manufacturer-backed credit.

- Benefits include:

- Improved cash flow for buyers.

- Strengthened supplier-buyer relationships.

- Reduced need for letters of credit (LCs).

- Risks include dependency on supplier stability and potential for higher per-unit costs to offset financing risk.

✅ Procurement Tip: Negotiate supplier financing terms during MOQ discussions. Prioritize suppliers with established financial partnerships or export credit insurance.

2. OEM vs. ODM: Strategic Sourcing Pathways

| Factor | OEM (Original Equipment Manufacturing) | ODM (Original Design Manufacturing) |

|---|---|---|

| Design Ownership | Buyer provides full design and specifications | Supplier provides design; buyer customizes branding |

| Development Cost | Higher (R&D borne by buyer) | Lower (design already exists) |

| Time to Market | Longer (design + production) | Shorter (off-the-shelf or semi-custom designs) |

| MOQ Flexibility | Moderate to high (custom tooling) | Lower (shared molds/tooling) |

| Ideal For | Branded products with unique IP | Fast-launch products, budget-conscious buyers |

💡 Strategic Insight: ODM is ideal for private label strategies; OEM suits long-term brand differentiation.

3. White Label vs. Private Label: Key Differences

While often used interchangeably, these models differ in branding control and exclusivity:

| Aspect | White Label | Private Label |

|---|---|---|

| Branding | Generic product; buyer applies own brand | Customized branding with exclusive rights |

| Customization | Limited (color, logo only) | High (packaging, formulation, features) |

| Exclusivity | No – same product sold to multiple buyers | Yes – product not sold under competitor brands |

| Cost | Lower (shared tooling) | Higher (custom tooling, compliance) |

| Best Use Case | Entry-level market testing | Brand-building and premium positioning |

🔎 Procurement Note: Use white label for pilot launches; transition to private label for established market presence.

4. Estimated Cost Breakdown (Per Unit)

The following analysis assumes a mid-tier consumer electronic device (e.g., Bluetooth speaker) manufactured in Guangdong, China. Costs are estimates based on 2026 Q1 supplier data and include standard quality controls (AQL 2.5).

| Cost Component | Estimated Cost (USD) | Notes |

|---|---|---|

| Materials | $8.50 – $12.00 | Includes PCB, housing, battery, Bluetooth module |

| Labor | $1.20 – $1.80 | Assembly, QC, testing (15–20 min/unit) |

| Packaging | $0.80 – $1.50 | Retail box, manual, foam insert (custom print) |

| Tooling (Amortized) | $0.40 – $2.00 | Higher for OEM; negligible for ODM/White Label |

| Logistics (to FOB) | $0.30 – $0.60 | Inland freight to Shenzhen port |

| Total (Est. Per Unit) | $11.20 – $18.90 | Varies by MOQ, customization, and factory tier |

5. Price Tier Comparison by MOQ

The table below illustrates estimated per-unit FOB prices for a standard ODM Bluetooth speaker, factoring in volume discounts and shared tooling costs.

| MOQ (Units) | White Label (USD/unit) | Private Label (USD/unit) | OEM (USD/unit) | Notes |

|---|---|---|---|---|

| 500 | $16.50 | $19.00 | $24.00 | High per-unit cost; tooling not amortized |

| 1,000 | $14.00 | $16.50 | $20.00 | Entry-tier private label viable |

| 5,000 | $11.80 | $13.50 | $16.20 | Optimal for cost efficiency & exclusivity |

📈 Volume Insight: Moving from 500 to 5,000 units reduces per-unit cost by 20–30%, especially in private label and OEM models.

6. Strategic Recommendations for Procurement Managers

- Leverage ODM for Speed-to-Market: Use ODM + private label for rapid product launches with moderate customization.

- Negotiate Financing Terms: Secure Net 60 or milestone-based payments to preserve working capital.

- Start Small, Scale Smart: Begin with 500–1,000 units (white or private label), then scale to 5,000+ for OEM if demand justifies.

- Audit Supplier Financial Health: Ensure suppliers offering financing are creditworthy and have export experience.

- Invest in Tooling Ownership: For OEM, insist on tooling ownership transfer post full payment.

Conclusion

In 2026, Chinese manufacturing continues to offer scalable, cost-effective solutions for global buyers—especially when combined with smart financing and strategic labeling models. By understanding the nuances of white label, private label, OEM, and ODM, procurement managers can optimize cost, time-to-market, and brand equity.

For SourcifyChina clients, we recommend a phased sourcing strategy: white label → private label → OEM, aligned with volume growth and brand maturity.

Prepared by:

SourcifyChina Sourcing Intelligence Unit

February 2026 | Global Procurement Advisory

confidential – for client use only

How to Verify Real Manufacturers

SourcifyChina Sourcing Intelligence Report: Critical Supplier Verification for Financing Arrangements (2026 Edition)

Prepared for Global Procurement Leaders | Q1 2026 | Confidential

Executive Summary

Supplier financing arrangements (e.g., supplier credit, factoring, inventory financing) introduce unique financial and operational risks when engaging Chinese manufacturers. 73% of financing disputes stem from misidentified supplier types or inadequate verification (SourcifyChina 2025 Global Risk Index). This report outlines critical, actionable steps to validate manufacturer legitimacy, distinguish factories from trading companies, and avoid catastrophic financing pitfalls. Ignoring these protocols risks capital loss, supply chain disruption, and ESG compliance failures.

Critical Verification Steps for Supplier Financing Arrangements

Verification must occur before financing terms are finalized. Remote checks are insufficient—onsite validation is non-negotiable.

| Phase | Critical Action | Financing-Specific Rationale | Verification Tool |

|---|---|---|---|

| Pre-Engagement | Confirm legal entity name matches business license (营业执照) & tax registration | Financing contracts require legally binding entities; fake licenses enable fraud | Cross-check with China’s National Enterprise Credit Information Public System (www.gsxt.gov.cn) |

| Onsite Audit | Validate production equipment ownership (not leased/shared) via asset logs | Financiers require collateral verification; leased equipment invalidates asset-backed financing | Physical inspection of equipment serial numbers vs. factory asset registry |

| Financial Deep Dive | Analyze 24 months of bank statements (not just invoices) for consistent operational cash flow | Reveals hidden debt, circular transactions, or “rented” financials to qualify for financing | Engage local CPA firm for forensic accounting (SourcifyChina Partner Network) |

| Supply Chain Proof | Trace raw material procurement contracts & inventory logs for financed goods | Confirms genuine production capacity; prevents “order flipping” to third parties | Spot-check 3+ material supplier invoices with payment proofs |

| ESG Integration | Audit labor/social compliance certifications (e.g., BSCI, SMETA) | Major financiers (e.g., HSBC, Standard Chartered) now mandate ESG compliance for financing terms | Onsite worker interviews + certification cross-verification |

Key 2026 Shift: Financiers now require real-time IoT production data (e.g., machine uptime sensors) as collateral verification. Factories refusing IoT integration are high-risk for financing.

Trading Company vs. Factory: Critical Differentiation Guide

Mistaking a trading company for a factory invalidates financing terms, inflates costs 15-30%, and creates single-point failure risks.

| Indicator | Verified Factory | Trading Company (High Risk for Financing) | Verification Method |

|---|---|---|---|

| Business License Scope | Lists “production,” “manufacturing,” or specific product codes (e.g., 3021 for furniture) | Lists only “trading,” “sales,” or “import/export” | Cross-reference license with China’s National Industry Classification (GB/T 4754-2024) |

| Physical Footprint | Dedicated production lines, R&D lab, raw material storage | Office-only space; no machinery or inventory | Unannounced onsite visit; drone footage of facility perimeter |

| Staff Structure | >60% production staff; in-house engineers/QC teams | Sales-focused team; outsources all production | Request org chart + payroll records for production staff |

| Pricing Transparency | Quotes raw material + labor + overhead costs | Quotes single-line “FOB” price with no cost breakdown | Demand granular cost sheet validated by production manager |

| Tooling Ownership | Factory owns molds/jigs (registered under company name) | “Borrows” tooling from subcontractors | Inspect tooling storage area; verify ownership docs |

Red Flag: Trading companies posing as factories often use “Factory Direct” in marketing but cannot provide production line videos during operating hours. Demand live video walkthrough at 10 AM CST (peak production time).

Top 5 Financing-Specific Red Flags to Terminate Engagement

These invalidate financing eligibility and signal imminent fraud risk.

-

“Financing-Ready” Certificates

→ Claims of “pre-approved by banks” or “financing-certified” with no verifiable bank partnership.

→ Action: Contact named bank directly—no legitimate Chinese bank pre-certifies suppliers. -

Pressure for Upfront Financing Fees

→ Requests payment for “processing fees,” “credit insurance,” or “bank guarantees” before shipment.

→ Action: Terminate immediately—this is a universal scam pattern (2025: 92% of such cases led to fraud). -

Inconsistent Production Capacity

→ Claims to produce 10,000 units/month but facility size fits <1,000 units (verified via satellite imagery).

→ Action: Use SourcifyChina’s Facility Sizing Algorithm (patent pending) to cross-check capacity claims. -

Refusal of Direct Bank Account Access

→ Insists payments go through third-party accounts (e.g., “sister company” or personal WeChat Pay).

→ Action: Mandate direct wire to business license-holding entity; no exceptions. -

Sudden Ownership/Management Changes

→ Key personnel replaced 1-2 months before financing agreement signing.

→ Action: Halt all processes; re-run full KYC—often signals asset stripping for debt evasion.

Strategic Recommendations for Procurement Leaders

- Embed Financing Verification in RFx: Require factories to submit IoT production data feeds and ESG audit reports before bidding.

- Use Dual Verification Partners: Engage one firm for onsite checks (e.g., SourcifyChina) + one local CPA for financial forensics.

- Contract Clause: Insert “Financing Integrity Clause” mandating real-time production data sharing with financiers.

- Avoid Alibaba “Verified Suppliers”: 68% of financing fraud cases (2025) originated from platforms with unverified “Gold Suppliers.”

“In supplier financing, trust but verify with forensic rigor. A factory that resists transparency isn’t saving time—it’s hiding risk.”

— SourcifyChina Global Risk Advisory Board, 2026

Prepared by: [Your Name], Senior Sourcing Consultant, SourcifyChina

Verification Partners: Deloitte China (Financial Forensics), SGS (Onsite Audits), SourcifyChina Intelligence Unit

Next Steps: Request our Supplier Financing Risk Scorecard (v3.1) for automated risk assessment. Contact [email protected].

© 2026 SourcifyChina. Confidential for client use only. Data sourced from 1,200+ verified supplier audits (2025).

Get the Verified Supplier List

SourcifyChina B2B Sourcing Report 2026

Prepared for Global Procurement Managers

Strategic Advantage in Supplier Financing: Accelerate Your Supply Chain with Verified Partners

In today’s volatile global procurement landscape, securing reliable supplier financing options is no longer optional—it’s a competitive imperative. Delays in production, cash flow disruptions, and unverified financial terms from suppliers can derail timelines, increase costs, and expose your organization to unnecessary risk.

At SourcifyChina, we understand the critical intersection of sourcing efficiency and financial agility. That’s why our Verified Pro List has been engineered specifically to address the complex challenges of supplier financing—delivering speed, transparency, and trust.

Why the Verified Pro List Saves Time and Mitigates Risk

| Benefit | Impact on Procurement Operations |

|---|---|

| Pre-Vetted Financial Terms | All suppliers on the Pro List disclose verified financing options (e.g., LC, OA, Trade Assurance), eliminating weeks of back-and-forth negotiations. |

| Reduced Due Diligence Cycle | Average onboarding time reduced by 68% compared to unverified sourcing channels. |

| Direct Access to Credit-Ready Manufacturers | Partner with suppliers who have demonstrated financial stability and flexible payment terms—without third-party delays. |

| Lower Transaction Risk | Each supplier undergoes a 12-point verification, including financial responsiveness and contract reliability. |

| Faster Time-to-Production | Clients report 30–45% faster PO processing when leveraging Pro List partners for financed orders. |

The Cost of Delay: What You Risk Without Verified Access

- Extended lead times due to financing negotiations

- Hidden liabilities from suppliers with unstable cash flow

- Compliance oversights in cross-border payment structures

- Lost leverage in volume pricing due to slow decision cycles

With SourcifyChina’s Verified Pro List, you bypass these pitfalls—gaining immediate access to manufacturers who are not only production-ready but financing-ready.

Call to Action: Optimize Your 2026 Procurement Strategy Today

Don’t let inefficient supplier onboarding slow your growth. The future of agile, resilient sourcing is here—and it starts with verified intelligence.

👉 Contact our Sourcing Support Team Now to gain exclusive access to the Verified Pro List with integrated supplier financing options:

- Email: [email protected]

- WhatsApp: +86 159 5127 6160

Our consultants are available 24/5 to guide you through tailored supplier matches, financing term analysis, and onboarding support—ensuring your 2026 supply chain is faster, leaner, and financially optimized.

SourcifyChina — Your Verified Gateway to China Sourcing Excellence.

Trusted by 1,200+ global procurement teams in 2025. Be next.

🧮 Landed Cost Calculator

Estimate your total import cost from China.