Introduction: Navigating the Global Market for nj manufacturers ins

Navigating the complexities of the global market for NJ manufacturers insurance can be a daunting task for international B2B buyers, especially when trying to source reliable coverage that aligns with diverse operational needs. As businesses expand across borders, understanding the nuances of insurance offerings becomes crucial to safeguarding assets and ensuring operational continuity. This comprehensive guide delves into the multifaceted world of NJ manufacturers insurance, exploring various types of coverage, their applications, and essential supplier vetting processes that can significantly impact your purchasing decisions.

In this guide, you will find detailed insights into key insurance products such as workers’ compensation, commercial auto, and property insurance tailored specifically for manufacturers. We will also address the cost implications, helping you assess the value of different policies and providers in relation to your business requirements. For international B2B buyers from regions such as Africa, South America, the Middle East, and Europe—particularly countries like Saudi Arabia and Brazil—this resource aims to empower you with the knowledge needed to make informed choices.

By providing a structured overview of the insurance landscape in New Jersey, this guide not only highlights critical considerations for policy selection but also offers actionable strategies to navigate potential challenges. Equip yourself with the tools necessary to protect your investments and foster sustainable growth in an increasingly interconnected marketplace.

Top 10 Nj Manufacturers Ins Manufacturers & Suppliers List

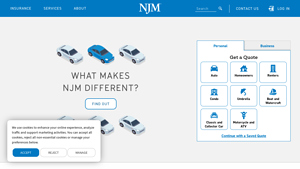

1. NJM – Comprehensive Insurance Solutions

Domain: njm.com

Registered: 1998 (27 years)

Introduction: NJM offers a range of insurance products including:

– Auto Insurance (including Classic and Collector Car, Motorcycle and ATV, Boat and Personal Watercraft)

– Home Insurance (including Homeowners, Condo, Renters, Flood, Personal Umbrella)

– Commercial Insurance (including Workers’ Compensation, Commercial Auto, ProPack Commercial Package Policy, ProEdge Businessowners Policy, Commercial Excess …

2. NJM – Workers’ Compensation and Auto Insurance

Domain: members.bcrcc.com

Registered: 2013 (12 years)

Introduction: New Jersey Manufacturers Insurance Company (NJM) is New Jersey’s largest property-casualty insurer, founded in 1913. The company specializes in workers’ compensation insurance and is a leading provider of personal and commercial auto insurance, as well as homeowners insurance. NJM operates in a mutual fashion for the exclusive benefit of its policyholders, having returned nearly $6.0 billion in di…

3. NJM – Insurance Solutions

4. NJM – Property and Casualty Insurance

5. NJM Insurance Group – Key Insurance Products

Domain: yelp.com

Registered: 2003 (22 years)

Introduction: NJM Insurance Group offers the following insurance products:

– Auto Insurance

– Homeowners Insurance

– Condo Insurance

– Renters Insurance

– Personal Umbrella Insurance

– Workers’ Compensation Insurance (for business owners)

– Commercial General Liability Insurance

– ProEdge Businessowners Policy

– Commercial Excess and Umbrella Insurance

– Commercial Auto Insurance

These services are …

6. New Jersey Manufacturers Insurance Co. – Insurance Services

Domain: bloomberg.com

Registered: 1993 (32 years)

Introduction: New Jersey Manufacturers Insurance Co. provides insurance services including commercial and personal auto insurance, workers compensation, homeowners insurance, flood insurance, and umbrella insurance.

Understanding nj manufacturers ins Types and Variations

| Type Name | Key Distinguishing Features | Primary B2B Applications | Brief Pros & Cons for Buyers |

|---|---|---|---|

| Workers’ Compensation Insurance | Covers employee injuries and illnesses on the job. | Essential for all businesses with employees. | Pros: Legal compliance, employee protection. Cons: Can be costly depending on the industry. |

| Commercial Auto Insurance | Protects vehicles used for business purposes. | Necessary for businesses with company-owned vehicles. | Pros: Coverage for accidents, liability protection. Cons: Premiums can be high based on usage. |

| Businessowners Policy (BOP) | Bundles multiple coverages including property and liability. | Ideal for small to medium-sized businesses. | Pros: Cost-effective, comprehensive coverage. Cons: May not cover all specific risks. |

| Commercial General Liability | Protects against third-party claims for bodily injury and property damage. | Critical for service-oriented businesses. | Pros: Essential for risk management. Cons: Exclusions can limit coverage. |

| Commercial Excess Liability | Provides additional coverage beyond standard liability limits. | Suitable for businesses with higher risk exposure. | Pros: Enhanced protection, peace of mind. Cons: Additional costs, may not be necessary for all. |

What Are the Key Features of Workers’ Compensation Insurance for B2B Buyers?

Workers’ Compensation Insurance is a crucial type of coverage for any business with employees. It protects employers from legal liability in the event of workplace injuries or illnesses. This insurance not only covers medical expenses and rehabilitation costs but also compensates for lost wages. B2B buyers should consider their industry’s specific risks and legal requirements when purchasing this insurance, as premiums can vary significantly based on the nature of the work and the claims history.

How Does Commercial Auto Insurance Benefit Businesses?

Commercial Auto Insurance is designed for vehicles owned or used by a business. This type of insurance provides coverage for damages resulting from accidents involving these vehicles, protecting the business from liability claims and vehicle repair costs. Companies that rely on transportation, such as delivery services or mobile businesses, should prioritize this coverage. It’s essential to evaluate the extent of coverage needed based on the number of vehicles and the nature of their use to ensure adequate protection.

What Should You Know About Businessowners Policies (BOP)?

A Businessowners Policy (BOP) is a convenient insurance solution that combines several essential coverages into one policy, typically including property, liability, and business interruption insurance. This type of policy is particularly beneficial for small to medium-sized enterprises, offering a comprehensive safety net at a lower cost than purchasing separate policies. B2B buyers should assess their specific business needs and risks to determine if a BOP is the right fit, as it may not cover all unique industry risks.

Why Is Commercial General Liability Important for Service Businesses?

Commercial General Liability insurance is fundamental for businesses that provide services to clients, as it protects against claims of bodily injury and property damage. This coverage is vital for maintaining a professional reputation and ensuring business continuity in the event of a lawsuit. B2B buyers should carefully review the policy terms, including coverage limits and exclusions, to ensure that their specific business activities are adequately protected against potential claims.

How Does Commercial Excess Liability Provide Additional Protection?

Commercial Excess Liability insurance offers an extra layer of protection by extending the limits of existing liability policies. This coverage is particularly valuable for businesses exposed to higher risks, such as those in construction or manufacturing. While it provides peace of mind by safeguarding against large claims, B2B buyers must weigh the additional costs against their risk exposure to determine if this coverage is necessary for their operations.

Key Industrial Applications of nj manufacturers ins

| Industry/Sector | Specific Application of nj manufacturers ins | Value/Benefit for the Business | Key Sourcing Considerations for this Application |

|---|---|---|---|

| Manufacturing | Workers’ Compensation Insurance | Provides financial protection for employee injuries, ensuring compliance with labor laws. | Evaluate coverage limits, industry-specific needs, and claim processing efficiency. |

| Construction | Commercial General Liability Insurance | Protects against claims of bodily injury or property damage, securing project contracts. | Assess coverage for subcontractors and project-specific risks. |

| Transportation & Logistics | Commercial Auto Insurance | Covers vehicle-related liabilities, ensuring smooth operation of logistics. | Consider fleet size, vehicle types, and international shipping regulations. |

| Retail | Businessowners Policy (BOP) | Bundles property and liability coverage, streamlining insurance management. | Review property values, inventory levels, and potential risks specific to retail. |

| Hospitality | Commercial Property Insurance | Safeguards against property loss, ensuring business continuity in hotels and restaurants. | Investigate coverage for equipment, natural disasters, and guest liabilities. |

How is Workers’ Compensation Insurance Applied in Manufacturing?

In the manufacturing sector, workers’ compensation insurance is critical for protecting businesses against claims resulting from employee injuries. This coverage ensures that injured workers receive medical benefits and wage replacement, which helps maintain morale and productivity. For international buyers, understanding the local labor laws and compliance requirements is essential. Moreover, manufacturers should evaluate the claim process efficiency and the insurer’s experience in handling industry-specific risks.

What Role Does Commercial General Liability Insurance Play in Construction?

Commercial general liability insurance is indispensable for construction companies, as it protects against claims related to bodily injury or property damage that may occur on job sites. This coverage not only helps secure contracts but also fosters trust with clients and stakeholders. International B2B buyers should consider the specific risks associated with construction projects in their regions, including subcontractor coverage and the insurance provider’s understanding of local regulations and requirements.

How Does Commercial Auto Insurance Benefit Transportation and Logistics?

For businesses in the transportation and logistics sector, commercial auto insurance is essential for covering liabilities associated with vehicle operations. This insurance protects against accidents and damages that can occur during the transportation of goods. International buyers must assess their fleet size and vehicle types, as well as any international shipping regulations that may impact coverage. Understanding the insurer’s expertise in global logistics can also provide added assurance for smoother operations.

Why is a Businessowners Policy Important for Retail?

Retail businesses benefit significantly from a Businessowners Policy (BOP), which combines property and liability coverage into a single package. This streamlining of insurance management is particularly valuable for small to medium-sized retailers looking to minimize costs while maximizing protection. International buyers should review property values and inventory levels to ensure adequate coverage. Additionally, understanding potential risks specific to retail, such as theft or customer injury, is crucial when selecting an insurance provider.

How is Commercial Property Insurance Utilized in Hospitality?

In the hospitality industry, commercial property insurance is vital for protecting hotels and restaurants against losses due to theft, fire, or natural disasters. This coverage ensures business continuity and provides peace of mind for owners and operators. For international buyers, evaluating coverage for equipment and guest liabilities is essential, as different regions may have unique risks. Additionally, understanding local regulatory requirements regarding property insurance can help businesses remain compliant and secure.

A stock image related to nj manufacturers ins.

3 Common User Pain Points for ‘nj manufacturers ins’ & Their Solutions

Scenario 1: Navigating Complex Insurance Policies for Manufacturing Operations

The Problem: Many international B2B buyers in the manufacturing sector find themselves overwhelmed by the complexities of insurance policies tailored for their industry. This confusion often stems from a lack of clarity around coverage types, exclusions, and specific terms that apply to manufacturing operations. For instance, a company in Brazil looking to expand its operations into New Jersey may struggle to understand the differences between general liability, workers’ compensation, and property insurance. This can lead to inadequate coverage, unexpected costs, and ultimately, a financial burden.

The Solution: To overcome these challenges, B2B buyers should take a proactive approach by engaging directly with insurance brokers who specialize in manufacturing insurance in New Jersey. Brokers can provide detailed explanations of policy terms and help buyers understand the specific risks associated with their operations. Additionally, buyers should conduct thorough research on the types of coverage available. A checklist can be helpful: list all potential risks, such as equipment failure or employee injuries, and match these risks with appropriate insurance products. Utilizing online resources and comparison tools can also aid in making informed decisions. Finally, regular policy reviews—ideally annually—can ensure that coverage remains relevant as business needs evolve.

Scenario 2: Managing Claims Effectively in the Manufacturing Sector

The Problem: Filing insurance claims can be particularly daunting for B2B buyers in the manufacturing industry. Delays in claim processing, disputes over coverage, and insufficient documentation can result in significant downtime and lost revenue. For example, a manufacturer from the Middle East that experiences a fire incident may find itself in a long and frustrating claims process, which not only affects its financial stability but also its reputation and operational capabilities.

The Solution: To streamline the claims process, manufacturers should maintain meticulous records of all operations, including safety protocols and incident reports. In the event of a claim, having detailed documentation can expedite the process significantly. Furthermore, establishing a clear communication channel with the insurance provider is crucial. B2B buyers should designate a claims manager within their organization who can act as the point of contact with the insurance company, ensuring that all communications are timely and comprehensive. Additionally, leveraging technology—such as insurance management software—can facilitate real-time updates and provide a structured way to track claims progress.

Scenario 3: Understanding Coverage Gaps for International Operations

The Problem: As international B2B buyers expand their manufacturing operations, they often encounter gaps in their insurance coverage that can lead to significant financial risks. For instance, a South American company that starts exporting products to Europe may not realize that its current policies do not cover international shipping risks or liability claims arising from overseas operations. This oversight can result in substantial out-of-pocket expenses in the event of an incident.

The Solution: To address these coverage gaps, B2B buyers should engage in comprehensive risk assessments that consider all operational aspects, including international logistics. Collaborating with insurance experts who specialize in international manufacturing can help identify specific risks tied to global operations. Additionally, buyers should seek out insurers that offer customizable policies allowing them to add endorsements or riders for specific needs, such as international shipping coverage or product liability for exports. Regular training sessions for staff on the importance of insurance and the specifics of the coverage can also empower teams to recognize and report potential risks, ensuring that the business is adequately protected as it grows internationally.

Strategic Material Selection Guide for nj manufacturers ins

What Are the Key Properties of Common Materials Used by NJ Manufacturers?

When selecting materials for manufacturing processes, understanding their properties is crucial. Here, we analyze four common materials used by New Jersey manufacturers, focusing on their performance, advantages, disadvantages, and considerations for international B2B buyers.

1. Steel

Key Properties: Steel is known for its high tensile strength, durability, and resistance to deformation under stress. It can withstand high temperatures and pressures, making it suitable for a variety of applications.

Pros & Cons: The primary advantage of steel is its strength and versatility, allowing it to be used in construction, automotive, and machinery. However, it is susceptible to corrosion unless treated, which can lead to increased maintenance costs. Additionally, the manufacturing process can be complex, requiring specialized equipment.

Impact on Application: Steel is compatible with various media, including water and oil, but its corrosion resistance must be considered in harsh environments. This is particularly relevant for applications in humid or chemically aggressive settings.

Considerations for International Buyers: Compliance with international standards such as ASTM and DIN is essential for steel products. Buyers from regions like Africa and the Middle East should also consider local sourcing options to mitigate import costs.

2. Aluminum

Key Properties: Aluminum is lightweight, corrosion-resistant, and has excellent thermal and electrical conductivity. It can be easily fabricated and is available in various alloys.

Pros & Cons: The lightweight nature of aluminum makes it ideal for applications where reducing weight is critical, such as in aerospace and automotive industries. However, it is generally more expensive than steel and may not offer the same strength, leading to potential limitations in load-bearing applications.

Impact on Application: Aluminum is compatible with a wide range of media, including water and chemicals, making it suitable for diverse applications. Its corrosion resistance is particularly beneficial in coastal or humid environments.

Considerations for International Buyers: Buyers should ensure that the aluminum meets relevant standards like JIS and EN, especially when importing to regions with strict regulations, such as Europe.

3. Polypropylene

Key Properties: Polypropylene is a thermoplastic polymer known for its chemical resistance, lightweight, and flexibility. It can withstand temperatures up to 100°C (212°F) and is often used in applications requiring a balance of strength and flexibility.

Pros & Cons: The primary advantage of polypropylene is its excellent chemical resistance, making it suitable for containers and piping systems. However, it has lower tensile strength compared to metals and may not perform well under extreme temperatures.

Impact on Application: Polypropylene is compatible with a wide range of chemicals, including acids and bases, making it ideal for chemical processing industries. Its lightweight nature also reduces transportation costs.

Considerations for International Buyers: Compliance with international safety and quality standards is crucial. Buyers should verify that the polypropylene meets ASTM specifications, particularly for applications in the food and pharmaceutical industries.

4. Glass Fiber Reinforced Plastic (GFRP)

Key Properties: GFRP combines the lightweight characteristics of plastics with the strength of glass fibers, providing excellent tensile strength and corrosion resistance. It can withstand a variety of environmental conditions.

Pros & Cons: GFRP is highly durable and resistant to corrosion, making it suitable for outdoor applications. However, it can be more expensive than traditional materials and may require specialized manufacturing processes.

Impact on Application: GFRP is compatible with various media, including water and chemicals, making it ideal for applications in marine and chemical industries. Its lightweight nature also facilitates easier handling and installation.

Considerations for International Buyers: Buyers should ensure that GFRP products comply with international standards, as well as local regulations in their respective regions, to avoid legal complications.

Summary Table of Material Selection

| Material | Typical Use Case for nj manufacturers ins | Key Advantage | Key Disadvantage/Limitation | Relative Cost (Low/Med/High) |

|---|---|---|---|---|

| Steel | Construction, automotive, machinery | High strength and versatility | Susceptible to corrosion | Medium |

| Aluminum | Aerospace, automotive | Lightweight and corrosion-resistant | More expensive than steel | High |

| Polypropylene | Chemical containers, piping systems | Excellent chemical resistance | Lower tensile strength than metals | Medium |

| Glass Fiber Reinforced Plastic (GFRP) | Marine applications, chemical industries | Highly durable and corrosion-resistant | Higher cost and specialized manufacturing | High |

This strategic material selection guide provides insights into the properties and considerations of various materials that NJ manufacturers utilize. Understanding these factors will help international B2B buyers make informed decisions tailored to their specific needs and regional compliance requirements.

A stock image related to nj manufacturers ins.

In-depth Look: Manufacturing Processes and Quality Assurance for nj manufacturers ins

What Are the Main Stages of Manufacturing Processes for NJ Manufacturers?

New Jersey manufacturers employ a comprehensive manufacturing process that typically includes several key stages: material preparation, forming, assembly, and finishing. Understanding these stages is crucial for international B2B buyers looking to ensure quality and reliability in their supply chains.

How Do Material Preparation and Forming Impact Product Quality?

The first stage, material preparation, involves sourcing and preparing raw materials according to specific project requirements. This may include cutting, shaping, or treating materials to enhance their properties. Techniques such as laser cutting, CNC machining, and chemical treatments are common in this phase.

In the forming stage, manufacturers utilize various methods to shape materials into desired forms. Common techniques include:

- Molding: Used for plastics and metals, where materials are poured into molds to achieve specific shapes.

- Casting: Involves pouring liquid material into a mold to create complex shapes, often used in metal manufacturing.

- Forging: A process where metal is shaped by applying compressive forces, enhancing its strength.

These processes are pivotal in determining the final product’s integrity and performance, making it essential for buyers to assess the manufacturers’ capabilities and expertise in these areas.

What Are the Key Steps in Assembly and Finishing Processes?

Following forming, the assembly stage integrates various components into a complete product. This may involve manual assembly or automated processes, depending on the complexity of the product and the manufacturer’s capabilities. Techniques such as robotic assembly and automated screw driving are increasingly popular, enhancing efficiency and precision.

The finishing stage includes surface treatments and quality enhancements such as painting, coating, or polishing. These processes not only improve aesthetics but also protect against corrosion and wear. Buyers should inquire about the finishing techniques employed, as they can significantly impact product durability and performance.

What International Standards Should B2B Buyers Consider for Quality Assurance?

Quality assurance in manufacturing is critical, particularly for international B2B buyers who require reliable and consistent products. Many NJ manufacturers adhere to international standards, such as ISO 9001, which outlines a framework for quality management systems. Compliance with these standards indicates a commitment to quality and continuous improvement.

In addition to ISO standards, industry-specific certifications such as CE (Conformité Européenne) for European markets and API (American Petroleum Institute) for oil and gas sectors are also important. These certifications ensure that products meet rigorous safety and performance criteria, which can be particularly relevant for buyers in sectors with strict regulatory requirements.

How Are Quality Control Checkpoints Implemented in Manufacturing?

Quality Control (QC) is integral to the manufacturing process, involving multiple checkpoints to ensure products meet specified standards. Key QC phases include:

-

Incoming Quality Control (IQC): This stage involves inspecting raw materials before they enter the production process. It ensures that all materials meet required specifications and helps prevent defects later in the manufacturing process.

-

In-Process Quality Control (IPQC): Continuous monitoring during the manufacturing process is crucial. This may include real-time inspections and tests to identify defects as they occur, allowing for immediate corrective actions.

-

Final Quality Control (FQC): Before products leave the facility, they undergo rigorous testing to ensure they meet quality standards. This may involve functional testing, performance evaluation, and final inspections.

What Common Testing Methods Are Utilized in Quality Control?

Manufacturers employ various testing methods to ensure product quality and compliance with standards. Common methods include:

-

Destructive Testing: This involves testing the product to failure to determine its limits and performance characteristics. Techniques include tensile testing and impact testing.

-

Non-Destructive Testing (NDT): Methods such as ultrasonic, radiographic, and magnetic particle testing allow manufacturers to evaluate materials and components without causing damage.

-

Functional Testing: This assesses the performance of the product under operational conditions, ensuring that it meets design specifications.

B2B buyers should request detailed reports on these testing methods from manufacturers to verify their adherence to quality standards.

How Can B2B Buyers Verify Supplier Quality Control Practices?

For international buyers, verifying a supplier’s quality control practices is paramount. Here are several strategies to ensure quality assurance:

-

Conduct Audits: Regularly scheduled audits can provide insights into a manufacturer’s processes, adherence to standards, and overall quality culture. Buyers can either perform these audits themselves or hire third-party firms specializing in quality assessments.

-

Request Quality Reports: Manufacturers should provide comprehensive quality reports that detail their processes, testing methods, and outcomes. These documents can help buyers understand the level of quality assurance in place.

-

Engage in Third-Party Inspections: Utilizing third-party inspection services can offer an unbiased evaluation of the manufacturer’s quality control processes. This is particularly important for buyers in regions with strict regulatory requirements.

-

Check Certifications and Accreditations: Buyers should verify that manufacturers hold the necessary certifications and accreditations relevant to their industry. This can serve as a baseline assurance of quality practices.

What Are the Unique Quality Control Considerations for International Buyers?

International B2B buyers, particularly from regions such as Africa, South America, the Middle East, and Europe, should be aware of specific quality control nuances. These may include:

-

Cultural Differences in Quality Standards: Different regions may have varying expectations regarding quality. Understanding these differences can help buyers establish clear quality benchmarks with suppliers.

-

Import Regulations and Compliance: Familiarity with local regulations and compliance requirements is crucial. Buyers should ensure that their suppliers are knowledgeable about and compliant with these regulations to avoid delays or penalties.

-

Logistics and Supply Chain Considerations: Quality control does not end at the factory; logistics can impact product quality during transportation. Buyers should collaborate with suppliers to implement quality assurance measures throughout the supply chain.

By understanding the manufacturing processes and quality assurance practices of NJ manufacturers, B2B buyers can make informed decisions that ensure product quality, compliance, and reliability. This knowledge fosters stronger supplier relationships and supports successful international trade.

Practical Sourcing Guide: A Step-by-Step Checklist for ‘nj manufacturers ins’

The following guide serves as a comprehensive checklist for international B2B buyers seeking to procure insurance services from New Jersey manufacturers. This step-by-step approach will help ensure that you make informed decisions while sourcing the right insurance solutions for your business needs.

Step 1: Identify Your Insurance Requirements

Understanding your specific insurance needs is crucial before engaging with potential suppliers. Consider the types of coverage you require, such as workers’ compensation, commercial auto, or general liability. Take into account your business operations, industry regulations, and any unique risks associated with your activities.

Step 2: Research Potential Insurance Providers

Conduct thorough research on insurance companies that operate in New Jersey, focusing on their history, reputation, and customer reviews. Look for providers like New Jersey Manufacturers Insurance Company, known for its strong financial stability and customer service. Utilize resources like the Better Business Bureau (BBB) to gauge the company’s reliability and responsiveness to client concerns.

Step 3: Evaluate Coverage Options and Policies

Once you have shortlisted potential providers, review the specific coverage options they offer. Ensure that their policies align with your business needs and compliance requirements. Pay attention to:

– Policy Limits: Understand the maximum coverage amounts.

– Exclusions: Identify any coverage gaps that may affect your business.

Step 4: Request Quotes and Compare Costs

Contact the selected insurance companies to request detailed quotes based on your identified needs. Comparing quotes from multiple insurers will provide insight into pricing structures and available discounts. Look for:

– Total Cost: Consider both premiums and deductibles.

– Discounts Available: Inquire about multi-policy or loyalty discounts that can reduce overall costs.

Step 5: Assess Customer Service and Claims Process

An essential factor in choosing an insurance provider is their customer service and claims handling process. Evaluate their responsiveness and the ease of filing a claim. A company like NJM is recognized for high customer satisfaction, which can be critical during stressful claim situations. Ensure you understand:

– Claims Process: How claims are filed and the average processing time.

– Support Availability: Availability of customer service representatives, especially for international clients.

Step 6: Check Financial Stability and Ratings

Before finalizing your decision, verify the financial stability of the insurance providers. Look for ratings from reputable agencies like A.M. Best or Moody’s, which evaluate the insurer’s ability to pay claims. A solid financial rating indicates reliability and gives you confidence in their long-term viability.

Step 7: Review the Contract Thoroughly

Finally, before signing any agreement, review the insurance contract carefully. Ensure that all terms, conditions, and coverage details are clearly defined and match what was discussed. Seek clarification on any ambiguous terms and consider consulting with a legal advisor to ensure that your interests are protected.

By following these steps, B2B buyers can effectively navigate the process of sourcing insurance from New Jersey manufacturers, ensuring that they select the most suitable provider for their business needs.

Comprehensive Cost and Pricing Analysis for nj manufacturers ins Sourcing

What Are the Key Cost Components for Sourcing from NJ Manufacturers?

When sourcing from New Jersey manufacturers, understanding the cost structure is crucial for international buyers. The main cost components include:

-

Materials: The quality and type of raw materials significantly influence pricing. Specialty materials or those with certifications can increase costs.

-

Labor: Labor costs in New Jersey are typically higher than in many other regions, driven by state-specific wage regulations and benefits. This is particularly important for labor-intensive manufacturing processes.

-

Manufacturing Overhead: This includes utilities, rent, and other indirect costs associated with production. NJ manufacturers often have well-maintained facilities, which can lead to higher overhead costs but also better product quality.

-

Tooling: Custom tooling can be a significant upfront investment, especially for specialized products. Understanding the tooling costs is essential for accurate pricing.

-

Quality Control (QC): Rigorous quality control processes can add to the cost but are crucial for ensuring product reliability, especially for international buyers who may have stringent quality requirements.

-

Logistics: Shipping costs, including freight and insurance, can vary based on the destination and shipping method. Buyers should factor in these costs to determine the total landed cost.

-

Margin: Manufacturers typically add a profit margin on top of their costs, which can vary based on market demand and competitive factors.

How Do Price Influencers Affect Sourcing Decisions for International Buyers?

Several factors can influence pricing when sourcing from NJ manufacturers:

-

Volume and Minimum Order Quantities (MOQ): Larger orders typically lead to lower per-unit prices due to economies of scale. International buyers should negotiate MOQs to optimize costs.

-

Specifications and Customization: Custom products may incur additional design and manufacturing costs. Clearly defining specifications can help mitigate unexpected expenses.

-

Material Quality and Certifications: Higher quality materials and necessary certifications (e.g., ISO) can increase costs but may be essential for compliance in certain markets.

-

Supplier Factors: The reputation and reliability of the manufacturer play a significant role in pricing. Established manufacturers may charge a premium for their proven track record.

-

Incoterms: Understanding the terms of shipment (e.g., FOB, CIF) is critical. These terms define who bears the cost and risk at various points in the shipping process, impacting overall expenses.

What Buyer Tips Can Help Optimize Costs in Sourcing?

International B2B buyers, particularly from regions like Africa, South America, the Middle East, and Europe, can employ several strategies to optimize costs:

-

Negotiation: Engaging in robust negotiations can lead to better pricing and terms. Having a clear understanding of the cost components allows buyers to make informed arguments during discussions.

-

Cost-Efficiency Analysis: Buyers should conduct a thorough analysis of the total cost of ownership (TCO), which includes not only the purchase price but also logistics, maintenance, and potential tariffs.

-

Pricing Nuances for International Buyers: Be aware of additional costs such as import duties, taxes, and customs fees that can significantly affect the final price.

-

Establish Long-Term Relationships: Building strong relationships with suppliers can lead to better pricing and terms over time. Loyalty often results in better service and pricing flexibility.

Conclusion: Understanding the Cost Structure and Pricing Influencers

When engaging with NJ manufacturers, international buyers must navigate a complex landscape of cost components and pricing influencers. By leveraging strategic negotiation tactics, understanding the intricacies of pricing, and conducting thorough cost analyses, buyers can optimize their sourcing strategies and achieve greater value in their procurement processes.

Disclaimer: Prices and cost structures mentioned are indicative and can vary based on specific circumstances and market conditions. Always consult with manufacturers directly for accurate pricing and terms tailored to your needs.

Alternatives Analysis: Comparing nj manufacturers ins With Other Solutions

Understanding Alternatives to NJ Manufacturers Insurance

In the dynamic landscape of insurance solutions, B2B buyers often seek viable alternatives to meet their unique operational needs. This section explores how NJ Manufacturers Insurance (NJM) stacks up against other insurance solutions tailored for businesses. By understanding different options, international buyers from regions like Africa, South America, the Middle East, and Europe can make informed decisions that align with their strategic goals.

| Comparison Aspect | Nj Manufacturers Ins | Alternative 1: AIG Business Insurance | Alternative 2: Allianz Global Corporate & Specialty |

|---|---|---|---|

| Performance | High customer satisfaction and robust claims support | Strong global presence with tailored coverage | Comprehensive risk management solutions for large enterprises |

| Cost | Competitive pricing with potential dividends | Higher premiums for extensive coverage options | Variable pricing based on global risk assessment |

| Ease of Implementation | Streamlined onboarding with dedicated agents | More complex due to international operations | Requires in-depth risk analysis before policy setup |

| Maintenance | User-friendly online portal for policy management | Needs ongoing communication with brokers | Regular audits and updates required for compliance |

| Best Use Case | Small to medium businesses in the U.S. | Multinational corporations needing specialized coverage | Large enterprises with complex global operations |

What Are the Pros and Cons of AIG Business Insurance?

AIG Business Insurance offers a robust suite of products designed for various industries. Pros include its strong global presence and ability to tailor coverage according to specific business needs, making it suitable for multinational operations. However, the cons include generally higher premiums compared to NJM and a more complex implementation process that may require extensive engagement with brokers to ensure proper coverage.

How Does Allianz Global Corporate & Specialty Compare?

Allianz Global Corporate & Specialty provides comprehensive risk management solutions, particularly for large enterprises. The advantages of Allianz include its extensive global reach and a focus on complex risk scenarios, which can be invaluable for businesses with international operations. On the downside, the disadvantages lie in the variable pricing structure that can lead to higher costs and the need for a thorough risk assessment before policy initiation, which may not be ideal for smaller firms or startups.

Conclusion: How to Choose the Right Insurance Solution for Your Business

Selecting the right insurance solution hinges on understanding your business’s specific requirements and operational context. For small to medium enterprises primarily operating in the U.S., NJ Manufacturers Insurance may provide the best balance of cost, performance, and ease of use. Conversely, if your business operates on a global scale or requires specialized coverage for intricate risks, AIG or Allianz might be more suitable despite their complexities and higher costs. B2B buyers should conduct a thorough assessment of their needs, budget, and operational scope to choose the most fitting solution.

Essential Technical Properties and Trade Terminology for nj manufacturers ins

What Are the Key Technical Properties Relevant to NJ Manufacturers Insurance?

When dealing with NJ manufacturers insurance, understanding specific technical properties is essential for B2B buyers. Here are some critical specifications that influence insurance policies and coverage options:

-

Coverage Limits

Coverage limits define the maximum amount an insurer will pay for a covered loss. In the context of manufacturing, having adequate coverage limits ensures that businesses can recover from significant losses due to equipment failure, natural disasters, or liability claims. Buyers should assess their operational risks and select coverage limits that align with potential financial impacts. -

Deductibles

A deductible is the amount a policyholder must pay out-of-pocket before the insurance coverage kicks in. Lower deductibles typically result in higher premiums, while higher deductibles can decrease premium costs but increase financial exposure during a claim. Understanding the balance between deductible levels and premium costs is crucial for manufacturers to manage cash flow and risk effectively. -

Policy Exclusions

Policy exclusions are specific conditions or circumstances that are not covered by the insurance. For manufacturers, common exclusions may involve certain types of machinery breakdowns or natural disasters. Being aware of exclusions allows businesses to take necessary precautions and possibly seek additional coverage where gaps exist. -

Claims Process Efficiency

The efficiency of the claims process can significantly affect a manufacturer’s operations after a loss. A streamlined claims process ensures quick recovery and minimizes downtime. Understanding the insurer’s claims response time and procedures can aid manufacturers in selecting an insurer that prioritizes customer service and swift resolutions. -

Risk Assessment Protocols

Insurers often conduct risk assessments to evaluate the potential hazards associated with a manufacturer’s operations. These protocols include evaluating workplace safety, equipment maintenance, and compliance with industry regulations. A thorough risk assessment can help in tailoring insurance solutions that address specific operational risks effectively.

What Are Common Trade Terms in NJ Manufacturers Insurance?

Navigating the insurance landscape requires familiarity with specific industry jargon. Here are several common terms that B2B buyers should understand:

-

OEM (Original Equipment Manufacturer)

OEM refers to companies that produce parts and equipment that may be marketed by another manufacturer. In insurance, knowing the OEM status of machinery can influence coverage terms and risk assessments, as original parts often have different warranty and liability implications compared to aftermarket components. -

MOQ (Minimum Order Quantity)

MOQ is the smallest quantity of a product that a supplier is willing to sell. For manufacturers, understanding MOQs is critical when sourcing materials or components, as it can impact inventory costs and cash flow management. Insurance policies may also consider inventory levels when assessing risk. -

RFQ (Request for Quotation)

An RFQ is a document sent to suppliers requesting pricing and terms for specific products or services. In the context of insurance, an RFQ can be used when manufacturers are seeking quotes from multiple insurers, allowing them to compare coverage options and pricing effectively. -

Incoterms (International Commercial Terms)

Incoterms are a set of international trade rules that define the responsibilities of buyers and sellers regarding shipping, insurance, and tariffs. Familiarity with Incoterms is essential for manufacturers engaged in international trade, as they determine liability and insurance responsibilities during transit. -

BOP (Businessowners Policy)

A BOP is a package insurance policy designed for small to medium-sized businesses, combining various coverage types such as property, liability, and business interruption. For manufacturers, a BOP can provide comprehensive protection tailored to their operational needs, often at a lower cost than purchasing separate policies. -

Workers’ Compensation Insurance

This insurance covers medical costs and lost wages for employees injured on the job. For manufacturers, having robust workers’ compensation coverage is vital, as it not only protects employees but also helps the company comply with legal requirements and manage potential liability risks.

Understanding these properties and terms is crucial for international B2B buyers looking to navigate the complexities of NJ manufacturers insurance effectively. By equipping themselves with this knowledge, manufacturers can make informed decisions that protect their businesses and enhance their operational resilience.

Navigating Market Dynamics and Sourcing Trends in the nj manufacturers ins Sector

What Are the Current Market Dynamics and Key Trends in the NJ Manufacturers Insurance Sector?

The New Jersey Manufacturers Insurance (NJM) sector is witnessing significant shifts influenced by global drivers such as technological advancements, regulatory changes, and evolving customer expectations. For international B2B buyers, particularly from regions like Africa, South America, the Middle East, and Europe, understanding these dynamics is essential for making informed sourcing decisions.

A key trend is the integration of technology in insurance processes, such as the use of Artificial Intelligence (AI) and machine learning for underwriting and claims processing. These technologies enhance efficiency and reduce operational costs, making insurance products more accessible and tailored to diverse business needs. Additionally, the rise of digital platforms allows for seamless interactions and transactions, which are particularly appealing to international buyers seeking reliability and speed in service delivery.

Emerging markets are increasingly focused on risk management and compliance, driven by stricter regulations and a growing awareness of the importance of corporate governance. This trend highlights the necessity for manufacturers in New Jersey to align their offerings with global standards, ensuring that international buyers can trust their insurance providers to meet regulatory requirements. Furthermore, the ongoing focus on customer experience is reshaping the competitive landscape, with firms like NJM emphasizing transparency and responsive service as core differentiators.

How Important Is Sustainability and Ethical Sourcing in the NJ Manufacturers Insurance Sector?

Sustainability and ethical sourcing have become critical considerations for B2B buyers globally, and the NJ manufacturers insurance sector is no exception. Environmental impacts associated with insurance processes, such as paper use and energy consumption, are under scrutiny. Consequently, many companies are adopting ‘green’ practices, implementing digital solutions to minimize their carbon footprint and enhance operational efficiency.

For international buyers, partnering with insurers that prioritize sustainability can enhance their brand reputation and appeal to environmentally-conscious consumers. Certifications such as ISO 14001, which focuses on effective environmental management systems, can serve as indicators of a company’s commitment to sustainable practices. Furthermore, using eco-friendly materials in policy documentation and communications can also align with buyers’ sustainability goals.

Ethical supply chains are equally essential, as buyers increasingly demand transparency in how services are delivered. Insurers that demonstrate a commitment to fair labor practices and community engagement are more likely to attract international clients. By fostering relationships with suppliers and partners that share these values, NJ manufacturers can enhance their market positioning and create a competitive edge in the global marketplace.

What Is the Evolution and History of the NJ Manufacturers Insurance Sector?

The NJ manufacturers insurance sector has evolved significantly since its inception in the early 20th century. Founded in 1913, NJM has built its reputation on a mutual business model that prioritizes the interests of policyholders. This approach has enabled the company to return nearly $6 billion in dividends to its customers, establishing a strong foundation of trust and reliability.

Historically, NJM emerged as a key player in the workers’ compensation insurance market, responding to the needs of a rapidly industrializing region. Over the decades, the company expanded its offerings to include a wide range of personal and commercial insurance products. As the market dynamics shifted, NJM adapted by embracing technological advancements and enhancing customer service, thereby solidifying its position as New Jersey’s largest property-casualty insurer.

Today, NJM’s commitment to innovation and customer satisfaction continues to drive its growth, making it an attractive partner for international B2B buyers looking for reliable insurance solutions.

Frequently Asked Questions (FAQs) for B2B Buyers of nj manufacturers ins

-

How can I ensure I choose the right insurance provider for my manufacturing business in New Jersey?

To select the right insurance provider, research their reputation, financial stability, and customer service history. Look for reviews and ratings from other businesses in your industry. It’s also beneficial to consult with local business associations or industry groups for recommendations. Make sure the insurer offers coverage that aligns with your specific needs, such as workers’ compensation, commercial auto, and general liability insurance. Additionally, consider their claims process and how they handle customer support during emergencies. -

What types of insurance coverage should I consider for my manufacturing operations?

Manufacturers should consider several types of insurance coverage, including general liability, property insurance, workers’ compensation, and commercial auto insurance. Depending on your operations, you might also need specialized coverage such as product liability, equipment breakdown, or environmental liability insurance. An insurance agent experienced in the manufacturing sector can help you assess your risks and tailor a policy that meets your unique needs. -

How do minimum order quantities (MOQ) affect insurance coverage?

Minimum order quantities (MOQ) can influence your insurance needs, particularly regarding product liability and inventory coverage. If your MOQ is high, you may require more comprehensive coverage to protect against potential losses from unsold inventory or product recalls. It’s essential to discuss your MOQ with your insurance provider to ensure that your policy adequately covers your inventory levels and associated risks. -

What payment terms are typically offered by insurance providers for manufacturers?

Payment terms can vary widely among insurance providers. Many offer flexible options, including monthly, quarterly, or annual payment plans. Some may provide discounts for paying the full premium upfront. It’s important to review the payment structure and any associated fees, as well as inquire about potential discounts for bundling multiple policies or having a claims-free history. -

How can I vet insurance providers when sourcing from New Jersey manufacturers?

Vetting insurance providers involves checking their financial ratings, customer reviews, and claims handling history. Look for providers with strong ratings from agencies like A.M. Best or Standard & Poor’s. Engage in conversations with their representatives to gauge their responsiveness and expertise. Additionally, consider seeking testimonials from other businesses in your network that have experience with the provider. -

What logistics considerations should I keep in mind when dealing with insurance for international trade?

When engaging in international trade, it’s crucial to understand the logistics of shipping, customs regulations, and insurance coverage for goods in transit. Ensure that your insurance policy includes coverage for international shipping and loss during transit. Familiarize yourself with Incoterms to clarify responsibilities for insurance during shipping. Consulting with a logistics expert can help you navigate these complexities and ensure compliance with international regulations. -

How can I customize my insurance policy to fit my specific manufacturing needs?

Customizing your insurance policy involves working closely with your insurance agent to identify your unique risks and coverage requirements. Discuss your specific manufacturing processes, equipment, and workforce to tailor your policy. Many insurers offer add-ons or endorsements that can enhance your coverage, such as cyber liability or equipment breakdown. Regularly review your policy to ensure it evolves with your business needs. -

What quality assurance measures should I implement to reduce insurance premiums?

Implementing robust quality assurance (QA) measures can lower your insurance premiums by minimizing risks associated with claims. Establish strict quality control processes, regular employee training, and thorough documentation of compliance with safety regulations. Insurers often provide discounts for businesses that demonstrate a commitment to safety and risk management. Regularly reviewing and updating these measures can also help maintain lower premiums over time.

Important Disclaimer & Terms of Use

⚠️ Important Disclaimer

The information provided in this guide, including content regarding manufacturers, technical specifications, and market analysis, is for informational and educational purposes only. It does not constitute professional procurement advice, financial advice, or legal advice.

While we have made every effort to ensure the accuracy and timeliness of the information, we are not responsible for any errors, omissions, or outdated information. Market conditions, company details, and technical standards are subject to change.

B2B buyers must conduct their own independent and thorough due diligence before making any purchasing decisions. This includes contacting suppliers directly, verifying certifications, requesting samples, and seeking professional consultation. The risk of relying on any information in this guide is borne solely by the reader.

Strategic Sourcing Conclusion and Outlook for nj manufacturers ins

As the landscape of manufacturing continues to evolve, New Jersey manufacturers insurance (NJM) offers a vital opportunity for international B2B buyers to strategically source reliable and comprehensive insurance solutions. The key takeaways from this guide highlight the importance of understanding the unique offerings of NJM, particularly in areas such as workers’ compensation, commercial auto, and liability insurance. By leveraging the financial stability and customer satisfaction that NJM is known for, businesses can mitigate risks and enhance their operational efficiency.

Strategic sourcing in this context not only ensures protection against unforeseen events but also fosters long-term partnerships that can adapt to the changing needs of global markets. For buyers from regions like Africa, South America, the Middle East, and Europe, NJM presents a competitive advantage, offering tailored solutions that align with diverse regulatory environments and business practices.

Looking ahead, the collaboration between NJ manufacturers and international buyers is poised to create a robust network of support and innovation. We encourage you to explore these insurance solutions further, as investing in the right coverage can significantly bolster your business’s resilience and growth trajectory in the global marketplace.