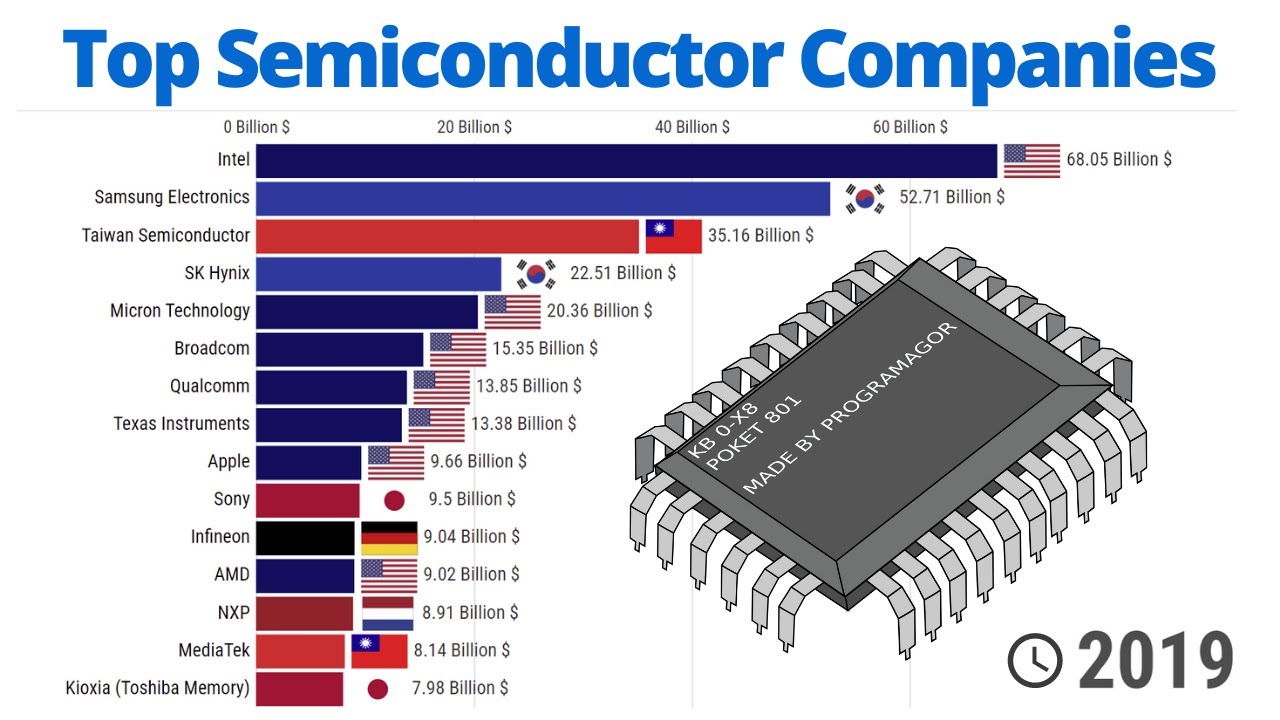

The global semiconductor market continues to experience robust growth, driven by increasing demand across industries such as consumer electronics, automotive, telecommunications, and industrial automation. According to a 2023 report by Mordor Intelligence, the semiconductor market was valued at USD 574 billion in 2022 and is projected to reach USD 1.3 trillion by 2028, growing at a CAGR of approximately 14.3% during the forecast period. This expansion is fueled by advancements in AI, 5G deployment, and rising adoption of IoT devices. As innovation accelerates and supply chain dynamics evolve, a select group of manufacturers are leading the charge in capacity, technology, and market share. Based on revenue, R&D investment, and production scale, the following nine companies represent the top semiconductor manufacturers shaping the future of the industry.

Top 9 Top Semiconductor Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Top Semiconductor

As of now, in H2 (the second half) of 2024, specific market data and projections for the year 2026 are forward-looking and based on current industry trends, analyst forecasts, and macroeconomic indicators. While actual 2026 performance cannot yet be known, we can analyze likely market trends for top semiconductor companies—such as NVIDIA, Intel, AMD, TSMC, Samsung Electronics, Broadcom, and others—based on ongoing technological developments, geopolitical dynamics, and demand drivers that are expected to shape the sector through 2026.

Here is an analysis of projected 2026 market trends for the top semiconductor companies, using H2 2024 insights as a foundation:

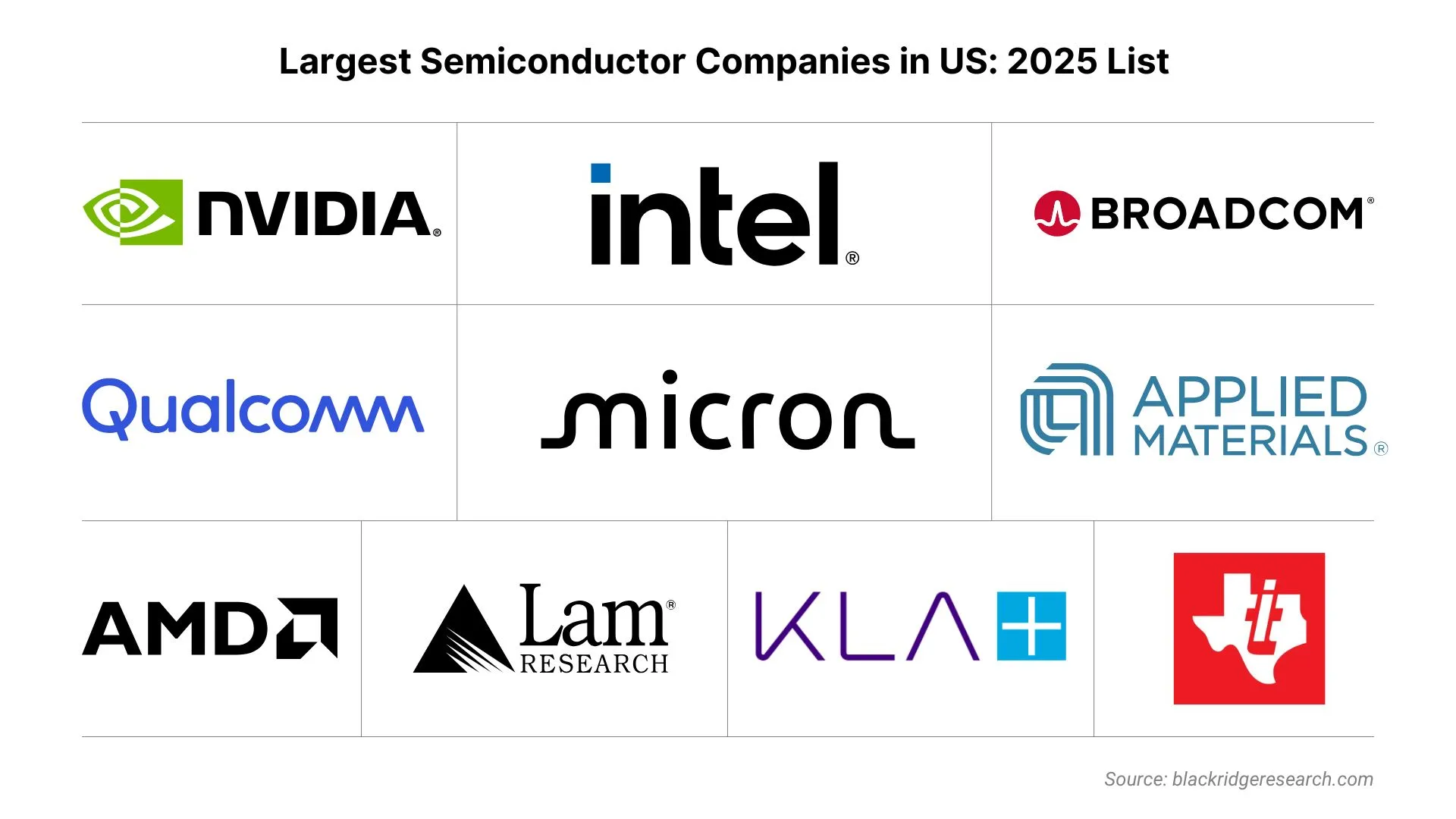

1. AI and High-Performance Computing (HPC) to Drive Growth

– Key Players: NVIDIA, AMD, Intel, Broadcom

– Trend: The explosive demand for AI accelerators—especially GPUs and custom AI chips—will continue to be the primary growth engine in 2026.

– Analysis: NVIDIA remains dominant in data center GPUs (e.g., H100, B200, Blackwell architecture). By 2026, competition will intensify as AMD (MI300X and beyond) and Intel (Gaudi 3 and future Ponte Vecchio derivatives) gain traction. Cloud hyperscalers (e.g., Google, Microsoft, Amazon) are expected to increase custom chip development, boosting demand for IP from Arm and design tools from Synopsys and Cadence.

– Outlook: The AI chip market could grow at a CAGR of 30–35% through 2026, with data center semiconductors representing over 40% of revenue growth.

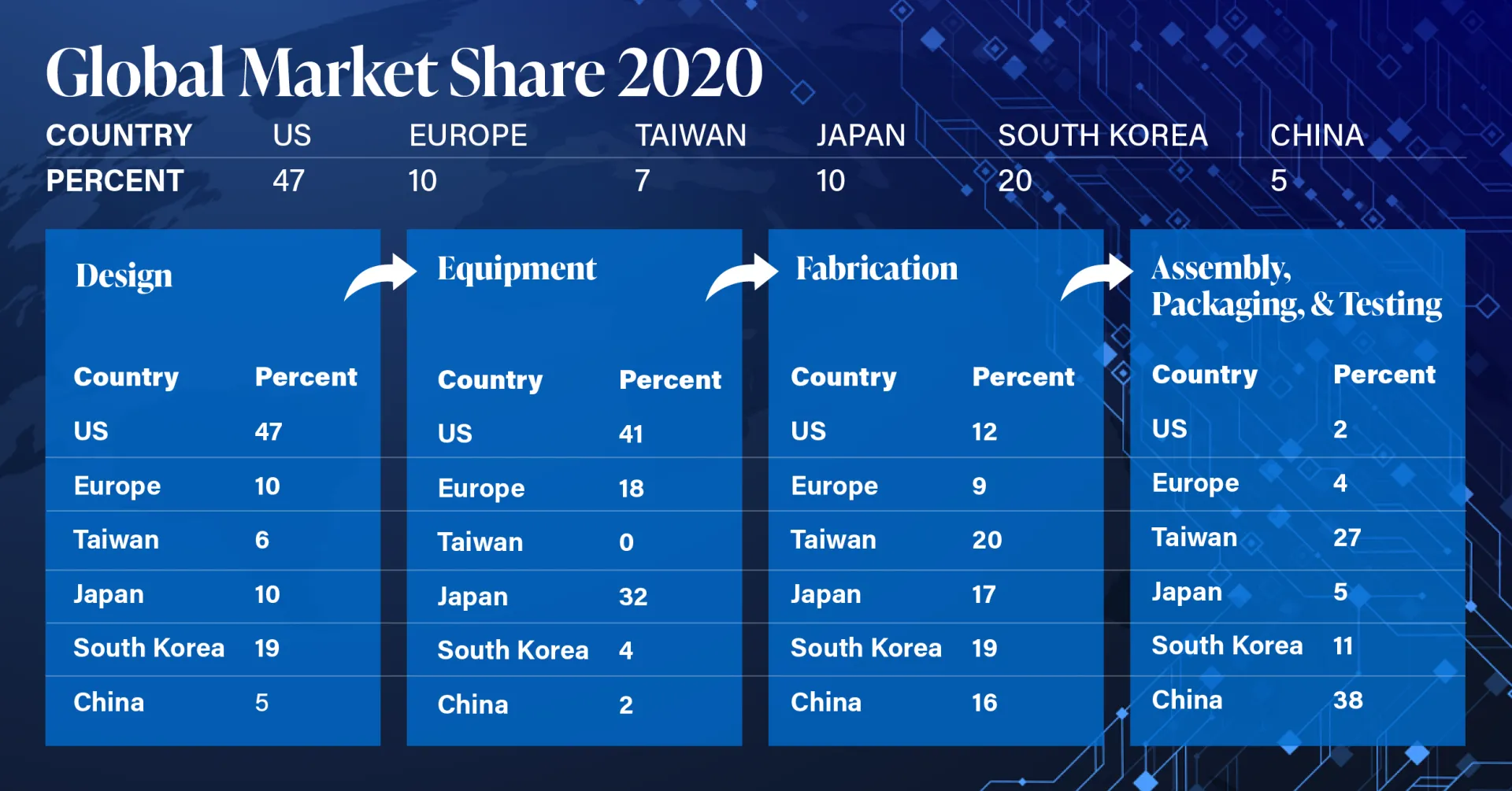

2. Geopolitical Fragmentation and Supply Chain Resilience

– Key Players: TSMC, Samsung, Intel, SMIC

– Trend: U.S.-China tech decoupling will continue to influence manufacturing and R&D strategies.

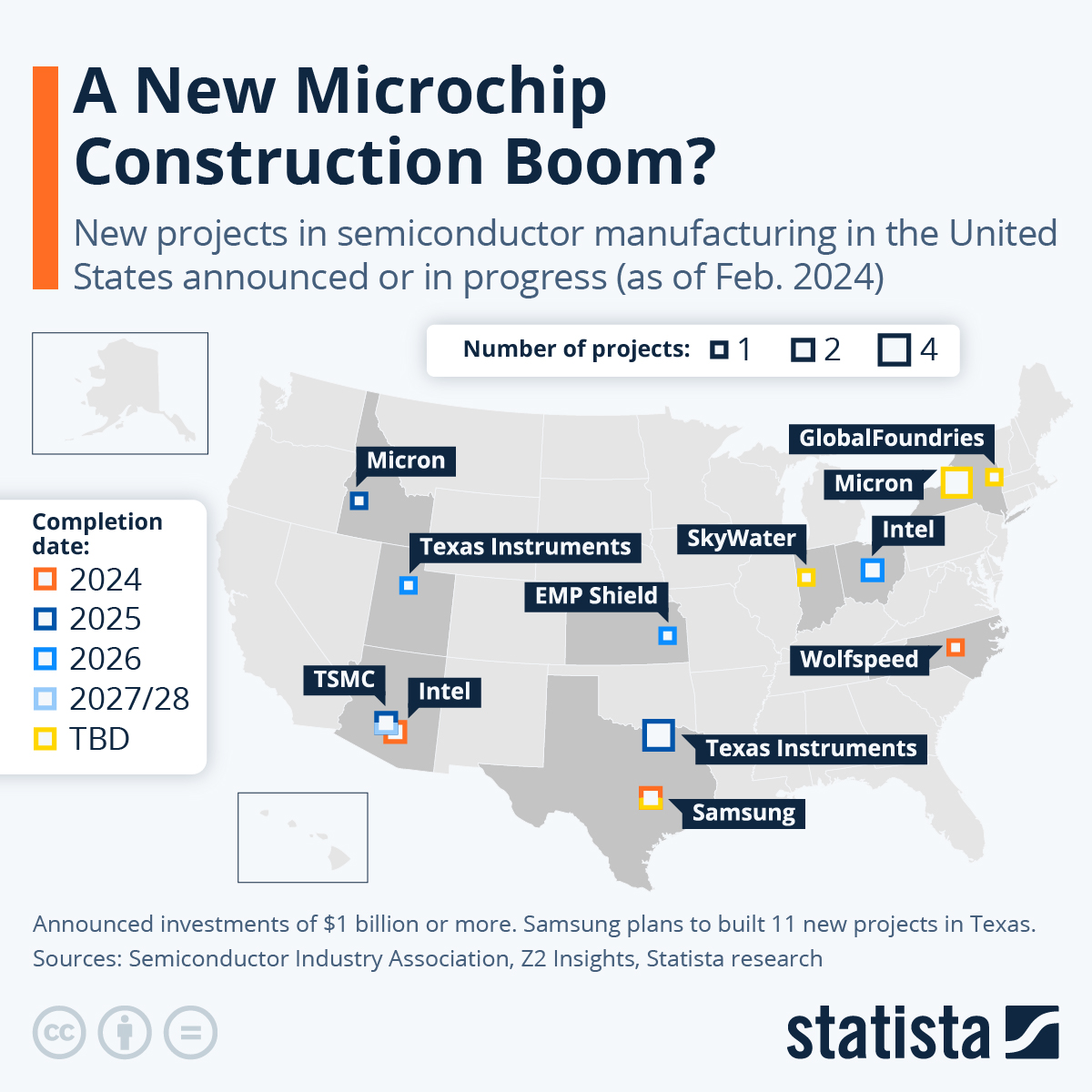

– Analysis: TSMC’s advanced fabs in Arizona (expected online in phases by 2025–2026) will bolster U.S. onshoring efforts. Samsung and Intel are also expanding U.S. and EU manufacturing capacity with government subsidies (CHIPS Act, EU Chips Act). Meanwhile, China will accelerate domestic semiconductor capabilities via SMIC and Huawei’s HiSilicon, though likely limited to mature and mid-node processes due to export controls.

– Outlook: By 2026, a “three-pole” semiconductor ecosystem may emerge: U.S./Allied (TSMC, Intel, Samsung), China (SMIC, YMTC), and hybrid global supply chains, increasing complexity and cost.

3. Advanced Packaging and Chiplet Adoption

– Key Players: TSMC (CoWoS, SoIC), Intel (Foveros), Samsung (I-Cube)

– Trend: Moore’s Law slowdown is accelerating innovation in packaging.

– Analysis: TSMC’s CoWoS (Chip-on-Wafer-on-Substrate) capacity is a bottleneck in H2 2024, with lead times exceeding 12 months. By 2026, TSMC, Intel, and Samsung are expected to scale heterogeneous integration and chiplet solutions, enabling more powerful and energy-efficient systems.

– Outlook: Advanced packaging market could reach $60B+ by 2026 (Yole Group). Companies with in-house packaging tech (e.g., TSMC, Intel) will gain competitive advantage.

4. Automotive and Edge AI Expansion

– Key Players: NVIDIA (DRIVE), Qualcomm, NXP, Infineon, AMD (Xilinx)

– Trend: Automotive semiconductors (especially for ADAS, EVs, cockpit systems) will grow steadily.

– Analysis: By 2026, AI inference at the edge (in vehicles, factories, IoT) will drive demand for low-power, high-efficiency chips. NVIDIA’s DRIVE Thor and Qualcomm’s Snapdragon Digital Chassis are positioned to capture premium EV segments. Xilinx FPGAs (AMD) remain strong in industrial and automotive customization.

– Outlook: Automotive semiconductor market projected to exceed $100B by 2026 (McKinsey), with AI-enabled systems accounting for over 30% of growth.

5. Memory Market Recovery and Next-Gen Tech

– Key Players: Samsung, SK Hynix, Micron

– Trend: After a cyclical downturn in 2023–2024, memory (DRAM, NAND) markets are rebounding in H2 2024.

– Analysis: AI-driven demand for High Bandwidth Memory (HBM) is surging. By 2026, HBM4 and next-gen GDDR7 will be critical for AI/ML workloads. Samsung and SK Hynix lead HBM supply; Micron is catching up. NAND demand will be fueled by data centers, AI storage, and client SSDs.

– Outlook: Memory sector could see strong margins in 2025–2026, especially for HBM, which may represent 20%+ of DRAM revenue by 2026.

6. RISC-V and Architecture Diversification

– Key Players: Alibaba (T-Head), Qualcomm, SiFive, NVIDIA (Grace CPU)

– Trend: RISC-V adoption is accelerating in IoT, automotive, and AI accelerators.

– Analysis: While x86 and Arm remain dominant, RISC-V offers cost and customization benefits. By 2026, we may see RISC-V cores embedded in AI SoCs and edge devices, particularly in China and emerging markets.

– Outlook: RISC-V chip shipments could exceed 80 billion by 2026 (Semico Research), though revenue share remains modest.

7. Sustainability and Energy Efficiency

– Trend: As AI data centers consume more power, energy-efficient chips become critical.

– Analysis: Top semiconductor firms will emphasize performance-per-watt metrics. NVIDIA’s Blackwell, AMD’s MI300, and Intel’s Gaudi 3 all emphasize efficiency. Cooling and packaging innovations (e.g., liquid cooling, 3D stacking) will be essential.

– Outlook: By 2026, energy efficiency could be a key differentiator in data center procurement decisions.

Summary: Key 2026 Market Outlook by Company

| Company | 2026 Growth Driver | Risk Factor |

|————-|—————————————-|————————————|

| NVIDIA | AI GPUs, data center, automotive | Competition, supply constraints |

| AMD | AI (MI300), data center CPUs, Xilinx | Execution in AI market |

| Intel | Gaudi AI, foundry growth, 18A node | Foundry scalability, competition |

| TSMC | CoWoS packaging, 2nm node, AI demand | Geopolitical risk, capacity cap |

| Samsung | HBM, foundry, memory leadership | Foundry profitability, capex |

| Broadcom | AI networking (Tomahawk, Jericho) | Dependence on cloud capex |

| Qualcomm | Auto, edge AI, RISC-V expansion | Auto market competition |

Conclusion:

By 2026, the semiconductor market will be defined by AI dominance, geopolitical realignment, advanced packaging, and specialized computing. Top players with strong AI exposure, manufacturing leadership (TSMC, Intel), and vertical integration (NVIDIA, AMD) are best positioned. However, supply chain fragility, technical bottlenecks (e.g., packaging capacity), and regulatory challenges will remain key risks.

Note: This analysis is based on H2 2024 data and projections from industry sources including Gartner, McKinsey, Yole Group, and Bloomberg Intelligence. Actual 2026 outcomes will depend on unforeseen technological breakthroughs, macroeconomic conditions, and policy developments.

Common Pitfalls in Sourcing Top-Tier Semiconductors: Quality and Intellectual Property Risks

Sourcing high-performance semiconductors is critical for maintaining product reliability, performance, and competitiveness. However, organizations frequently encounter significant challenges related to quality assurance and intellectual property (IP) protection. Overlooking these risks can result in costly failures, legal disputes, and reputational damage.

Poor Quality Control and Counterfeit Components

One of the most prevalent pitfalls is the unintentional procurement of substandard or counterfeit semiconductor components. These may originate from unauthorized distributors, gray market channels, or suppliers lacking rigorous quality certifications. Counterfeit chips—often remarked, recycled, or outright fakes—can exhibit erratic behavior, early failure, or complete malfunction, leading to field failures and safety hazards. Additionally, inconsistent process control from low-tier foundries may result in parametric drift or reduced device longevity, undermining system reliability.

Inadequate Supplier Qualification and Auditing

Many companies fail to thoroughly vet semiconductor suppliers, especially when pursuing cost savings or faster time-to-market. Skipping on-site audits, neglecting to verify ISO 9001 or IATF 16949 certifications, or overlooking a supplier’s manufacturing traceability systems increases the risk of receiving non-conforming products. Without rigorous supplier qualification, organizations may become dependent on vendors with weak quality management systems or limited process controls, especially in advanced nodes where process variation significantly impacts yield and performance.

Insufficient IP Protection and Licensing Clarity

Intellectual property risks are particularly acute in semiconductor sourcing. Organizations may inadvertently use IP-protected designs, firmware, or process technologies without proper licensing, exposing themselves to litigation. This is common when sourcing application-specific integrated circuits (ASICs) or using third-party design libraries (e.g., ARM cores). Ambiguous IP ownership clauses in supply agreements—or lack thereof—can result in disputes over design rights, derivative works, or reuse permissions, especially when engaging offshore design houses or foundries.

Reliance on Obsolete or End-of-Life (EOL) Components

Sourcing components without verifying lifecycle status can lead to dependency on obsolete semiconductors. While some suppliers offer “last time buy” options, continued reliance on EOL parts introduces long-term supply chain vulnerability. Furthermore, obsolete components are more likely to be counterfeited due to high demand and limited availability, compounding quality and authenticity risks.

Lack of Traceability and Chain of Custody

Without full traceability—from wafer fabrication through assembly and test—companies cannot verify the origin or handling history of a semiconductor. Breaks in the chain of custody increase the risk of tampering, remarking, or exposure to electrostatic discharge (ESD) and moisture, all of which can degrade performance. This is especially critical in aerospace, medical, and automotive applications where component pedigree is mandatory.

Overlooking Geopolitical and Export Control Risks

Global semiconductor supply chains are subject to export regulations (e.g., U.S. EAR, China’s export controls) and geopolitical tensions. Sourcing high-end chips from certain regions may inadvertently violate trade restrictions or expose IP to unwanted technology transfer. Failure to conduct due diligence on export compliance can result in shipment seizures, fines, or sanctions.

Conclusion

Mitigating these pitfalls requires a strategic approach: rigorous supplier qualification, robust quality audits, clear IP agreements, lifecycle management, and end-to-end traceability. Companies must prioritize long-term reliability and legal compliance over short-term cost savings to ensure the integrity and security of their semiconductor supply chain.

Logistics & Compliance Guide for Top Semiconductor

This guide outlines essential logistics and compliance procedures for Top Semiconductor, ensuring smooth operations, regulatory adherence, and supply chain integrity across global markets.

Shipping and Transportation Management

Top Semiconductor utilizes a multimodal transportation strategy, combining air, sea, and ground freight to optimize delivery times and costs. High-priority semiconductor wafers and finished chips are typically shipped via air freight under strict temperature and static-controlled conditions. Bulk raw materials and equipment move via ocean freight with climate-controlled containers. All shipments must comply with carrier-specific requirements, including hazardous material classifications when applicable (e.g., certain chemical precursors). Real-time tracking and digital documentation are mandatory for all outbound and inbound logistics.

Customs and Import/Export Compliance

All international shipments must adhere to the export control regulations of the country of origin and the import laws of the destination country. Top Semiconductor complies with key regulatory frameworks, including the U.S. Export Administration Regulations (EAR), EU Dual-Use Regulation, and China’s Export Control Law. Export licenses are required for restricted technologies and must be obtained prior to shipment. Accurate Harmonized System (HS) codes, commercial invoices, packing lists, and Certificates of Origin must accompany every shipment. The company maintains an internal screening process to ensure entities are not on denied or restricted parties lists (e.g., BIS Denied Persons List).

Environmental, Health, and Safety (EHS) Standards

Top Semiconductor enforces strict EHS protocols throughout its logistics chain. Hazardous materials (e.g., photoresists, etching gases) are handled, labeled, and transported in accordance with OSHA, REACH, and ADR/IATA/IMDG regulations. All logistics partners must demonstrate compliance with ISO 14001 and OHSAS 18001 or equivalent standards. Regular audits are conducted to ensure proper waste disposal, spill prevention, and employee safety training. Sustainability goals include reducing carbon emissions through route optimization and transitioning to eco-friendly packaging materials.

Supply Chain Security and Integrity

To prevent counterfeiting and ensure product authenticity, Top Semiconductor implements a secure supply chain protocol aligned with ISO 28000 and C-TPAT guidelines. This includes tamper-evident packaging, serialized tracking, and restricted access to high-value inventory. Third-party logistics (3PL) providers are vetted for cybersecurity practices, especially when handling sensitive design data or shipment information. All suppliers and distributors must sign confidentiality and compliance agreements.

Regulatory Documentation and Recordkeeping

Complete and accurate documentation is required for all logistics operations. Key records include:

– Export Control Classification Numbers (ECCNs) for all controlled items

– Technical data transfer authorizations

– Bill of Materials (BOM) with country-of-origin details

– Proof of compliance with RoHS, REACH, and Conflict Minerals regulations

All records must be retained for a minimum of five years and made available for regulatory audits upon request. Digital archiving systems are used to ensure data integrity and accessibility.

Incident Response and Non-Compliance Protocol

Any logistics or compliance breach (e.g., shipment delay, customs seizure, safety incident) must be reported immediately to the Global Compliance Office. A formal incident report is required within 24 hours, followed by root cause analysis and corrective action planning. Escalation procedures are in place for regulatory notifications, including filing Voluntary Self-Disclosures (VSDs) when appropriate. Employees are trained annually on compliance reporting channels and whistleblower protections.

Continuous Improvement and Training

Top Semiconductor conducts biannual reviews of logistics performance and compliance adherence. Staff and partners undergo mandatory training on export controls, EHS standards, and anti-bribery laws (e.g., FCPA, UK Bribery Act). Feedback from audits and incidents informs updates to this guide, ensuring alignment with evolving global regulations and industry best practices.

In conclusion, sourcing from top semiconductor manufacturers requires a strategic approach that balances technological capability, production capacity, supply chain reliability, and long-term partnerships. Leading manufacturers such as TSMC, Samsung Foundry, Intel, and others offer advanced process nodes, high yield rates, and robust quality control, making them ideal partners for high-performance applications in industries ranging from consumer electronics to automotive and aerospace.

When selecting a semiconductor supplier, key considerations include technological leadership, foundry capacity, geographic location, scalability, and compliance with international standards. Additionally, geopolitical factors, trade regulations, and supply chain resilience have become increasingly critical in recent years, prompting companies to diversify sourcing strategies and consider nearshoring or regional partnerships.

Ultimately, building strong relationships with top-tier manufacturers—supported by dual-sourcing options and strategic inventory planning—enables organizations to mitigate risks, accelerate time-to-market, and maintain a competitive edge in a rapidly evolving industry. As demand for semiconductors continues to grow, proactive engagement with premier suppliers will remain a cornerstone of innovation and operational success.