The global steel manufacturing industry continues to expand, fueled by rising demand across construction, automotive, and infrastructure sectors. According to a 2023 report by Mordor Intelligence, the global steel market was valued at approximately USD 1.2 trillion in 2022 and is projected to grow at a CAGR of over 4.5% from 2023 to 2028. This growth is driven by urbanization, industrialization—particularly in Asia-Pacific—and increasing investments in sustainable steel production technologies. As competition intensifies, a select group of manufacturers have emerged as industry leaders, combining scale, innovation, and global reach. Based on production volume, revenue, and market influence, the following seven companies represent the top steel producers worldwide, shaping the future of one of the most critical materials in modern manufacturing and construction.

Top 7 Top Steel In The World Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Top Steel In The World

2026 Market Trends for Top Steel in the World

As the global economy continues to evolve in the post-pandemic era, the steel industry—particularly the top steel-producing nations and companies—is poised for significant transformation by 2026. Driven by technological innovation, environmental regulations, shifting demand patterns, and geopolitical dynamics, the world steel market is entering a phase of strategic recalibration. This analysis explores the key market trends expected to shape the landscape for top steel producers globally in 2026.

Global Production and Leading Producers

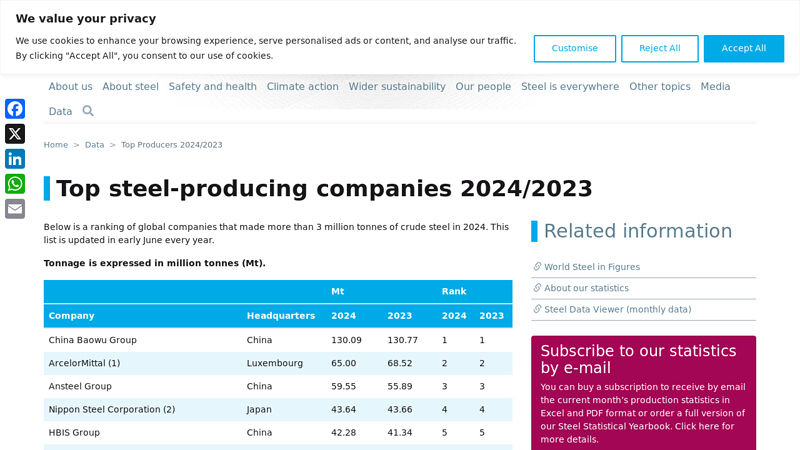

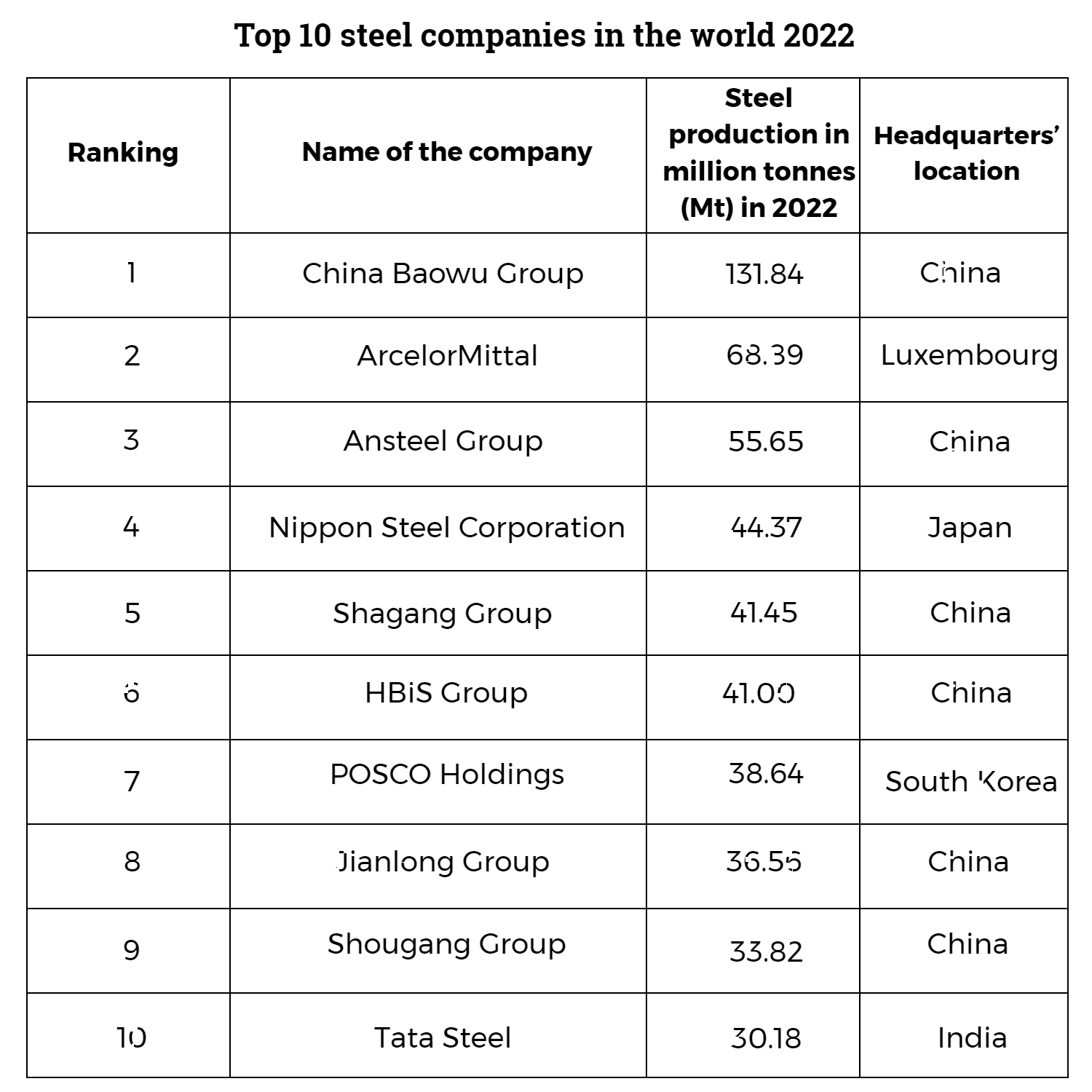

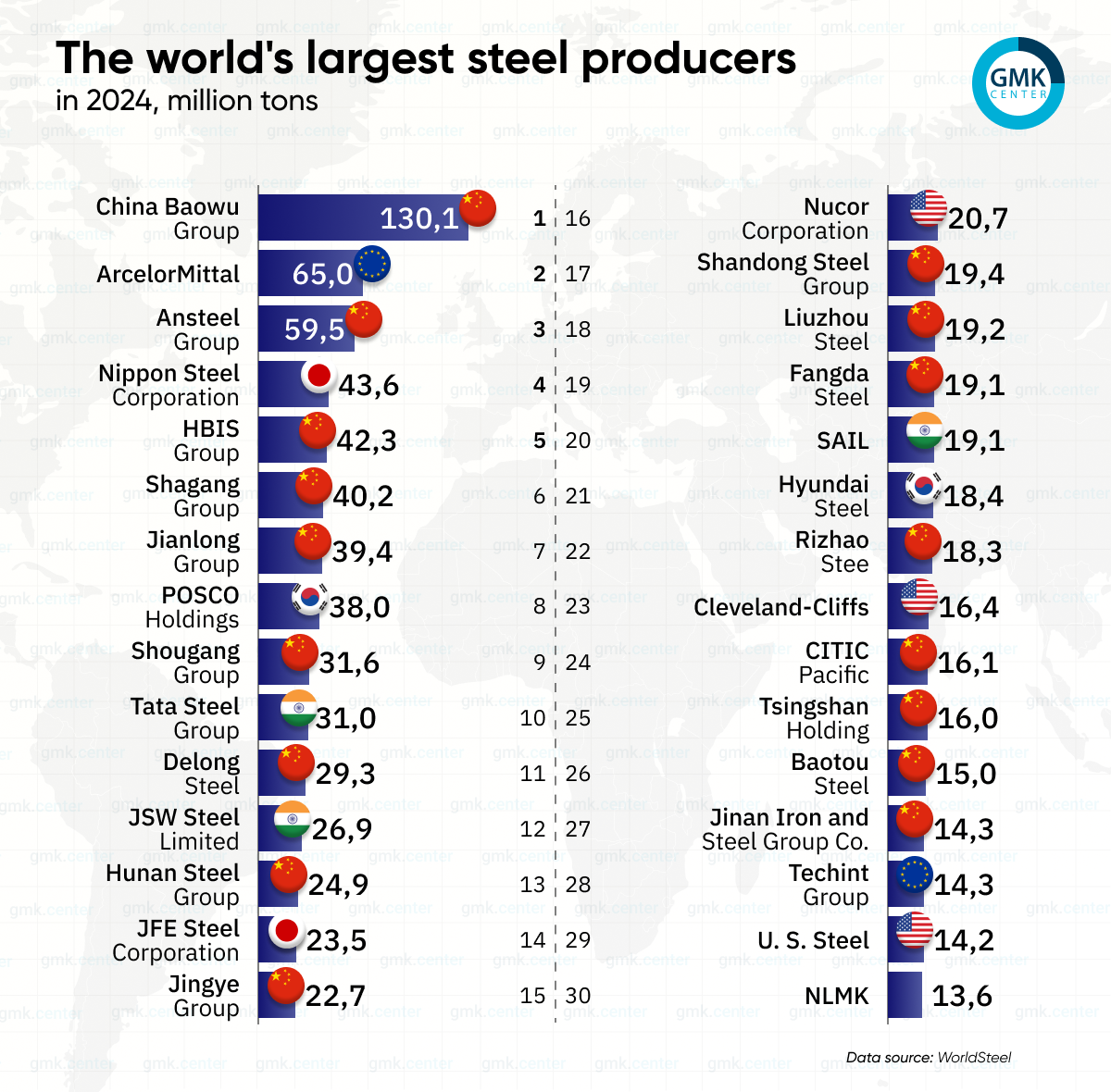

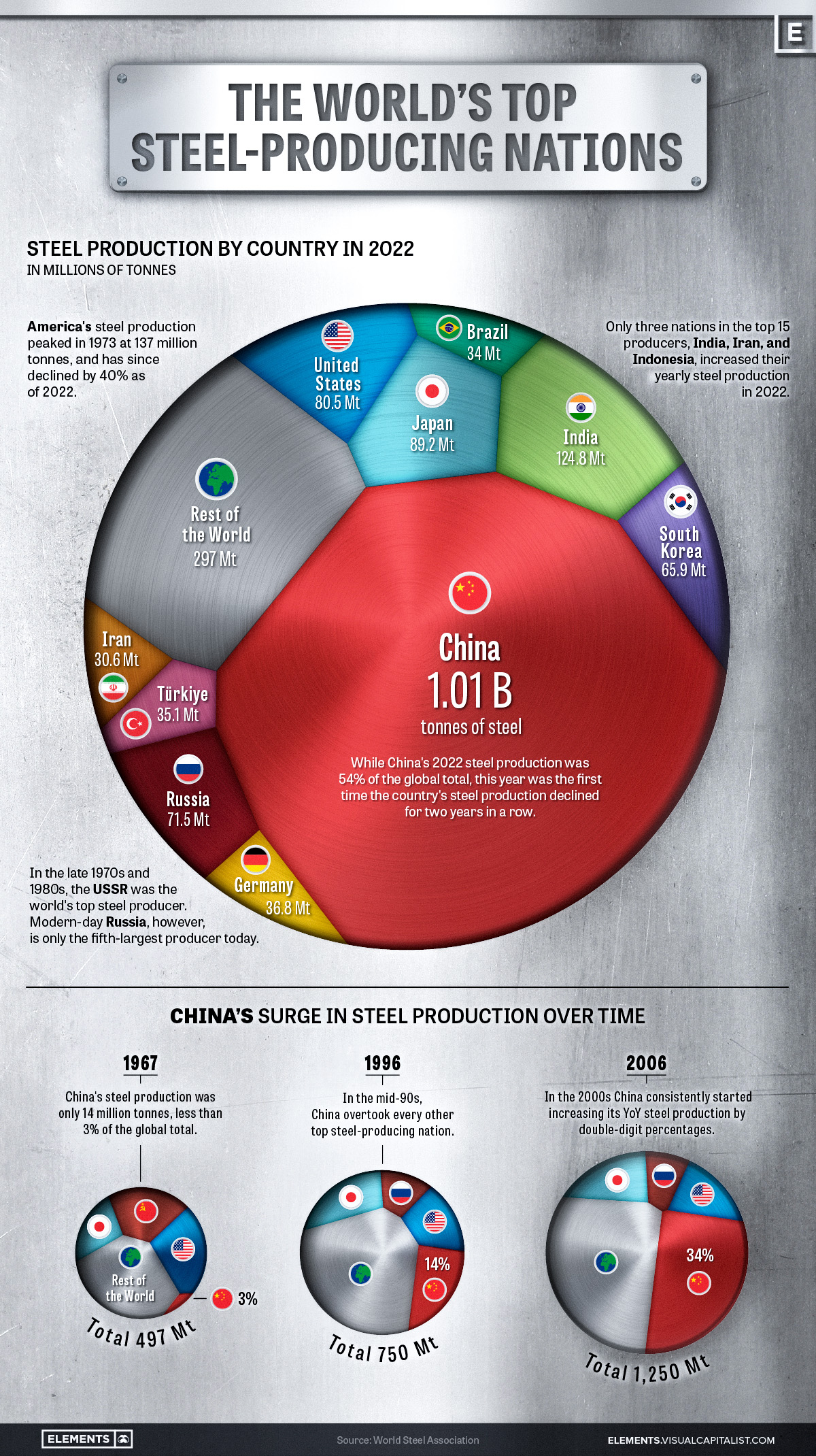

By 2026, China is expected to maintain its position as the world’s largest steel producer, though its growth will likely slow due to domestic economic rebalancing and government-driven de-carbonization policies. The National Development and Reform Commission (NDRC) has set aggressive targets to cap steel output and reduce reliance on coal-based production, pushing Chinese steelmakers toward electric arc furnaces (EAFs) and greener technologies.

India is projected to emerge as the second-largest steel producer, with output potentially surpassing 150 million metric tons by 2026. Supported by strong infrastructure development and government initiatives such as the National Steel Policy, Indian steel companies like Tata Steel and JSW Steel are expanding capacity and investing in modern, low-emission plants.

Outside Asia, the United States and the European Union are reinvigorating their steel sectors. In the U.S., the Inflation Reduction Act (IRA) and infrastructure spending are driving demand for domestically produced, low-carbon steel. Companies like Nippon Steel USA and Cleveland-Cliffs are investing heavily in EAF technology and hydrogen-based reduction methods.

In Europe, despite short-term challenges from high energy costs, the Green Deal and Carbon Border Adjustment Mechanism (CBAM) are accelerating the shift toward green steel. Swedish innovator HYBRIT (a joint venture by SSAB, LKAB, and Vattenfall) is expected to scale up commercial production of fossil-free steel by 2026, setting a benchmark for sustainability.

Technological Advancements and Green Steel Transition

A defining trend for 2026 is the global pivot toward green steel—steel produced with minimal carbon emissions. Hydrogen-based direct reduced iron (DRI) and carbon capture, utilization, and storage (CCUS) technologies are moving from pilot stages to commercial deployment.

Top steel companies are aligning with net-zero targets. ArcelorMittal, the world’s second-largest steelmaker, plans to reduce CO₂ emissions by 25% by 2030, with significant investments in Smart Carbon technology and XCarb™ innovations. Similarly, South Korea’s POSCO is advancing its FINEX and HYBREX technologies to cut emissions and improve efficiency.

Digitalization is another key driver. By 2026, artificial intelligence, predictive maintenance, and digital twins will be standard across leading steel plants, improving yield, reducing downtime, and optimizing energy use. Smart factories in Germany, Japan, and China exemplify the integration of Industry 4.0 in steel production.

Demand Dynamics and Sectoral Shifts

Global steel demand in 2026 will be shaped by construction, automotive, and renewable energy sectors. Urbanization in Africa and Southeast Asia will sustain demand for rebar and structural steel. Meanwhile, the electric vehicle (EV) revolution is increasing demand for advanced high-strength steels (AHSS), which offer lightweighting and durability.

The renewable energy sector—especially wind turbines and solar panel mounting systems—will be a growing market for specialized steel grades. Offshore wind projects in Europe and the U.S. are requiring high-grade corrosion-resistant steel, creating new opportunities for premium producers.

Conversely, traditional demand from fossil fuel infrastructure may wane due to energy transition policies, prompting steel companies to diversify their product portfolios.

Trade Policies and Geopolitical Factors

Trade dynamics will continue to influence the global steel market in 2026. The U.S. and EU are expected to maintain safeguards against steel dumping, particularly from overcapacity regions. The CBAM will impose carbon costs on imported steel, giving low-emission domestic producers a competitive edge.

Geopolitical tensions, including U.S.-China relations and the ongoing impact of sanctions on Russia, will affect supply chains. Russian steel exports are likely to be rerouted to Asia and Africa, while Western markets increasingly source from trusted, ESG-compliant suppliers.

Conclusion

By 2026, the world’s top steel producers will be defined not just by volume, but by sustainability, innovation, and resilience. The convergence of environmental regulation, technological disruption, and shifting demand is reshaping the competitive landscape. Companies that invest in green technologies, digital transformation, and strategic market positioning will lead the next era of global steel production. The future belongs to those who can deliver high-quality steel with a low carbon footprint—ushering in a new chapter for one of the world’s oldest and most essential industries.

Common Pitfalls Sourcing Top Steel in the World (Quality, IP)

Sourcing high-quality steel from top global producers offers performance and reliability benefits, but it comes with significant risks related to quality consistency and intellectual property (IP) protection. Falling into common pitfalls can lead to project delays, safety issues, and legal complications.

Quality Inconsistencies Despite Reputable Suppliers

Even when sourcing from globally recognized steel manufacturers, buyers may encounter inconsistent quality due to variations in production batches, third-party processing, or inadequate quality control during logistics and handling. Some suppliers may outsource part of the manufacturing process, leading to deviations from original specifications. Without rigorous third-party inspection and certification (e.g., ISO, ASTM, EN standards), companies risk receiving substandard material that compromises structural integrity.

Misrepresentation of Steel Grades and Certifications

A frequent issue is the mislabeling or falsification of steel grades and mill test certificates (MTCs). Some suppliers, particularly in complex supply chains, may provide counterfeit documentation claiming compliance with international standards (e.g., ASTM A36, EN 10025) when the material does not meet those specifications. This misrepresentation can lead to regulatory non-compliance and safety hazards in critical applications like construction or energy infrastructure.

Intellectual Property (IP) Risks in Custom Alloys and Proprietary Processes

When sourcing advanced or custom-engineered steel (e.g., high-strength low-alloy steels or corrosion-resistant grades), there’s a risk of inadvertently infringing on patented technologies. Top steel producers often hold IP rights over specific compositions, manufacturing methods (e.g., thermomechanical rolling), or coatings. Sourcing without proper due diligence—such as verifying licensing agreements or freedom-to-operate—can expose buyers to legal disputes, import bans, or financial liabilities.

Supply Chain Transparency and Traceability Gaps

Global steel sourcing often involves multiple intermediaries, making it difficult to trace the material’s origin and processing history. This lack of transparency increases the risk of receiving steel produced using unethical labor practices or in violation of environmental regulations, which can damage brand reputation and lead to compliance issues under laws like the U.S. Uyghur Forced Labor Prevention Act (UFLPA).

Inadequate Contracts and Enforcement Challenges

Many sourcing agreements fail to clearly define quality benchmarks, inspection protocols, and IP indemnification clauses. When disputes arise, enforcing these terms across international jurisdictions can be costly and time-consuming. Weak contracts leave buyers with limited recourse in cases of non-conformance or IP infringement.

To mitigate these pitfalls, companies should conduct thorough supplier audits, require independent material testing, secure IP clearances, and establish clear contractual terms with enforceable quality and compliance standards.

Logistics & Compliance Guide for Top Steel in the World

Overview

This guide outlines essential logistics and compliance procedures for Top Steel, a leading global steel manufacturer and distributor. Adherence to these standards ensures efficient operations, regulatory compliance, and customer satisfaction across international markets.

International Shipping & Transportation

Top Steel utilizes multimodal transportation—sea, rail, and road—to deliver steel products globally. Key logistics considerations include:

– Containerization: Steel coils, plates, and sections are secured in ISO containers or flat-rack containers to prevent damage.

– Route Optimization: Strategic routing minimizes transit time and fuel consumption, especially for bulk shipments.

– Carrier Selection: Partnerships with certified logistics providers ensure reliability and adherence to safety standards.

– Temperature & Handling: Steel products must be protected from moisture and extreme temperatures during transit to prevent corrosion.

Customs Compliance

Compliance with import/export regulations is mandatory in every jurisdiction Top Steel operates. Key requirements include:

– Accurate Documentation: Commercial invoices, packing lists, certificates of origin, and bill of lading must be complete and error-free.

– HS Code Classification: Steel products must be correctly classified under the Harmonized System (HS) codes (e.g., 7208–7229 for iron and steel).

– Trade Agreements: Leverage preferential tariffs under agreements such as USMCA, EU-South Korea FTA, or ASEAN Free Trade Area where applicable.

– Export Controls: Adhere to sanctions and restrictions imposed by OFAC (U.S.), EU, and UN on certain destinations.

Regulatory & Safety Standards

Top Steel complies with international and regional safety and quality standards:

– ISO Certifications: Maintain ISO 9001 (Quality Management), ISO 14001 (Environmental Management), and ISO 45001 (Occupational Health & Safety).

– Product Standards: Steel products must meet ASTM (U.S.), EN (Europe), JIS (Japan), or GB (China) specifications as required by customers.

– REACH & RoHS Compliance: Ensure steel products are free from restricted hazardous substances when shipped to the EU.

– Dangerous Goods Handling: Although steel is generally non-hazardous, coated or treated steel may require special handling documentation.

Environmental & Sustainability Compliance

As part of global ESG commitments, Top Steel adheres to environmental regulations:

– Carbon Reporting: Monitor and report emissions in line with local regulations and initiatives like CBAM (Carbon Border Adjustment Mechanism) in the EU.

– Waste Management: Recycle scrap metal and manage industrial by-products according to EPA, EEA, or equivalent standards.

– Sustainable Sourcing: Ensure raw materials (e.g., iron ore, coal) are sourced from suppliers complying with environmental and labor laws.

Documentation & Recordkeeping

Robust documentation is critical for traceability and audits:

– Maintain records of shipment manifests, customs filings, quality test reports, and compliance certificates for a minimum of 5 years.

– Use digital logistics platforms (e.g., TMS, ERP systems) to track shipments and ensure real-time compliance monitoring.

Risk Management & Contingency Planning

Anticipate and mitigate logistics disruptions:

– Monitor geopolitical risks, port congestion, and weather events.

– Maintain alternative shipping routes and backup suppliers.

– Secure cargo insurance covering theft, damage, and delays.

Training & Internal Audits

- Conduct regular training for logistics and compliance teams on updated trade regulations and safety protocols.

- Perform internal audits quarterly to verify adherence to compliance standards and identify improvement areas.

Conclusion

By following this Logistics & Compliance Guide, Top Steel ensures smooth global operations, minimizes legal risks, and upholds its reputation as a reliable, responsible industry leader. All departments must collaborate to maintain compliance and operational excellence worldwide.

In conclusion, identifying the top steel manufacturers in the world involves evaluating key factors such as production capacity, technological innovation, product quality, global market presence, and sustainability practices. Leading companies such as China Baowu Steel Group, ArcelorMittal, Nippon Steel, POSCO, and JSW Steel stand out due to their large-scale operations, advanced manufacturing processes, and consistent commitment to meeting international standards. These industry leaders not only dominate global output but also drive advancements in green steel production and digital transformation within the sector. For businesses seeking reliable and high-quality steel supply, partnering with these top-tier manufacturers ensures access to superior materials, technological expertise, and long-term supply chain stability in an increasingly competitive and environmentally conscious market.