The Turkish manufacturing sector has emerged as a pivotal force in the global supply chain, with steady growth fueled by strategic geography, competitive labor costs, and strong industrial diversification. According to Mordor Intelligence, the Turkey Manufacturing Market is projected to grow at a CAGR of over 5.8% from 2024 to 2029, driven by rising exports, government incentives for industrial investment, and advancements in automation and digitalization across key sectors such as automotive, textiles, and machinery. Grand View Research further supports this trajectory, noting that Turkey’s industrial production index has shown consistent year-on-year increases, bolstered by robust domestic demand and expanding trade relationships with both European and Middle Eastern markets. As global sourcing strategies increasingly favor resilient and cost-efficient manufacturing hubs, Turkey has solidified its position as a top destination for high-quality, scalable production. This data-backed growth underscores the importance of recognizing the country’s leading manufacturers—innovators who combine engineering excellence with export-ready capabilities.

Top 10 Turkey Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Turkey

H2: Market Trends in Turkey for 2026

As Turkey moves into 2026, its economy and market landscape are shaped by a confluence of domestic reforms, geopolitical dynamics, technological advancement, and regional integration efforts. Following a period of economic volatility marked by currency fluctuations and inflationary pressures in the early 2020s, Turkey’s market in 2026 reflects cautious optimism, driven by structural adjustments, digital transformation, and strategic positioning in global trade.

1. Economic Stabilization and Monetary Policy Shifts

By H2 2026, Turkey’s economy shows signs of stabilization after the Central Bank of the Republic of Turkey (CBRT) implemented more orthodox monetary policies. Having shifted away from unorthodox low-interest-rate experiments, the CBRT has maintained a tighter policy stance since late 2023, leading to a gradual decline in inflation—from triple digits in 2022 to approximately 25–30% in early 2026. The Turkish lira (TRY) remains volatile but has stabilized relative to previous years, supported by higher interest rates and increased foreign reserves.

The government has also introduced fiscal discipline measures, reducing budget deficits and enhancing public debt sustainability. These efforts have improved investor confidence, particularly among European and Gulf investors seeking high-yield opportunities in emerging markets.

2. Digital Transformation and Fintech Expansion

Turkey’s technology sector continues to surge, with H2 2026 marking a peak in digital adoption across businesses and consumers. Fintech is a standout performer, fueled by a young, tech-savvy population and increasing smartphone penetration. Digital banking, mobile payments, and e-commerce platforms are expanding rapidly, with local fintech startups attracting significant venture capital from both domestic and international sources.

The government’s “Digital Turkey 2026” initiative has accelerated the rollout of 5G infrastructure and broadband access, enabling digital services in rural and underserved areas. E-government services, e-health, and smart city projects are also gaining traction, improving efficiency and transparency.

3. Green Energy and Sustainability Investments

Energy transition is a key theme in 2026. Turkey has increased its renewable energy capacity, particularly in wind, solar, and geothermal power, aiming to reduce reliance on imported fossil fuels and meet EU-aligned climate goals. The country is leveraging its geographic advantage to become a regional energy hub, with upgraded grid infrastructure and cross-border electricity interconnections.

Sustainability is becoming a core consideration for investors. Environmental, Social, and Governance (ESG) criteria are increasingly integrated into corporate strategies, especially among export-oriented manufacturers and firms seeking access to European markets. Green bonds and sustainability-linked loans are gaining popularity in capital markets.

4. Manufacturing and Export-Led Growth

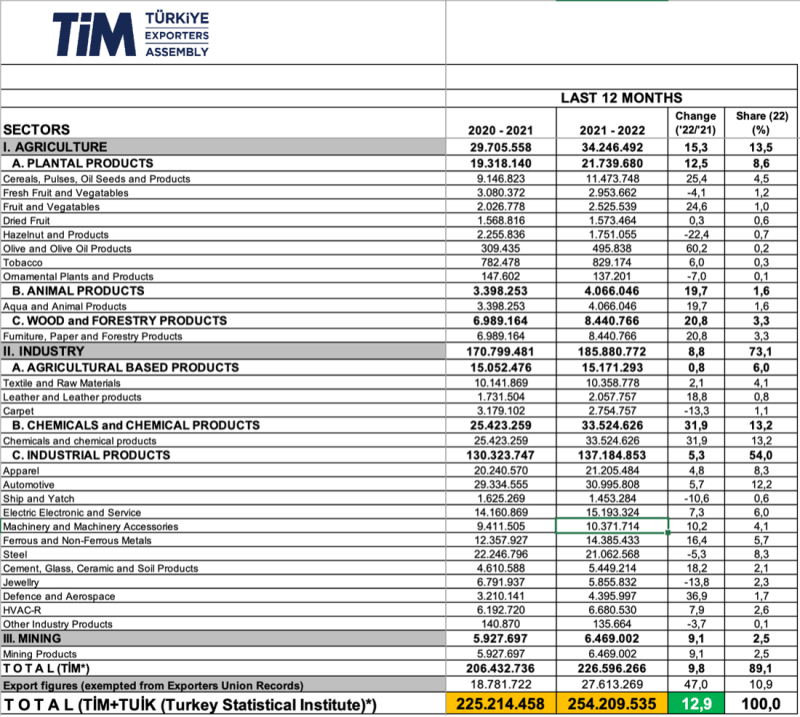

Turkey’s industrial base remains resilient, with strong performance in automotive, textiles, defense, and electronics manufacturing. In H2 2026, exports are a primary engine of growth, supported by free trade agreements with the EU, the UK, and several Middle Eastern and African countries. The “Make in Türkiye” campaign has attracted foreign direct investment (FDI), particularly in high-value manufacturing and R&D centers.

The defense and aerospace sector, led by firms like Baykar and Turkish Aerospace Industries (TAI), continues to expand, with increasing exports of drones and aircraft to Africa, Asia, and Eastern Europe. This sector is a major contributor to the trade surplus and technological self-reliance.

5. Real Estate and Urban Development

The real estate market in Turkey remains robust, particularly in Istanbul, Ankara, and emerging cities like Izmir and Antalya. Demand is driven by foreign buyers—especially from Gulf countries, Russia, and Central Asia—drawn by citizenship-by-investment programs and relatively affordable luxury properties. However, regulatory scrutiny has increased to prevent speculative bubbles and ensure market transparency.

Urban regeneration projects, including the redevelopment of informal settlements (gecekondus) and smart city developments, are transforming metropolitan areas. These projects are supported by public-private partnerships and international financing institutions.

6. Geopolitical and Trade Dynamics

Turkey’s geopolitical positioning continues to influence its market environment. Its role in regional security, energy transit, and refugee management grants it strategic leverage with both NATO and neighboring states. Trade diversification is evident, with growing exports to Africa, Central Asia, and the Middle East, reducing overdependence on European markets.

Negotiations for enhanced cooperation with the European Union—though not full accession—have progressed, particularly in trade, customs union modernization, and digital regulation alignment. This has eased some investor concerns about policy predictability.

7. Labor Market and Demographic Trends

Turkey benefits from a young population, with over 60% under the age of 35. However, youth unemployment remains a challenge, prompting government and private-sector initiatives to improve vocational training and digital skills. The gig economy and remote work are expanding, especially in tech and creative industries.

Women’s labor force participation is slowly increasing, supported by childcare incentives and flexible work policies, though structural barriers persist.

Conclusion

In H2 2026, Turkey’s market reflects a maturing economy navigating post-crisis recovery with a focus on stability, innovation, and strategic diversification. While challenges such as inflation, geopolitical risks, and institutional reforms remain, the country is leveraging its geographic location, demographic strength, and industrial capabilities to position itself as a dynamic emerging market. Investors are cautiously optimistic, particularly in technology, energy, and manufacturing sectors, setting the foundation for sustained, albeit moderate, growth in the coming years.

Common Pitfalls When Sourcing from Turkey: Quality and Intellectual Property Risks

Sourcing products from Turkey offers numerous advantages, including strategic geographic location, competitive pricing, and a skilled manufacturing base. However, companies must be aware of potential pitfalls related to product quality and intellectual property (IP) protection to avoid costly setbacks.

Quality Control Challenges

One of the primary concerns when sourcing from Turkey is maintaining consistent product quality. While many Turkish manufacturers meet international standards, disparities can exist across suppliers and production batches.

- Inconsistent Manufacturing Standards: Not all Turkish suppliers adhere to the same quality control protocols. Some may lack certifications such as ISO 9001, leading to variability in raw materials, workmanship, and final product quality.

- Limited Oversight: Without on-the-ground quality audits or third-party inspections, defects may go unnoticed until goods reach the destination market, resulting in returns, delays, or reputational damage.

- Communication Gaps: Misunderstandings due to language barriers or vague specifications can lead to deviations from product requirements. Clear technical documentation and regular communication are essential but often overlooked.

Intellectual Property Vulnerabilities

Protecting intellectual property when sourcing from Turkey requires proactive measures, as the country’s IP enforcement mechanisms can be inconsistent.

- Weak Enforcement of IP Rights: Although Turkey is a member of WIPO and has IP laws aligned with EU standards, enforcement can be slow and unpredictable. Counterfeiting and unauthorized replication of designs, molds, or proprietary technology remain risks.

- Lack of Supplier Vetting: Engaging with suppliers without thorough due diligence increases the risk of IP theft. Some manufacturers may share designs with competitors or produce unauthorized copies for other clients.

- Inadequate Contractual Protections: Many sourcing agreements lack robust IP clauses, such as clear ownership terms, confidentiality obligations, and restrictions on secondary production. Without these, legal recourse is limited in case of infringement.

Mitigation Strategies

To navigate these pitfalls, businesses should:

– Conduct factory audits and request quality certifications.

– Implement third-party pre-shipment inspections.

– Draft comprehensive contracts with explicit IP clauses.

– Register trademarks and designs in Turkey.

– Work with legally vetted partners and consider using escrow services for tooling and molds.

Proactive risk management is key to leveraging Turkey’s sourcing potential while safeguarding quality and intellectual assets.

Logistics & Compliance Guide for Turkey

Turkey serves as a strategic bridge between Europe, Asia, and the Middle East, making it a key hub for international trade. Understanding its logistics infrastructure and regulatory environment is essential for businesses planning to import, export, or distribute goods in the country.

Trade Regulations and Import/Export Controls

Turkey maintains a liberalized trade regime but enforces certain restrictions and controls on specific goods. The Ministry of Trade oversees trade policy and regulations. Importers and exporters must register with the Turkish Trade Registry and obtain a Tax Identification Number (TIN). Prohibited items include narcotics, counterfeit goods, and certain hazardous materials. Restricted goods—such as pharmaceuticals, firearms, and agricultural products—require prior authorization or permits from relevant authorities.

Customs Procedures and Documentation

Customs clearance in Turkey is managed by the Ministry of Trade and the Turkish Revenue Administration (Gelir İdaresi Başkanlığı). Required documentation typically includes:

- Commercial invoice

- Packing list

- Bill of lading or air waybill

- Certificate of origin (especially for preferential tariff treatment under free trade agreements)

- Import license or permit (for restricted goods)

- Turkish Customs Declaration Form (Gümrük Beyannamesi)

Customs duties and VAT are assessed based on the CIF (Cost, Insurance, Freight) value. Pre-arrival processing is encouraged to reduce clearance times, and automated systems like the National Single Window (Gümrük Bilgi Sistemi – GBS) streamline submissions.

Value-Added Tax (VAT) and Excise Duties

Turkey applies a standard VAT rate of 20%, with reduced rates of 10% and 1% on certain goods and services. VAT is levied on imports and payable at customs. Excise duties (ÖTV) apply to specific products such as alcohol, tobacco, petroleum products, and luxury vehicles. Rates vary depending on the product category and are calculated on top of customs duties.

Free Trade Zones (FTZs)

Turkey operates several Free Trade Zones (e.g., Istanbul, Izmir, Mersin) that offer significant benefits for international businesses. Activities in FTZs are exempt from customs duties, VAT, and excise taxes. Goods can be stored, processed, assembled, or re-exported without full customs clearance. However, moving goods from an FTZ to the domestic market triggers applicable taxes and compliance requirements.

Labeling and Product Compliance

Products sold in Turkey must comply with Turkish standards (published by TSE – Turkish Standards Institution) and labeling requirements. Labels must be in Turkish and include product details, manufacturer/importer information, ingredients (for food and cosmetics), safety warnings, and conformity marks where applicable. CE marking is accepted for many regulated products, but some sectors (e.g., telecommunications, electrical equipment) require additional national certifications.

Transportation and Logistics Infrastructure

Turkey has a well-developed multimodal logistics network:

- Road: Extensive highway system; trucks are the primary mode for domestic and regional freight.

- Rail: State-run TCDD manages freight rail; expanding high-capacity corridors connect to Europe and Asia.

- Sea: Major ports include Istanbul (Ambarli), Izmir, and Mersin, offering container, bulk, and Ro-Ro services.

- Air: Istanbul Airport is a major international cargo hub, supported by regional air freight facilities.

Temperature-controlled, hazardous materials, and oversized cargo transport require special permits and certified carriers.

Foreign Trade Regime and Incentives

Turkey has free trade agreements with the EU (via the Customs Union), EFTA, and several Middle Eastern and African countries. These agreements facilitate tariff-free or reduced-tariff access for qualifying goods. The government also offers investment incentives, including tax breaks, customs duty exemptions, and grants for companies operating in priority sectors or regions.

Intellectual Property and Restricted Parties Screening

Importers must respect intellectual property rights. Customs authorities can seize counterfeit goods upon rights holder request. Businesses should conduct due diligence and screen partners against sanctioned party lists, including those maintained by the Turkish Ministry of Treasury and Finance and international bodies like the UN and EU.

Conclusion

Successfully navigating logistics and compliance in Turkey requires careful planning, accurate documentation, and adherence to local regulations. Partnering with experienced customs brokers, legal advisors, and logistics providers can significantly ease market entry and ensure ongoing compliance. Staying updated on regulatory changes through official sources like the Ministry of Trade and Turkish Revenue Administration is crucial for sustained operations.

In conclusion, sourcing manufacturers in Turkey presents a compelling opportunity for businesses seeking high-quality production at competitive costs. Turkey’s strategic geographical location between Europe and Asia, well-developed manufacturing infrastructure, skilled labor force, and strong industrial clusters—particularly in textiles, automotive, machinery, and home goods—make it an attractive sourcing destination. Additionally, favorable trade agreements with the EU, EFTA, and other regions enhance export efficiency and reduce tariffs. However, successful sourcing requires due diligence in verifying supplier credibility, understanding local regulations, and managing logistics and communication effectively. With careful planning, cultural awareness, and strong supplier relationships, businesses can leverage Turkey’s manufacturing strengths to enhance supply chain resilience, reduce lead times, and improve overall product quality. Overall, Turkey stands out as a reliable and strategic sourcing partner in today’s global market.