The U.S. semiconductor industry continues to assert its global leadership amid surging demand for advanced electronics, artificial intelligence, and 5G infrastructure. According to market research by Grand View Research, the global semiconductor market was valued at USD 573.89 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 8.6% from 2023 to 2030. A significant portion of this growth is driven by U.S.-based innovation and manufacturing capabilities, supported by initiatives like the CHIPS and Science Act, which has catalyzed new investments in domestic production capacity. Mordor Intelligence projects similar momentum, forecasting the semiconductor market to grow at a CAGR of over 6.5% through 2028. As geopolitical dynamics and supply chain resilience become key priorities, American chipmakers are at the forefront of scaling next-generation technologies—from high-performance computing to automotive semiconductors—making this an opportune moment to examine the top 10 U.S. chip manufacturers shaping the future of the industry.

Top 10 Us Chip Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Us Chip

H2 2025–2026 Market Trends for U.S. Chip Industry

The U.S. semiconductor (chip) industry is poised for transformative growth and strategic shifts through the second half (H2) of 2025 and into 2026, driven by technological innovation, government support, geopolitical dynamics, and rising demand across key sectors. Below is an analysis of the major market trends shaping the industry in H2 2026.

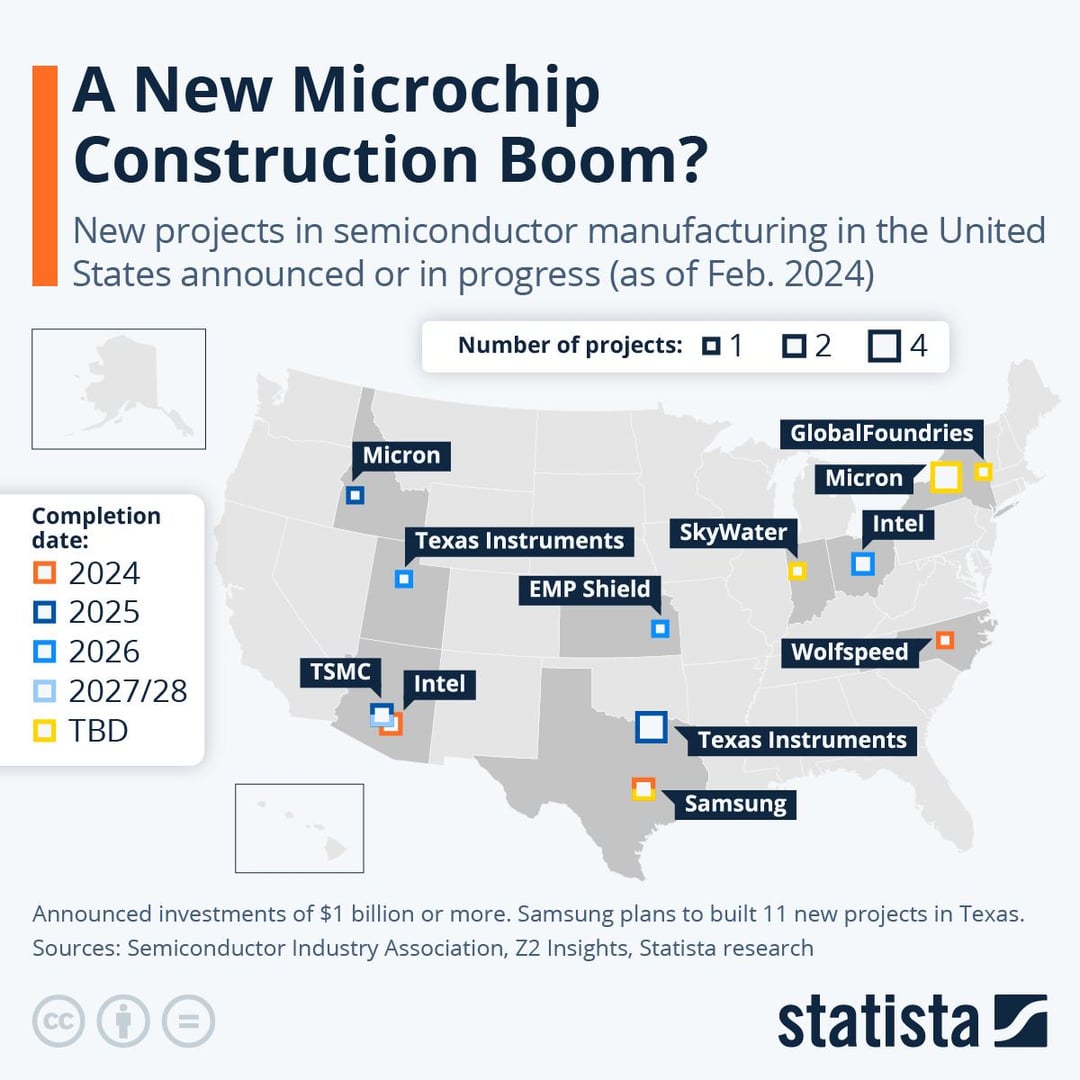

1. Accelerated Domestic Manufacturing (CHIPS Act Impact)

The U.S. CHIPS and Science Act continues to serve as a catalyst for reshoring semiconductor production. By H2 2026, several major fabrication plants (fabs) funded through CHIPS Act incentives are expected to become operational or reach critical milestones:

- Intel, TSMC, and Samsung are advancing multi-billion-dollar fab projects in Arizona, Ohio, and Texas, respectively.

- Domestic production of advanced nodes (sub-5nm and 3nm) is increasing, reducing reliance on Asia-Pacific supply chains.

- The U.S. share of global semiconductor manufacturing capacity is projected to rise from ~12% in 2023 to ~16–18% by end-2026.

This localized production strengthens supply chain resilience and supports national security objectives.

2. AI and Compute Demand Driving High-Performance Chips

Artificial intelligence remains the primary engine of semiconductor demand. In H2 2026:

- AI accelerators (GPUs, TPUs, NPUs) from NVIDIA, AMD, Intel, and custom silicon from cloud providers (Google, Amazon, Microsoft) dominate data center investments.

- Edge AI applications (autonomous vehicles, smart devices, industrial automation) drive demand for efficient, low-power chips.

- U.S. firms lead in AI chip design IP, with a growing ecosystem of startups (e.g., Cerebras, SambaNova, Groq) gaining traction.

This trend reinforces the U.S. competitive edge in chip design and innovation.

3. Geopolitical Tensions and Export Controls

U.S.-China tech rivalry continues to influence market dynamics:

- Export restrictions on advanced AI chips and semiconductor manufacturing equipment to China remain strict.

- Chinese firms accelerate domestic chip development, but still face challenges in advanced process nodes.

- U.S. allies (Japan, Netherlands, South Korea) align with export control regimes, limiting China’s access to cutting-edge tools.

These controls benefit U.S. chipmakers by protecting market leadership but also spur global diversification of supply chains.

4. Growth in Automotive and Industrial Semiconductors

The automotive sector remains a key growth vector:

- Electric vehicles (EVs) and advanced driver-assistance systems (ADAS) require more chips per vehicle, especially power management ICs, MCUs, and sensors.

- U.S. companies like Tesla, Qualcomm, and NXP (with U.S. design centers) are central to automotive semiconductor innovation.

- Industrial IoT and smart infrastructure projects boost demand for analog and mixed-signal chips.

By H2 2026, automotive is expected to be one of the fastest-growing end markets for U.S. chip suppliers.

5. Advances in Packaging and Heterogeneous Integration

As Moore’s Law slows, advanced packaging technologies (e.g., chiplets, 3D stacking, Foveros, Co-EMIB) become critical:

- U.S. companies lead in design and integration, with Intel, AMD, and NVIDIA adopting chiplet architectures.

- The U.S. government invests in R&D through programs like JUMP and the National Semiconductor Technology Center (NSTC).

- Domestic advanced packaging capacity is expanding to complement front-end fabrication.

This shift enhances performance and efficiency while reducing costs.

6. Workforce and R&D Investment

The U.S. semiconductor industry faces a talent shortage, but H2 2026 sees progress:

- Universities and community colleges expand semiconductor-focused programs with CHIPS Act funding.

- Partnerships between industry and academia (e.g., MIT.nano, Stanford, SUNY Poly) accelerate innovation in materials, design, and manufacturing.

- Venture capital continues to flow into U.S. semiconductor startups, especially in AI, quantum, and photonic chips.

This strengthens the long-term innovation pipeline.

7. Sustainability and Energy Efficiency

Environmental, social, and governance (ESG) concerns are rising:

- Chipmakers invest in energy-efficient fabs and water recycling technologies.

- Demand grows for low-power chips in mobile, IoT, and data centers to meet global sustainability targets.

- The U.S. leads in green semiconductor initiatives, including DOE-funded projects on energy-efficient computing.

Sustainability becomes a competitive differentiator.

Conclusion

By H2 2026, the U.S. semiconductor industry is on a strong growth trajectory, marked by expanded domestic manufacturing, leadership in AI and advanced design, and strategic positioning amid global tech competition. While challenges remain—such as supply chain vulnerabilities, talent gaps, and geopolitical risks—the convergence of policy support, technological innovation, and market demand positions U.S. chipmakers for sustained global leadership.

Common Pitfalls Sourcing US Chips (Quality, IP)

Sourcing semiconductor chips from the United States—while often associated with high performance and technological leadership—can present significant challenges related to both quality assurance and intellectual property (IP) protection. Companies venturing into this supply chain must be aware of these common pitfalls to mitigate risk and ensure long-term success.

Quality-Related Pitfalls

Inconsistent Lot-to-Lot Quality

Despite stringent manufacturing standards, variations in wafer fabrication processes can lead to inconsistencies across production lots. Relying on a single supplier without robust incoming inspection protocols may result in field failures or performance deviations, especially in mission-critical applications.

Counterfeit or Recycled Components

Even within US-distributed supply chains, counterfeit or remarketed chips can infiltrate through unauthorized distributors. These components may fail prematurely or underperform, undermining product reliability. Lack of traceability increases the risk, particularly when sourcing from third-party brokers.

Obsolescence and End-of-Life (EOL) Management

US semiconductor manufacturers frequently phase out older chip models to focus on newer technologies. Sourcing without monitoring product lifecycle status can lead to supply disruptions, costly redesigns, or forced reliance on unreliable aftermarket sources.

Lack of Transparent Testing and Qualification Data

Some suppliers may not fully disclose test procedures, environmental qualification data (e.g., AEC-Q100 for automotive), or reliability metrics. This opacity makes it difficult to assess suitability for specific applications, especially in aerospace, medical, or industrial environments.

IP-Related Pitfalls

Unlicensed or Infringing IP in Design or Firmware

Third-party IP blocks (e.g., SerDes, USB controllers, or DSP cores) embedded in US chips may be used without proper licensing or contain undisclosed IP conflicts. Importing or reselling products with such components can expose companies to costly litigation, especially in international markets.

Ambiguous IP Ownership in Custom or Semi-Custom Chips

When co-developing ASICs or FPGAs with US vendors, contracts may not clearly define IP ownership, usage rights, or design reuse limitations. This ambiguity can restrict future product development or lead to disputes over derivative works.

Export Control and Compliance Risks (e.g., EAR, ITAR)

US chips—especially those with dual-use or military-grade performance—may be subject to export regulations such as the Export Administration Regulations (EAR) or International Traffic in Arms Regulations (ITAR). Sourcing without verifying compliance can result in legal penalties, shipment seizures, or blacklisting.

Firmware and Software Licensing Traps

Many US chips include proprietary firmware or software development kits (SDKs) with restrictive licenses. Unintentional violations—such as reverse engineering, redistribution, or use in unauthorized applications—can trigger IP enforcement actions or loss of support.

Mitigation Strategies

To avoid these pitfalls, organizations should:

– Source exclusively through authorized distributors or direct OEM channels.

– Implement rigorous component testing and supply chain traceability.

– Conduct IP due diligence and legal review of licensing terms.

– Monitor export control classifications and maintain compliance documentation.

– Establish clear IP ownership clauses in development agreements.

Proactively addressing these quality and IP concerns ensures reliable sourcing of US chips while protecting against legal, operational, and reputational risks.

Logistics & Compliance Guide for US Chip

This guide outlines the key logistics and compliance considerations for the transportation, handling, and regulatory adherence related to semiconductor chips (referred to as “US Chip”) manufactured in or destined for the United States. Adherence to these standards ensures operational efficiency, legal compliance, and supply chain resilience.

Regulatory Compliance Framework

All shipments involving US Chip must comply with federal regulations enforced by agencies such as the Department of Commerce (BIS), U.S. Customs and Border Protection (CBP), and the Export Administration Regulations (EAR). Particular attention must be paid to Export Control Classification Numbers (ECCNs) and license requirements, especially for advanced semiconductors subject to restrictions under recent CHIPS Act provisions and foreign direct product rules.

Export and Import Documentation

Accurate and complete documentation is mandatory. Required documents include Commercial Invoices, Packing Lists, Shipper’s Export Declarations (SED), and, where applicable, Export Licenses or License Exceptions (e.g., LVS, TMP, or ENC). Importers must file Entry Records with CBP and ensure Harmonized Tariff Schedule (HTS) codes are correctly assigned—common classifications for semiconductor devices fall under HTS 8542.31 or 8542.39.

Restricted Party Screening

Prior to shipment, all parties in the transaction—including suppliers, customers, freight forwarders, and intermediaries—must be screened against U.S. government restricted party lists (e.g., Denied Persons List, Entity List, Unverified List). Automated screening tools integrated into logistics platforms are recommended to ensure real-time compliance.

Transportation and Handling Protocols

US Chip shipments require ESD (electrostatic discharge)-safe packaging and climate-controlled environments to prevent damage. Transport must adhere to IPC/JEDEC standards for moisture sensitivity levels (MSL). Use of tamper-evident seals and GPS-enabled tracking is advised for high-value or sensitive consignments.

Supply Chain Security

Compliance with the Customs-Trade Partnership Against Terrorism (C-TPAT) or equivalent supply chain security programs is strongly recommended. Facilities involved in handling US Chip must implement physical and cyber security measures to protect against theft, counterfeiting, and unauthorized access.

Recordkeeping and Audit Readiness

Maintain records of all export and import transactions for a minimum of five years. Records should include correspondence, licenses, screening logs, and shipment details. Regular internal audits should be conducted to verify compliance and prepare for potential government inspections.

CHIPS Act and Incentive Compliance

Entities receiving funding or incentives under the CHIPS and Science Act must comply with additional restrictions, including limitations on semiconductor manufacturing expansion in “foreign countries of concern” (e.g., China, Russia). Recipients must submit compliance certifications and maintain detailed operational records for federal oversight.

Environmental and Safety Regulations

Adhere to EPA and OSHA guidelines for the handling of materials used in chip packaging and logistics. Proper disposal of electronic waste and packaging materials must comply with federal and state environmental regulations. SDS (Safety Data Sheets) must be available for all hazardous materials in transit.

Conclusion

Effective logistics and compliance for US Chip require a proactive, integrated approach across legal, operational, and security domains. Continuous training, system automation, and close coordination with regulatory bodies and logistics partners are essential to ensure full compliance and support the integrity of the U.S. semiconductor ecosystem.

As global supply chain dynamics evolve and geopolitical tensions persist, overreliance on U.S. semiconductor manufacturers presents strategic risks for international businesses and national technology ecosystems. While U.S. chipmakers continue to lead in innovation, design, and advanced process nodes—companies like Intel, NVIDIA, and AMD remain pivotal in high-performance computing and AI—diversifying sourcing strategies is increasingly critical.

Relying solely on U.S. suppliers can expose companies to export controls, regulatory shifts, and capacity constraints, especially during periods of high demand or geopolitical instability. Therefore, a balanced sourcing approach that includes regional foundries (such as TSMC in Taiwan, Samsung in South Korea, and emerging domestic capabilities in Europe and Asia) enhances supply resilience and reduces dependency on any single nation.

In conclusion, while U.S. semiconductor manufacturers offer cutting-edge technology and strong R&D capabilities, businesses should adopt a multi-regional sourcing strategy. This approach mitigates risk, ensures continuity, and supports long-term competitiveness in an increasingly fragmented global tech landscape. Strategic partnerships, investment in alternative supply chains, and support for domestic semiconductor initiatives will be key to building a robust and resilient semiconductor ecosystem.