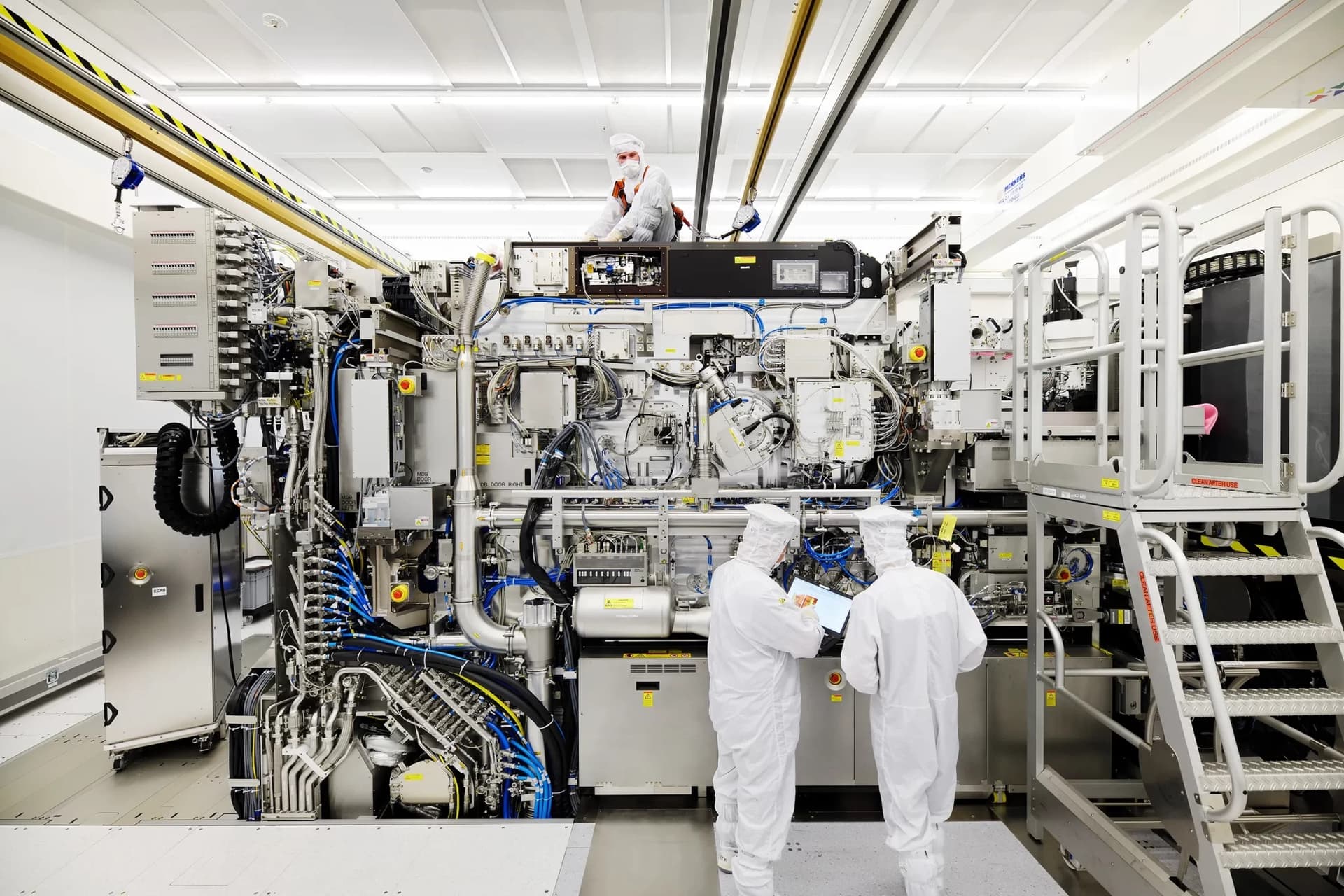

The U.S. semiconductor manufacturing industry continues to solidify its position as a global technology leader, driven by rising demand for advanced electronics, 5G infrastructure, artificial intelligence, and electric vehicles. According to Mordor Intelligence, the U.S. semiconductor market was valued at approximately USD 57.5 billion in 2023 and is projected to grow at a CAGR of over 4.5% from 2024 to 2029. This growth is further amplified by federal initiatives such as the CHIPS and Science Act, which aims to boost domestic production capacity and reduce reliance on overseas supply chains. With technological innovation accelerating across industries, domestic semiconductor manufacturers are scaling operations, investing heavily in R&D, and expanding fabrication facilities. As the backbone of modern computing and connectivity, U.S.-based semiconductor companies are not only shaping the future of technology but also reinforcing national competitiveness in a strategically vital sector. Below are the top nine U.S. semiconductor manufacturers leading this transformation.

Top 9 Us Semiconductor Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Us Semiconductor

H2 2026 Market Trends Analysis: U.S. Semiconductor Industry

As the second half of 2026 unfolds, the U.S. semiconductor industry is experiencing a pivotal transformation driven by technological innovation, geopolitical dynamics, and strategic policy initiatives. The sector is rebounding from earlier cyclical challenges and entering a phase of sustained growth, supported by strong demand in artificial intelligence (AI), advanced computing, automotive electrification, and national security applications.

1. AI and High-Performance Computing (HPC) Drive Demand

The most significant driver of semiconductor demand in H2 2026 is artificial intelligence. AI workloads—spanning generative AI, large language models (LLMs), and edge inference—are fueling unprecedented demand for advanced logic chips, particularly GPUs and AI accelerators. U.S. companies like NVIDIA, AMD, and Intel are leading the charge in supplying high-performance compute silicon, with domestic data centers and cloud providers ramping up AI infrastructure investments.

Chiplets and advanced packaging technologies (e.g., Intel’s Foveros, AMD’s 3D V-Cache) are becoming mainstream, enabling higher performance and energy efficiency. U.S. foundries and OSATs (Outsourced Semiconductor Assembly and Test) are expanding capabilities to meet this complex demand.

2. CHIPS and Science Act Fuels Domestic Manufacturing Growth

The U.S. government’s CHIPS and Science Act continues to deliver tangible results in H2 2026. Major semiconductor fabrication plants (fabs) funded under the Act—such as Intel’s $20 billion Ohio campus, TSMC’s Phoenix facility, and Samsung’s Taylor, Texas expansion—are beginning volume production. These investments are reducing reliance on offshore manufacturing and strengthening the domestic supply chain.

Notably, domestic production of leading-edge nodes (sub-3nm) is still limited, but the U.S. is rapidly closing the gap in mature and specialty nodes (28nm and above), which are critical for automotive, industrial, and defense applications.

3. Geopolitical Pressures and Supply Chain Resilience

U.S.-China technological decoupling remains a defining factor. Export controls on advanced semiconductor equipment and AI chips continue to tighten, pushing China toward self-reliance but also creating market opportunities for U.S. firms in allied markets (e.g., Japan, South Korea, EU, and India).

In response, U.S. semiconductor companies are diversifying supply chains through “friend-shoring” partnerships. Collaborations with Japan (in materials and equipment) and investment in Southeast Asia for backend operations are reducing exposure to regional risks.

4. Automotive and Industrial Sectors Stabilize

After years of volatility, the automotive semiconductor market has stabilized in H2 2026. Demand for electric vehicles (EVs), ADAS (Advanced Driver Assistance Systems), and in-vehicle AI is driving strong growth for power semiconductors (e.g., SiC and GaN) and microcontrollers. U.S. suppliers such as Wolfspeed (SiC), ON Semiconductor, and Texas Instruments are benefiting from long-term contracts with automakers.

The industrial and IoT sectors are also seeing renewed investment, particularly in smart manufacturing and energy-efficient systems, supporting demand for analog and mixed-signal chips.

5. Workforce and Innovation Challenges Persist

Despite strong market momentum, the U.S. semiconductor industry faces persistent challenges in talent acquisition and R&D scalability. The industry is investing heavily in university partnerships and workforce development programs to address the shortage of semiconductor engineers and technicians.

Additionally, competition for AI-optimized chip design talent is intensifying, with startups and hyperscalers competing aggressively for top designers.

6. Sustainability and Energy Efficiency as Competitive Differentiators

With increasing regulatory and investor focus on ESG (Environmental, Social, Governance), U.S. semiconductor firms are prioritizing energy-efficient chip design and sustainable manufacturing practices. Intel and GlobalFoundries have announced carbon-neutral fabs by 2030, while chip architects are optimizing for performance-per-watt in AI and mobile applications.

Conclusion:

H2 2026 marks a turning point for the U.S. semiconductor industry. Fueled by AI, supported by federal investment, and driven by strategic supply chain reconfiguration, the sector is regaining global leadership in innovation and manufacturing. While challenges remain in talent, geopolitics, and technology scaling, the overall outlook is strongly positive. The U.S. is poised to solidify its position as a hub for next-generation semiconductor development, particularly in AI, defense, and energy-efficient computing.

Common Pitfalls Sourcing US Semiconductors (Quality, IP)

Quality Assurance Challenges

Sourcing US semiconductors does not automatically guarantee superior quality. Buyers may face inconsistent quality control, especially when dealing with smaller or second-tier suppliers. Variability in manufacturing processes, lack of rigorous testing protocols, and supply chain disruptions can lead to defective or substandard components. Relying solely on a US origin label without verifying certifications (e.g., ISO 9001, IATF 16949) and conducting on-site audits increases the risk of receiving non-conforming products.

Intellectual Property (IP) Exposure Risks

Even when sourcing from US-based semiconductor manufacturers, IP protection is not foolproof. Poorly drafted contracts, ambiguous ownership clauses, or insufficient non-disclosure agreements (NDAs) can expose proprietary designs and sensitive technology. Additionally, reverse engineering risks persist if design files or samples are shared without adequate safeguards. Buyers must ensure robust legal frameworks are in place and verify the supplier’s track record in IP management.

Overreliance on “Made in USA” Claims

The label “US semiconductor” can be misleading. Many components may be packaged or tested in the US but contain foreign-made dies or use IP developed overseas. This hybrid sourcing increases complexity in ensuring true domestic content and compliance with regulations like the CHIPS Act or ITAR. Failing to trace the full bill of materials (BOM) may result in unintended dependency on foreign technology and compliance violations.

Supply Chain Transparency Gaps

US semiconductor suppliers may still rely on global sub-tier vendors for raw materials or specialized equipment. Lack of visibility into these lower tiers creates vulnerabilities, including exposure to counterfeit parts, forced labor concerns, or geopolitical risks. Without rigorous supply chain mapping and traceability systems, companies cannot fully ensure component integrity or regulatory compliance.

Inadequate Due Diligence on Emerging Suppliers

The push for domestic semiconductor production has led to a rise in new US-based startups. While promising, these suppliers may lack proven production scalability, long-term reliability data, or mature quality systems. Engaging without thorough technical evaluation and financial stability checks can lead to delivery delays, performance issues, or company insolvency, disrupting operations.

Logistics & Compliance Guide for U.S. Semiconductor Industry

Overview

The U.S. semiconductor industry operates within a highly regulated and strategically critical environment. Ensuring compliance with export controls, trade regulations, and supply chain security protocols is essential. This guide outlines key logistics and compliance considerations for companies involved in the design, manufacturing, and distribution of semiconductor technologies in the United States.

Export Controls and Licensing

Semiconductor products, especially advanced chips and related equipment, are subject to strict export control regulations administered by the Bureau of Industry and Security (BIS) under the Export Administration Regulations (EAR). Key compliance requirements include:

– Classification: Determine the Export Control Classification Number (ECCN) for each semiconductor product using the Commerce Control List (CCL).

– Licensing Requirements: Evaluate whether exports, reexports, or in-country transfers require a license based on destination, end-user, and end-use.

– Entity List Compliance: Screen all customers, suppliers, and partners against the BIS Entity List and other U.S. government restricted party lists.

– Advanced Computing & Supercomputing Rules: Adhere to specific restrictions on the export of advanced semiconductors and semiconductor manufacturing equipment to certain countries, particularly China, under recent BIS rulemakings (e.g., October 2022 and subsequent updates).

Sanctions and Restricted Parties Screening

U.S. semiconductor firms must implement robust screening processes to comply with Office of Foreign Assets Control (OFAC) sanctions:

– Conduct regular screening of all parties involved in transactions against the Specially Designated Nationals (SDN) List and other sanctions lists.

– Establish internal compliance programs that include automated screening tools and employee training.

– Maintain records of screening activities and compliance decisions for audit readiness.

Supply Chain Security and Resilience

Given the global nature of semiconductor supply chains, companies must ensure integrity and resilience:

– Foreign Direct Product Rule (FDP): Understand how U.S.-origin technology or software can trigger export licensing requirements even when products are manufactured abroad.

– Diversification: Develop strategies to mitigate risks from geopolitical disruptions, including supplier diversification and inventory buffering.

– Trusted Foundry Programs: Utilize vetted domestic or allied foundries when producing sensitive or defense-related semiconductor components.

Customs and Import Compliance

For imported semiconductor equipment and materials:

– Ensure accurate Harmonized Tariff Schedule (HTS) classification and valuation.

– Maintain records for Section 301 (China) tariffs and monitor exclusions or changes.

– Comply with Importer Security Filing (ISF) and Customs-Trade Partnership Against Terrorism (C-TPAT) best practices to expedite clearance.

Domestic Regulatory Considerations

- Defense Production Act (DPA): Be prepared for potential government prioritization of semiconductor production under DPA authorities.

- CHIPS and Science Act: Comply with funding requirements and guardrails for companies receiving federal incentives, including restrictions on expanding certain advanced manufacturing in China.

- Environmental Regulations: Adhere to EPA and OSHA standards related to chemical use, waste disposal, and workplace safety in fabrication facilities.

Cybersecurity and Data Protection

- Protect sensitive design data, intellectual property, and customer information through robust cybersecurity measures.

- Comply with frameworks such as NIST Cybersecurity Framework and CISA guidance for critical infrastructure sectors.

- Implement supply chain risk management for third-party software and hardware components (e.g., zero-trust architecture).

Recordkeeping and Audits

- Maintain comprehensive records of export transactions, license applications, denials, and compliance training for a minimum of five years.

- Conduct regular internal audits and risk assessments to identify and remediate compliance gaps.

- Prepare for potential BIS or OFAC audits with documented policies, procedures, and employee accountability.

Best Practices for Compliance

- Appoint a dedicated Export Compliance Officer.

- Implement an Export Management and Compliance Program (EMCP).

- Provide ongoing training for employees involved in logistics, sales, engineering, and procurement.

- Use automated compliance software for screening, classification, and license management.

Conclusion

The U.S. semiconductor industry plays a vital role in national security and economic competitiveness. By adhering to rigorous logistics and compliance standards, companies can mitigate legal and operational risks, support supply chain resilience, and ensure alignment with U.S. strategic objectives. Continuous monitoring of regulatory changes and proactive engagement with compliance frameworks are essential for long-term success.

Conclusion: Sourcing from U.S. Semiconductor Manufacturers

Sourcing semiconductors from U.S.-based manufacturers presents a strategic advantage in terms of supply chain resilience, technological innovation, and national security. With growing geopolitical uncertainties and increasing demand for reliable, high-quality components, domestic semiconductor production offers reduced lead times, enhanced intellectual property protection, and greater control over quality and compliance with regulatory standards.

Recent government initiatives, such as the CHIPS and Science Act, have revitalized the U.S. semiconductor industry by incentivizing onshore fabrication and fostering public-private partnerships. This support is accelerating investments in advanced manufacturing capabilities, positioning American foundries and IDMs (Integrated Device Manufacturers) to meet the growing demands of critical sectors, including defense, automotive, aerospace, and data infrastructure.

While challenges remain—such as higher production costs compared to offshore alternatives and ongoing capacity constraints—the long-term benefits of sourcing domestically are clear. Building strong partnerships with U.S. semiconductor manufacturers strengthens supply chain sovereignty, mitigates risks associated with global disruptions, and supports national economic and technological leadership.

In conclusion, prioritizing U.S.-based semiconductor sourcing is not only a prudent business decision but also a strategic imperative for ensuring technological competitiveness, supply chain security, and sustainable innovation in an increasingly digital and interconnected world.