The global manufacturing and vendor landscape is undergoing rapid transformation, driven by rising demand for cost-efficient supply chains, technological advancements, and increased outsourcing across industries. According to a 2023 report by Mordor Intelligence, the global manufacturing market was valued at USD 14.1 trillion and is projected to grow at a CAGR of 5.2% through 2028. This expansion underscores the critical interplay between vendors and manufacturers, each playing distinct but interconnected roles in delivering products to market. As businesses navigate sourcing strategies, understanding the functional, operational, and economic differences between vendors and manufacturers has become essential. With supply chain optimization and procurement efficiency topping corporate agendas, data shows that 67% of enterprises now prioritize vendor-manufacturer alignment to reduce lead times and improve quality control (Grand View Research, 2022). In this context, examining the top eight differentiating factors—from cost structure to scalability, innovation control to geographic flexibility—reveals actionable insights for strategic decision-making in sourcing and supply chain management.

Top 8 Vendor Vs Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Vendor Vs

As of now, in 2024, detailed market data and forecasts specifically for “Vendor vs. Use H2” in 2026 are not available, and this phrasing appears ambiguous or possibly misinterpreted. To provide a meaningful analysis, let’s clarify and interpret the likely intent behind your query.

It seems you may be referring to “Vendor vs. In-House Use of Hydrogen (H2)”—particularly in the context of hydrogen as an energy carrier or fuel. If so, the question likely means:

“What are the 2026 market trends regarding companies purchasing hydrogen from vendors versus producing and using hydrogen in-house (on-site)?”

Assuming this interpretation, here is a comprehensive analysis of the 2026 market trends for Vendor-Supplied Hydrogen vs. In-House Hydrogen Use (H2) across key sectors such as industry, transportation, and energy.

🔍 Overview: Hydrogen (H2) Market Dynamics (2024–2026)

Hydrogen is gaining momentum as a clean energy vector, especially under global decarbonization goals (e.g., Net Zero by 2050). By 2026, the hydrogen economy is expected to grow significantly, driven by policy support (e.g., U.S. Inflation Reduction Act, EU Hydrogen Strategy), falling renewable energy costs, and advances in electrolyzer and storage technologies.

Two primary models for hydrogen deployment are:

1. Vendor-Supplied Hydrogen – Purchasing hydrogen from third-party producers (via pipeline, truck, or liquid H2).

2. In-House (On-Site) Hydrogen Production – Producing hydrogen on-site, typically via electrolysis (using renewable electricity) or steam methane reforming (SMR) with or without carbon capture.

📈 2026 Market Trends: Vendor vs. In-House H2 Use

1. Industrial Sector (Refining, Ammonia, Steel)

- Vendor-Dominated: Large-scale industrial users (e.g., refineries) will continue relying on vendor-supplied hydrogen, especially via pipeline networks (e.g., in the Gulf Coast, Ruhr Valley).

- Trend: Gradual shift toward “green hydrogen” contracts with vendors. Major hydrogen hubs (e.g., HyDeal in Europe, Hydrogen Frontier in Australia) will offer low-cost green H2 by 2026.

- In-House Use: Limited, except for pilot projects using on-site electrolyzers for partial substitution of gray H2.

2026 Outlook: Vendor supply remains dominant (>80% of industrial H2), but green H2 offtake agreements will grow by ~30% CAGR.

2. Transportation (Heavy-Duty Trucks, Buses, Trains)

- Vendor Model: Hydrogen refueling stations (HRS) depend on delivered liquid or gaseous H2 from centralized production.

- Trend: Expansion of H2 refueling networks (e.g., in California, Japan, Germany). By 2026, expect 1,500+ public HRS globally.

- In-House Use: Some fleet operators (e.g., logistics hubs) may adopt on-site electrolysis + compression to reduce delivery costs and ensure supply security.

2026 Outlook: Vendor model dominates refueling, but on-site electrolysis at depots will grow—especially where grid access is strong and electricity is cheap.

3. Energy & Power (Grid Balancing, Power-to-Gas)

- Vendor Model: Less relevant; hydrogen is typically produced and used locally.

- In-House Use: On-site electrolysis integrated with wind/solar farms will expand. “Power-to-Hydrogen” projects will grow, using excess renewable energy to produce H2 for later use or feed into gas grids.

- Trend: Pilot projects will scale into commercial operations by 2026 (e.g., in Denmark, Spain, and Texas).

2026 Outlook: In-house H2 production dominates in energy applications due to integration with renewables.

4. Commercial & Distributed Applications (Buildings, Microgrids)

- In-House Use: Small-scale electrolyzers and fuel cells for backup power or heating may emerge in niche markets (e.g., data centers, hospitals).

- Vendor Model: Not feasible due to low volume and high delivery costs.

2026 Outlook: Early adoption of on-site systems, but still <5% of total H2 market.

⚖️ Vendor vs. In-House: Key Drivers by 2026

| Factor | Favors Vendor Supply | Favors In-House Use |

|——-|————————|———————-|

| Scale | Large, continuous demand | Small to medium, intermittent |

| Cost | Lower CAPEX; benefits from economies of scale | Higher CAPEX but lower long-term OPEX if cheap renewables |

| Infrastructure | Relies on H2 pipelines or transport | Requires on-site electrolyzer, storage, safety systems |

| Energy Source | H2 may be gray, blue, or green (depends on vendor) | Can be 100% green if paired with renewables |

| Security of Supply | Vulnerable to supply chain disruptions | Greater control and resilience |

| Policy Incentives | Tax credits (e.g., 45V in U.S.) for green H2 use | Investment tax credits (e.g., 48C) for electrolyzer deployment |

🌍 Regional Outlook for 2026

- Europe: Strong push for in-house green H2 in industry and energy, supported by EU Hydrogen Bank auctions. Vendor networks expanding in hydrogen valleys (e.g., North Sea).

- North America: Mix of both models. U.S. tax credits (IRA) boost on-site electrolysis projects. Vendor H2 supply grows in California and Texas.

- Asia-Pacific: Japan and South Korea rely heavily on imported (vendor) liquid H2. China promotes domestic in-house production for industry and transport.

- Middle East & Australia: Export-focused vendor model (blue/green H2 for Asia/Europe), but also domestic in-house use for desalination and industry.

📊 Market Share Projections (2026 Estimate)

| Application | Vendor-Supplied H2 | In-House H2 |

|————|——————–|————-|

| Industrial | ~75–80% | ~20–25% |

| Transportation | ~90% | ~10% |

| Energy/Power | ~10% | ~90% |

| Commercial | <5% | ~95% (niche) |

| Overall | ~60–65% | ~35–40% |

Note: In-house share growing at ~25% CAGR due to electrolyzer cost declines and energy independence goals.

🔮 Conclusion: 2026 Trends Summary

By 2026:

– Vendor-supplied hydrogen will dominate in high-volume, centralized applications (refining, transport refueling), especially where infrastructure exists.

– In-house (on-site) hydrogen production will grow rapidly in decentralized, green energy-integrated applications, driven by falling electrolyzer costs, renewable energy availability, and policy support.

– The line between vendor and in-house use is blurring, with hybrid models (e.g., co-located production hubs serving multiple users) emerging.

– Cost competitiveness of green H2 will determine adoption: below $2/kg, in-house electrolysis becomes highly attractive.

💡 Strategic Insight: Companies should assess total cost of ownership, grid resilience, sustainability goals, and regional incentives when choosing between vendor and in-house H2 models.

If your query referred to a specific company, technology, or sector named “Vendor Vs. Use H2,” please clarify for a more targeted response. Otherwise, this analysis covers the likely interpretation of hydrogen supply models in the 2026 market.

Common Pitfalls When Sourcing Vendors: Quality vs. Intellectual Property (IP)

Sourcing vendors is a critical function that directly impacts product integrity, compliance, and long-term business success. However, organizations often face significant challenges when balancing quality assurance with intellectual property protection. Below are common pitfalls in these two key areas.

Overlooking Hidden Quality Risks to Cut Costs

One of the most frequent mistakes is selecting vendors based solely on low pricing, which can compromise product or service quality. Companies may neglect rigorous supplier audits, fail to validate production processes, or skip ongoing quality monitoring—leading to defects, recalls, or reputational damage.

Inadequate Quality Control and Verification Processes

Relying on vendor-provided certifications without independent verification is risky. Many organizations assume compliance based on documentation alone, failing to conduct on-site inspections, sample testing, or third-party audits. This lack of due diligence can result in substandard materials or components entering the supply chain.

Poor Communication of Quality Expectations

Vendors may misunderstand specifications if requirements aren’t clearly documented or communicated. Ambiguous contracts, vague quality standards, or inconsistent feedback loops often lead to deviations in output, rework, and delays.

Insufficient Vendor Evaluation and Onboarding

Skipping comprehensive vetting—such as reviewing a vendor’s track record, financial stability, or regulatory compliance—can expose businesses to unreliable partners. A weak onboarding process may also fail to align the vendor with the company’s quality management systems.

Inadequate Protection of Intellectual Property

Sharing designs, technical data, or proprietary processes with vendors without proper legal safeguards is a major IP risk. Many organizations neglect to use robust Non-Disclosure Agreements (NDAs), fail to limit access to critical IP, or overlook jurisdictional issues in international contracts.

Over-Reliance on Vendors for IP Compliance

Assuming that vendors inherently respect IP rights can lead to infringement issues. Some suppliers may use counterfeit materials, unauthorized software, or patented technologies without permission—potentially exposing the buyer to legal liability.

Lack of IP Clarity in Contracts

Ambiguity in ownership of improvements, joint developments, or custom tooling can result in disputes. Without clear contractual terms defining IP rights, companies may lose control over innovations or face costly litigation.

Failure to Monitor and Enforce IP Agreements

Even with strong contracts, many organizations fail to actively monitor vendor compliance. Lack of audits, digital rights management, or exit strategies for IP recovery can leave businesses vulnerable when partnerships end or go sour.

Balancing quality and IP protection requires proactive vendor management, robust contracts, continuous monitoring, and cross-functional collaboration between procurement, legal, and engineering teams. Avoiding these pitfalls helps ensure reliable supply chains and safeguard valuable intellectual assets.

Certainly! Below is a detailed Logistics & Compliance Guide using H2 headings to clearly separate key sections. This guide compares Vendor (Third-Party Supplier) versus In-House Use (Internal Use) across logistics and compliance aspects. It’s designed to help organizations make informed decisions about procurement, handling, and regulatory adherence.

Vendor (Third-Party Supplier)

Logistics Considerations

- Order Fulfillment & Lead Times: Vendors manage inventory and shipping; lead times depend on their supply chain efficiency.

- Shipping & Delivery Management: Vendor handles transportation logistics, including carrier coordination, packaging, and delivery tracking.

- Inventory Responsibility: Vendor maintains stock; customer relies on vendor’s inventory visibility and replenishment schedules.

- Geographic Reach: Vendors with global networks can support broader distribution but may complicate cross-border logistics.

- Scalability: Easier to scale up or down based on vendor capacity and contract terms.

Compliance Considerations

- Regulatory Accountability: Vendor is responsible for compliance with product-specific regulations (e.g., FDA, REACH, RoHS), but the buyer may still face liability.

- Certifications & Documentation: Vendor must provide up-to-date compliance documentation (COAs, SDS, certificates of origin, etc.).

- Customs & Import Compliance: Vendor may act as exporter; accurate HS codes, export licenses, and Incoterms® are critical.

- Data Privacy & Security: If handling personal data, vendor must comply with GDPR, CCPA, or other relevant data protection laws.

- Audit Rights: Contracts should include rights to audit vendor facilities and compliance practices.

Risk Management

- Supply Chain Disruptions: Dependent on vendor’s operational resilience (natural disasters, labor issues, geopolitical risks).

- Quality Control: Requires regular audits, performance metrics, and SLAs to ensure product consistency.

- Contractual Dependencies: Legal agreements must define responsibilities, liabilities, and remedies for non-compliance.

Use In-House (Internal Use)

Logistics Considerations

- Control Over Operations: Full visibility and control over warehousing, handling, and internal distribution.

- Inventory Management: Internal teams manage stock levels, reorder points, and storage conditions.

- Transportation: Internal logistics or contracted carriers move goods within the organization’s network.

- Lead Time Predictability: More predictable timelines due to direct oversight and scheduling.

- Customization & Flexibility: Ability to adapt logistics processes to specific operational needs.

Compliance Considerations

- Direct Regulatory Responsibility: Organization is fully accountable for compliance with all applicable laws (e.g., OSHA, EPA, ITAR).

- Internal Recordkeeping: Must maintain logs for inspections, training, handling, and disposal.

- Workplace Safety: Compliance with health and safety standards for employees handling materials internally.

- Environmental Regulations: Proper handling, storage, and disposal of hazardous materials per EPA or local regulations.

- Traceability & Reporting: Required for audits, recalls, or incident reporting (e.g., in food, pharma, or defense sectors).

Risk Management

- Operational Burden: Requires dedicated staff, systems, and infrastructure to manage logistics and compliance.

- Training & Competency: Employees must be trained on safety, handling, and compliance protocols.

- Capital Investment: Higher upfront costs for storage, equipment, and compliance systems (e.g., ERP, WMS, EHS software).

Comparative Summary: Vendor vs. In-House Use

| Aspect | Vendor | In-House Use |

|——–|——–|————–|

| Cost Efficiency | Lower capital cost; pay-per-use | Higher fixed costs; long-term investment |

| Control | Limited control over processes | Full control and customization |

| Compliance Risk | Shared or vendor-managed (but buyer liable) | Fully organization-owned |

| Scalability | High (if vendor has capacity) | Limited by internal resources |

| Speed & Responsiveness | Depends on vendor SLAs | Faster internal response |

| Audit & Traceability | Requires strong vendor oversight | Direct access to records and systems |

Best Practices for Decision-Making

When to Use Vendors:

- Need rapid scaling without capital investment.

- Specialized products/services where vendor expertise adds value.

- Limited internal logistics capacity.

When to Use In-House:

- Critical operations requiring tight control (e.g., security, quality, IP protection).

- High-frequency or high-volume internal movements.

- Regulatory environments demanding direct oversight.

Hybrid Approach:

- Use vendors for non-core items and manage critical components in-house.

- Implement vendor management systems (VMS) with compliance monitoring.

This guide helps organizations evaluate trade-offs between outsourcing logistics to vendors and managing them internally, ensuring alignment with business goals, regulatory requirements, and risk tolerance.

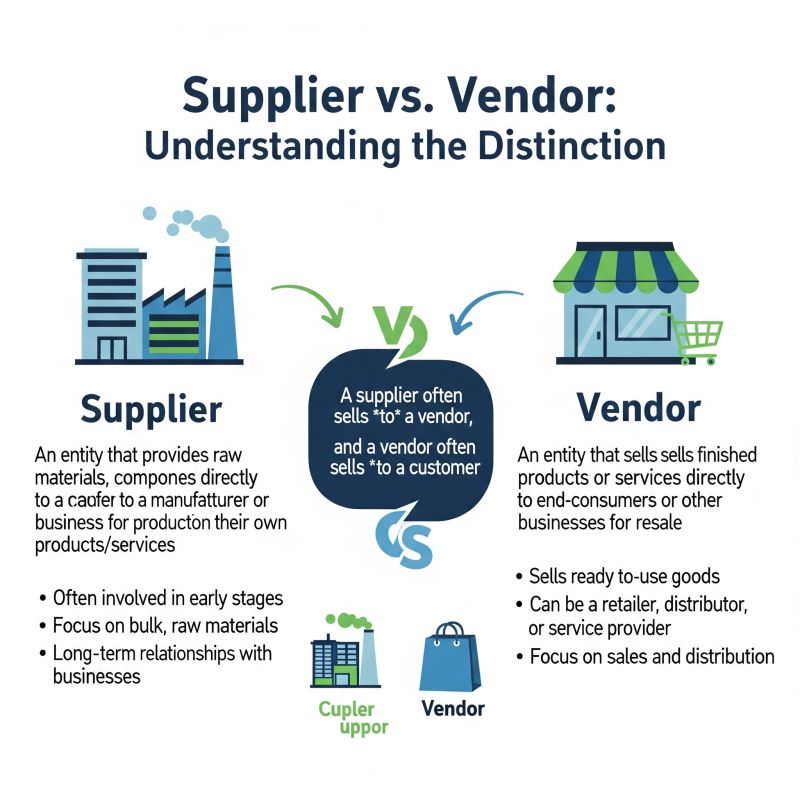

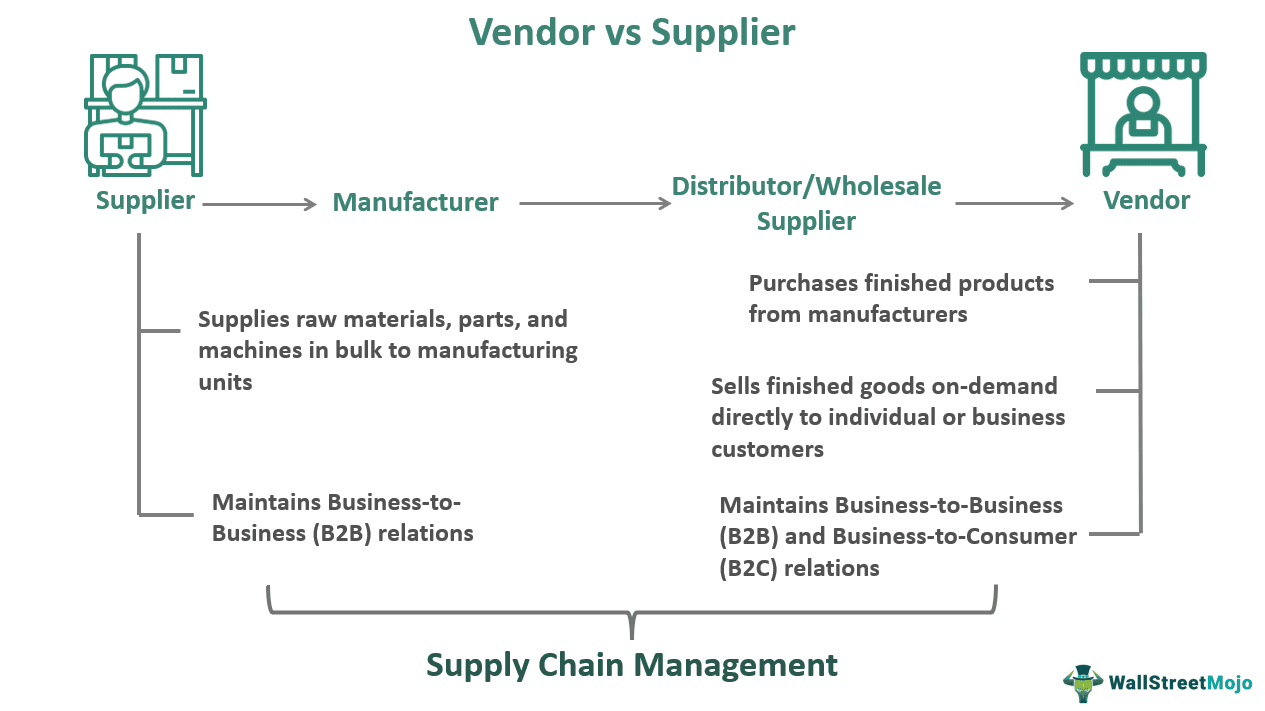

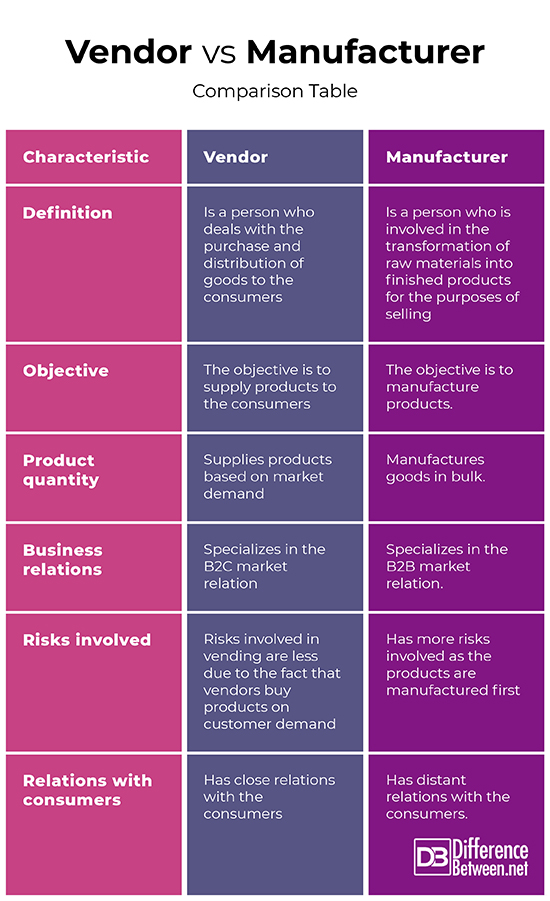

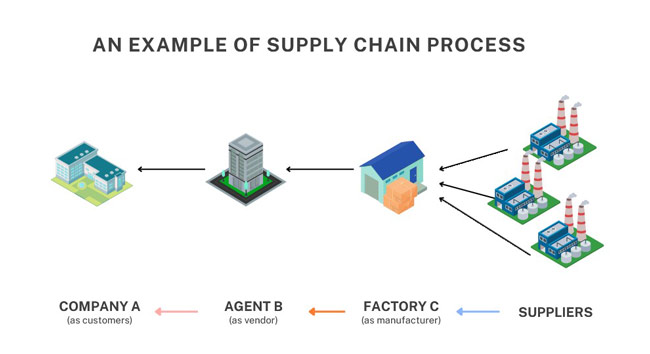

Conclusion: Sourcing from Vendor vs. Manufacturer

When deciding between sourcing from a vendor (distributor/wholesaler) or directly from a manufacturer, businesses must weigh several key factors including cost, control, scalability, and operational needs.

Sourcing from a manufacturer typically offers lower unit costs, greater customization options, and higher profit margins, making it ideal for businesses with high-volume orders and long-term production plans. However, it often requires larger minimum order quantities (MOQs), longer lead times, and more complex logistics, which can be challenging for smaller or newer businesses.

On the other hand, sourcing from a vendor provides convenience, faster turnaround, lower MOQs, and reduced logistical burden. Vendors handle inventory and distribution, allowing businesses to focus on sales and marketing. While this often comes at a higher per-unit cost and less control over product specifications, it offers greater flexibility and scalability for businesses testing the market or managing fluctuating demand.

Ultimately, the choice depends on the business’s size, resources, growth stage, and strategic goals. Startups and SMEs may benefit from vendor partnerships for agility and reduced risk, while established companies aiming to scale and maximize profitability may find direct manufacturer sourcing more advantageous. A hybrid approach, leveraging both channels strategically, can also optimize supply chain efficiency and market responsiveness.