The automotive financing landscape has shifted dramatically in recent years, with an increasing number of manufacturers leveraging 0% APR (annual percentage rate) financing offers to attract cost-conscious buyers. According to Mordor Intelligence, the global automotive finance market is projected to grow at a CAGR of over 7.2% from 2023 to 2028, driven by rising vehicle prices, extended loan tenures, and heightened competition among OEMs. This surge in demand for accessible financing has prompted major automakers to roll out aggressive 0% financing deals, particularly on new models, to stimulate sales and improve market share. As consumers seek to minimize borrowing costs amid fluctuating interest rates, manufacturers offering zero-interest incentives are gaining significant traction. Based on current market data and financing trends, the following seven car brands stand out for their consistent and competitive 0% financing programs—balancing affordability with strong residual values and consumer demand.

Top 7 What Car Are Offering 0 Financing Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for What Car Are Offering 0 Financing

H2: 2026 Market Trends for Cars Offering 0% Financing

As the automotive industry evolves heading into 2026, 0% financing offers remain a strategic tool used by manufacturers and dealerships to stimulate consumer demand amid shifting economic and technological landscapes. Here’s an analysis of key market trends influencing vehicles offering 0% financing in 2026:

1. Rising Interest Rates and Selective 0% Offers

Despite a volatile interest rate environment in the early 2020s, many automakers are expected to continue offering 0% financing selectively in 2026—particularly on specific trims, models with lower demand, or during promotional sales events. These offers are likely to be more targeted, reserved for buyers with excellent credit (typically FICO scores of 720+), and limited in loan term length (e.g., 36 to 60 months) to mitigate financial risk.

2. Electric Vehicle (EV) Incentives Driving 0% Financing Promotions

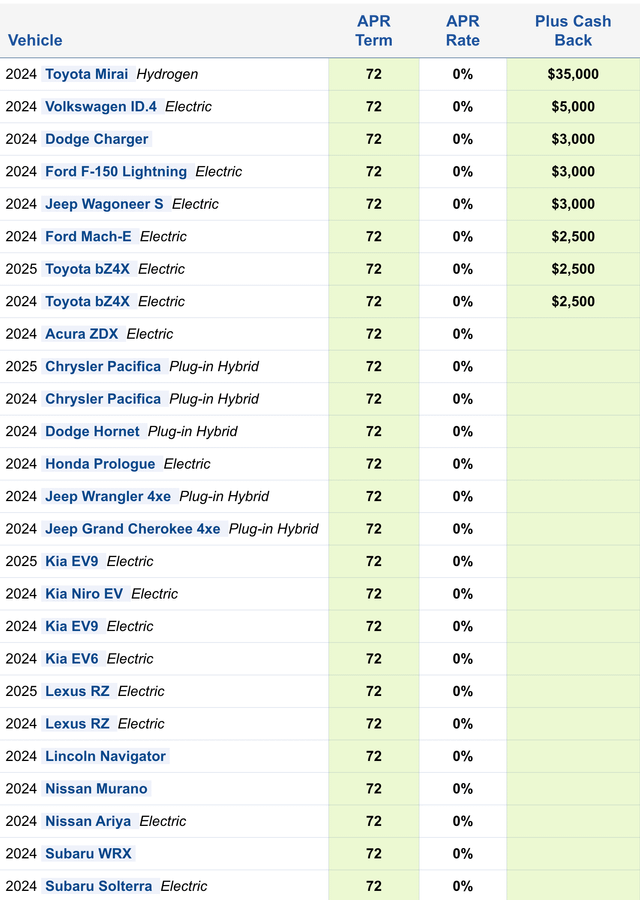

With governments pushing for EV adoption and automakers aiming to meet emissions targets, 0% financing is becoming a common incentive for electric models. In 2026, major brands like Chevrolet, Hyundai, and Kia are expected to bundle 0% APR deals with federal and state EV tax credits to lower the total cost of ownership and accelerate consumer adoption.

3. Increased Competition Among Automakers

As the market becomes saturated with new EVs and advanced internal combustion engine (ICE) models, automakers are leveraging 0% financing as a competitive differentiator. Brands such as Toyota, Honda, and Ford are likely to reintroduce or expand 0% financing on popular sedans and SUVs to maintain market share against disruptors like Tesla and Rivian, which traditionally avoid such promotions.

4. Tighter Eligibility and Shorter Promotional Windows

Due to inflationary pressures and tighter credit policies, 0% financing offers in 2026 are expected to come with stricter qualifications and shorter availability periods. Dealerships may limit these promotions to model-year clearance events or end-of-quarter sales, reducing long-term reliance on zero-interest deals.

5. Rise of Hybrid and Fuel-Efficient Models in Financing Deals

Beyond full EVs, automakers are increasingly promoting hybrid and fuel-efficient vehicles with 0% financing to appeal to cost-conscious buyers amid fluctuating fuel prices. Models like the Toyota RAV4 Hybrid, Honda CR-V Hybrid, and Ford Escape Hybrid are prime candidates for such incentives in 2026.

6. Digital Retailing and Transparent Financing

The growth of online car buying platforms has led to greater transparency in financing offers. By 2026, consumers can expect to see 0% financing options clearly advertised on manufacturer websites and third-party marketplaces, allowing for easier comparison shopping and faster decision-making.

Conclusion

In 2026, 0% financing will remain a powerful—but increasingly strategic—tool in the automotive sales arsenal. While economic factors may limit the breadth of these offers, they will continue to play a crucial role in driving sales of EVs, hybrids, and overstocked inventory. Buyers should monitor manufacturer incentives, maintain strong credit, and time their purchases around promotional events to fully benefit from these deals.

Common Pitfalls When Sourcing Cars with 0% Financing: Quality and Intellectual Property Concerns

While 0% financing deals can make purchasing a car more attractive, sourcing vehicles under such offers—especially from unfamiliar dealers, third-party brokers, or international markets—can expose buyers to significant risks related to vehicle quality and intellectual property (IP) issues. Understanding these pitfalls is crucial to making a safe and informed decision.

Hidden Quality Compromises in 0% Financing Deals

Many automakers and dealers use 0% financing as a marketing tool, but this often comes with strings attached that can impact the quality or value of the vehicle you receive:

-

Limited Vehicle Availability: 0% financing is typically restricted to base models or overstocked inventory. These vehicles may lack advanced safety features, modern infotainment systems, or premium materials, reducing overall quality and long-term satisfaction.

-

Higher MSRP or Hidden Fees: To offset the cost of interest-free loans, dealers may inflate the vehicle’s sticker price or add administrative, documentation, or “market adjustment” fees. This reduces the actual savings and may mean you’re paying a premium for a lower-quality product.

-

Shortened Warranty or Service Coverage: Some promotional deals pair 0% financing with reduced warranty terms or exclude complimentary maintenance. This increases long-term ownership costs and risks if quality issues arise post-purchase.

-

Used or Demonstrator Vehicles Marketed as New: Unethical sellers may present used, rental-return, or demonstrator models as new cars eligible for 0% financing. These vehicles may have hidden wear, prior damage, or diminished resale value.

-

Pressure to Purchase Without Proper Inspection: The urgency created by limited-time financing offers can lead buyers to skip essential quality checks, such as a pre-purchase inspection or CARFAX report, increasing the risk of buying a lemon.

Intellectual Property (IP) Risks in Sourcing Vehicles

While less commonly discussed, IP concerns can arise—particularly when sourcing vehicles from gray market importers, third-party modifiers, or overseas suppliers:

-

Counterfeit or Clone Vehicles: In some international markets, counterfeit cars that mimic popular brands (e.g., fake Land Rovers or Tesla lookalikes) are sold with falsified documentation. These vehicles infringe on trademarks and patents, making ownership legally risky and resale nearly impossible.

-

Unauthorized Modifications and Replicas: Some imported vehicles may include aftermarket parts or design elements that violate automakers’ IP rights—such as branded grilles, logos, or patented technology. Importing or selling such vehicles can lead to seizure or legal action.

-

Software and Firmware Violations: Modern cars contain proprietary software (e.g., infotainment systems, driver-assist features). Unauthorized duplication, tampering, or use of pirated software in reconditioned or imported vehicles can breach copyright and end-user license agreements.

-

Misrepresentation of Brand and Origin: Sellers may falsely advertise vehicles as genuine imports from authorized manufacturers, when in reality, they are rebranded or assembled using stolen designs. This misleads consumers and undermines brand integrity.

-

Lack of Support for IP-Infringing Components: If a vehicle contains infringing parts or software, the original manufacturer is not obligated to support, service, or update these systems, affecting reliability and safety.

How to Avoid These Pitfalls

- Always verify the vehicle’s VIN and run a comprehensive history report.

- Buy from authorized dealerships or certified importers.

- Read the full financing contract, including fine print about eligible models and附加 fees.

- Consult with a legal or automotive expert when sourcing from international or gray markets.

- Ensure all branding, software, and components are genuine and properly licensed.

By remaining vigilant about both quality and IP concerns, consumers can avoid costly mistakes and ensure their “0% financing” deal delivers real value without hidden risks.

Logistics & Compliance Guide for “What Car? Are Offering 0 Financing”

This guide outlines the key logistical considerations and compliance requirements when promoting or utilizing “0 financing” offers—such as those featured or advertised by What Car?—for automotive purchases in the UK. These guidelines ensure transparency, legal adherence, and customer trust.

Understanding 0 Financing Offers

“0 financing” typically refers to interest-free car finance deals where the borrower pays no interest on the loan amount over an agreed term. While this appears cost-free, it may come with specific conditions such as deposit requirements, credit checks, and eligibility criteria. What Car? often features these deals from manufacturers or finance providers, but they act as an information platform, not a finance provider.

Regulatory Framework and Compliance

All automotive financing promotions in the UK, including 0% APR offers, must comply with regulations enforced by the Financial Conduct Authority (FCA). Key compliance requirements include:

- Truthful Advertising: Promotions must not mislead consumers. Terms such as “0% financing” must be clearly explained with representative APR illustrations where applicable.

- Clear Disclosure of Terms: Advertisements must include representative examples, including the duration of the 0% offer, monthly payments, deposit required, total amount payable, and any fees.

- Credit Agreement Transparency: Finance providers must supply a clear Pre-Contract Credit Information Sheet (Pre-CCIS) and a credit agreement that outlines all terms before the customer commits.

- Responsible Lending: Lenders must conduct affordability and creditworthiness assessments. Promoting 0 financing without referencing eligibility criteria may breach FCA principles.

Logistics of Implementing 0 Financing Promotions

When dealerships or manufacturers work with platforms like What Car? to advertise 0 financing deals, logistical coordination is essential:

- Deal Validation: Ensure that live offers listed on What Car? match the terms available at participating dealers. Discrepancies can lead to customer dissatisfaction and compliance issues.

- Dealer Training: Sales teams must be trained on the exact terms of 0 financing offers, including duration, model availability, and customer eligibility.

- Stock Alignment: Ensure vehicle stock corresponds with advertised models eligible for 0% finance to avoid misleading customers.

- Lead Management: Coordinate with What Car? or other lead generators to ensure inquiries are routed efficiently and follow-up includes accurate financing details.

Consumer Communication and Disclosure

To remain compliant and build trust, clear communication is critical:

- Highlight Full Terms: Alongside “0 financing” messaging, clearly state the loan term (e.g., 36 months), required deposit, annual mileage limits (for PCP), and balloon payment (if applicable).

- Eligibility Statement: Include messaging such as “Subject to status. Terms and conditions apply. Finance provided by [Lender Name], a trading style of [Company], authorised and regulated by the FCA.”

- Avoid Misleading Claims: Do not imply that all customers qualify for 0% APR. Use language like “Representative 0% APR” and clarify that higher rates may apply based on credit history.

Monitoring and Audit Readiness

Regular audits help maintain compliance:

- Review Adverts: Periodically check all live 0 financing promotions (including those on What Car?) to ensure they meet FCA standards.

- Record Keeping: Maintain copies of all advertisements, credit agreements, and customer communications for at least five years.

- Compliance Training: Provide ongoing training for marketing and sales staff on FCA guidelines and advertising standards.

Conclusion

Promoting or advertising 0 financing deals—whether directly or through platforms like What Car?—requires strict adherence to FCA regulations and transparent customer communication. By following this logistics and compliance guide, automotive businesses can deliver attractive finance offers responsibly while minimizing legal and reputational risks.

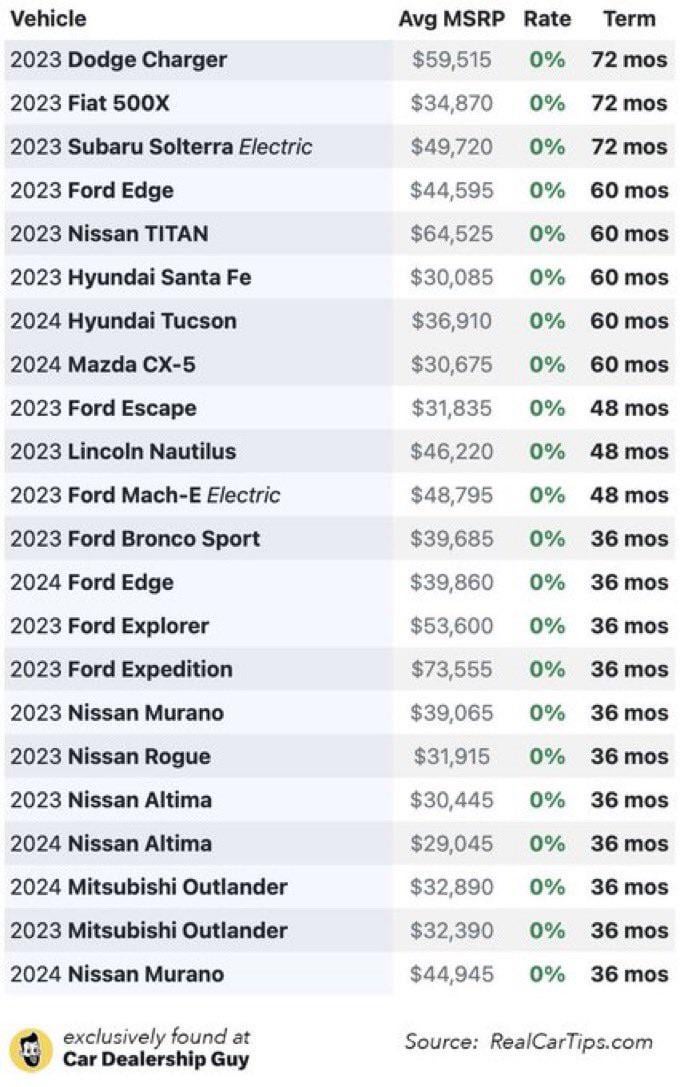

In conclusion, several car manufacturers currently offer 0% financing deals as part of their promotional incentives to attract buyers. These offers are typically reserved for customers with excellent credit and are often time-limited, varying by region and model availability. Major brands such as Honda, Toyota, Hyundai, Kia, and Mitsubishi frequently feature 0% APR financing on select new vehicles, especially during sales events or at the end of model years. It’s important for consumers to carefully review the terms, including loan duration, eligible models, and any associated fees or conditions. While 0% financing can significantly reduce overall costs, buyers should also consider alternative incentives—like cash rebates or lease specials—that might provide better value depending on their financial situation. To secure the best deal, it’s recommended to compare offers across manufacturers, negotiate with dealerships, and consult financing terms directly through official manufacturer websites or trusted financial institutions.