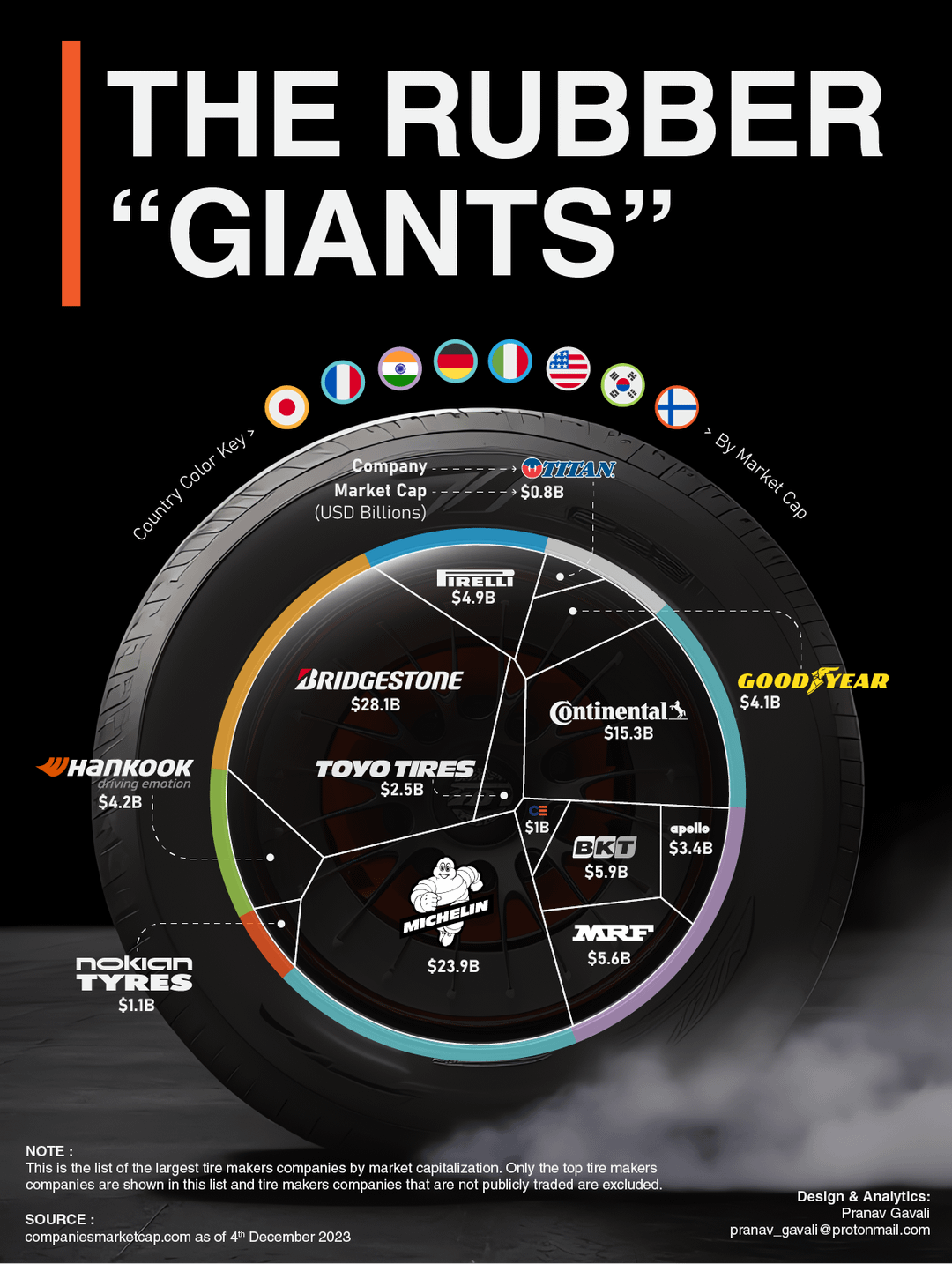

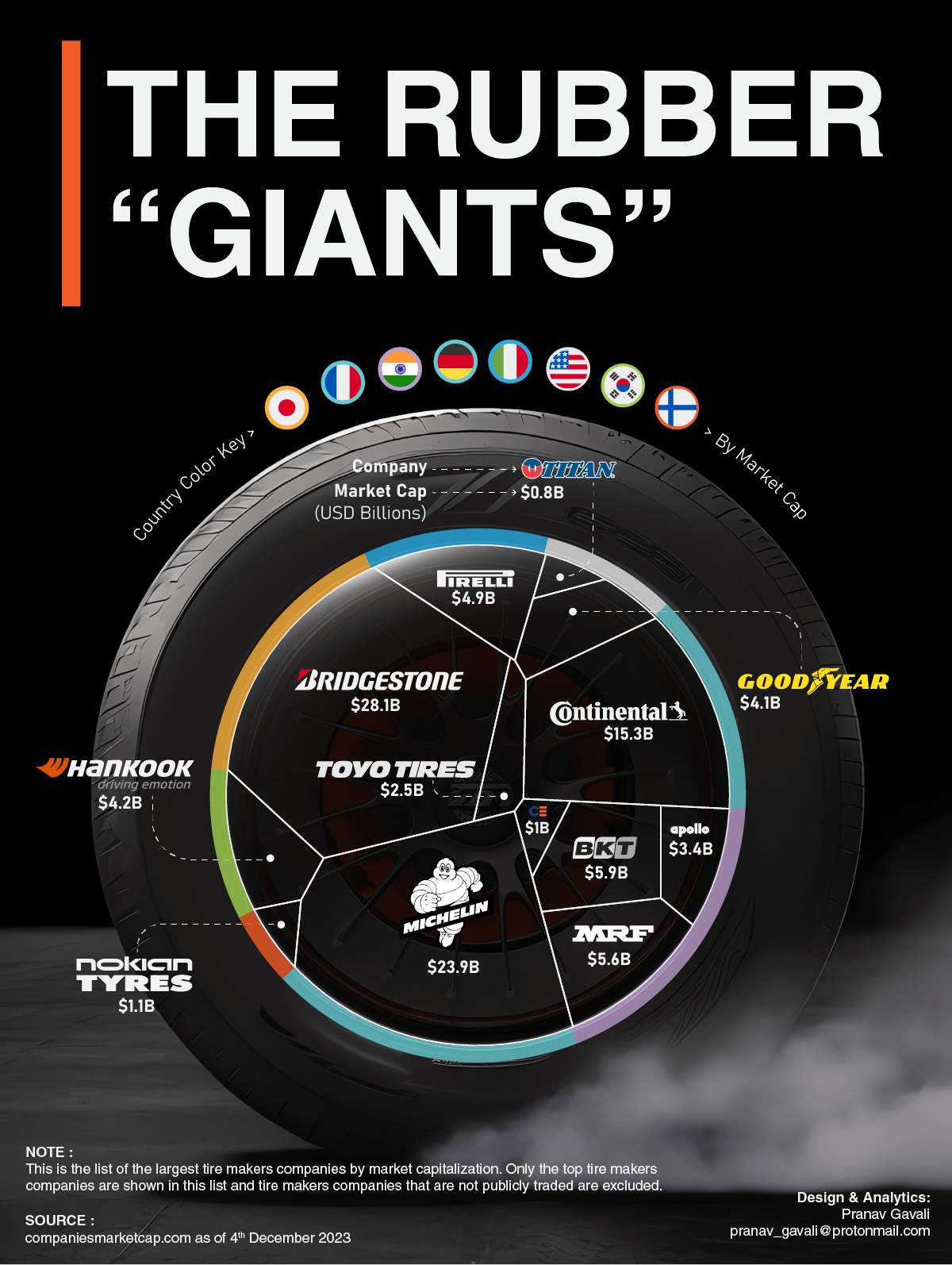

The global tire manufacturing industry has experienced steady growth over the past decade, driven by rising automotive production, increasing demand for replacement tires, and advancements in tire technology. According to a report by Grand View Research, the global tire market was valued at USD 183.6 billion in 2022 and is expected to expand at a compound annual growth rate (CAGR) of 4.2% from 2023 to 2030. Mordor Intelligence further projects that the market will surpass USD 234 billion by 2028, fueled by expanding vehicle ownership in emerging economies and growing demand for high-performance and fuel-efficient tires. In this evolving landscape, a select group of manufacturers dominate the sector through extensive production capacity, global distribution networks, and consistent innovation. The following list highlights the top 9 tire manufacturers worldwide, ranked by market share, revenue, and manufacturing scale, providing insight into the industry leaders shaping the future of mobility.

Top 9 Who Is The Largest Tire In The World Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Who Is The Largest Tire In The World

Who Is The Largest Tire Manufacturer in the World? 2026 Market Trends Analysis

Global Tire Market Overview in 2026

The global tire market is projected to reach approximately $280 billion by 2026, driven by increasing vehicle production, rising demand for electric vehicles (EVs), and advancements in tire technology. With a compound annual growth rate (CAGR) of 4.5% from 2021 to 2026, the industry is undergoing significant transformation. Sustainability, smart tires, and regional manufacturing shifts are key themes shaping competition among leading tire manufacturers. In this evolving landscape, one company continues to lead in terms of production volume, revenue, and global market share.

Bridgestone: Maintaining the Top Position

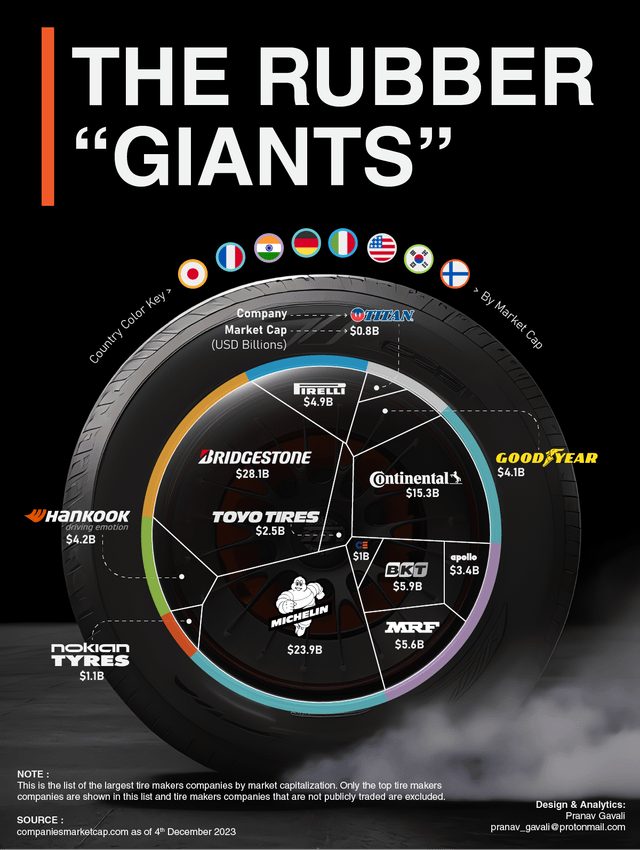

As of 2026, Bridgestone Corporation (Japan) remains the largest tire manufacturer in the world. The company holds an estimated 16% share of the global tire market, outpacing competitors in revenue and innovation. Bridgestone’s leadership is attributed to its strong presence in North America and Asia, diversified product portfolio, and strategic investments in sustainable tire development.

Bridgestone reported over $30 billion in tire-related revenue in 2025, with continued growth expected through 2026. The company has aggressively expanded its production of EV-specific tires—designed for higher load capacity, reduced rolling resistance, and noise reduction—catering to the surging electric vehicle market.

Key Competitors and Market Dynamics

While Bridgestone leads, it faces stiff competition from other global giants:

-

Michelin (France): A close second, Michelin has made significant strides in sustainability and digital mobility solutions. Its Vision concept tire and airless tire technology position it as an innovation leader. Michelin’s revenue in 2025 was approximately $28 billion, with a strong foothold in Europe and premium segments.

-

Goodyear (USA): Goodyear remains a dominant player in North America. Though third in global revenue, it has strengthened partnerships with EV manufacturers and invested heavily in retreading and circular economy initiatives.

-

Continental AG (Germany) and Yokohama Rubber (Japan) also hold significant market shares, particularly in OEM (original equipment manufacturer) supply chains.

Technological and Sustainability Trends Shaping Leadership

By 2026, tire leadership is not only measured by volume but also by innovation and environmental impact. Key trends influencing market position include:

- Sustainable Materials: Bridgestone and Michelin are leading in the use of bio-based and recycled materials, with goals to achieve 100% sustainable materials by 2050.

- Smart Tires: Integration of sensors for real-time pressure, temperature, and tread monitoring is becoming standard, especially in premium and commercial segments.

- Airless and Run-Flat Technologies: Bridgestone’s “Air-Free” concept and Michelin’s Uptis (puncture-proof tire) are expected to enter broader commercial use by 2026, particularly in fleet and urban mobility applications.

Regional Manufacturing Shifts

Asia-Pacific remains the largest production and consumption hub, with China and India driving demand. However, trade dynamics and supply chain resilience have prompted Bridgestone and others to expand manufacturing in North America and Eastern Europe to reduce dependency on single regions.

Conclusion: Bridgestone Leads in 2026

Despite intense competition, Bridgestone maintains its title as the world’s largest tire manufacturer in 2026 through a combination of global scale, technological innovation, and strategic sustainability initiatives. Its ability to adapt to electric mobility and circular economy trends ensures continued market leadership in a rapidly changing industry.

Common Pitfalls When Sourcing the Largest Tire in the World (Quality, IP)

When sourcing the largest tire in the world—typically referring to massive off-the-road (OTR) tires used in mining and heavy construction operations—companies face several critical challenges. Beyond logistics and cost, key pitfalls often revolve around quality assurance and intellectual property (IP) concerns. Understanding these risks is essential to avoid operational disruptions, legal complications, and financial losses.

Quality-Related Pitfalls

1. Compromised Materials and Manufacturing Standards

One of the most significant risks when sourcing large tires is encountering substandard materials or manufacturing processes. Some suppliers—especially those from less-regulated markets—may use inferior rubber compounds, weaker steel belts, or inconsistent curing methods. These flaws can lead to premature wear, blowouts, or catastrophic failures in extreme operating conditions.

Best Practice: Always verify compliance with international standards such as ISO 9001 and request third-party testing certifications. Prioritize suppliers with a proven track record in mining or heavy equipment sectors.

2. Lack of Performance Validation in Real-World Conditions

Large tires are engineered for specific loads, speeds, and terrains. A common mistake is assuming that a tire labeled as “largest” is suitable for all heavy-duty applications. Without field testing or performance data, buyers risk acquiring tires unsuitable for their operational environment.

Best Practice: Request case studies, load/speed ratings, and validation reports from real-world installations. Engage in pilot trials before full-scale procurement.

3. Inadequate After-Sales Support and Warranty Coverage

Some suppliers may offer competitive pricing but lack comprehensive service networks. Given the size and cost of these tires, timely repair, retreading, and replacement services are crucial.

Best Practice: Evaluate the supplier’s global service footprint, warranty terms, and availability of technical support engineers.

Intellectual Property (IP) Pitfalls

1. Risk of Sourcing Counterfeit or Reverse-Engineered Tires

The largest tires are often proprietary designs from industry leaders like Michelin, Bridgestone, or Caterpillar (through their OTR partnerships). Unauthorized manufacturers may produce look-alike tires that mimic branding or design, infringing on patents and trademarks.

Best Practice: Only source through authorized distributors or directly from OEMs. Conduct due diligence on suppliers to verify authenticity and avoid gray market products.

2. Patent and Design Infringement Exposure

Using or importing tires that violate existing patents—even unknowingly—can expose your company to legal liability. This is particularly relevant when sourcing from regions with lax IP enforcement.

Best Practice: Perform IP clearance checks and require suppliers to provide documentation confirming their designs do not infringe on existing patents.

3. Limited Recourse in Case of IP Disputes

If a tire supplier is found to be using stolen or copied technology, your organization may face supply chain disruptions, forced recalls, or reputational damage—even if you were not directly involved in the infringement.

Best Practice: Include indemnification clauses in procurement contracts, requiring suppliers to assume liability for any IP violations.

Conclusion

Sourcing the world’s largest tires demands more than just attention to size and price. Quality assurance and intellectual property integrity are critical factors that, if overlooked, can lead to safety hazards, legal exposure, and long-term operational inefficiencies. Partnering with reputable, transparent suppliers and conducting rigorous due diligence are essential steps in mitigating these risks.

Who Is The Largest Tire Manufacturer In The World: Logistics & Compliance Guide

When identifying the largest tire manufacturer in the world, Bridgestone Corporation currently holds the title, followed closely by Michelin and Goodyear. As global leaders in tire production, these companies manage complex international logistics and stringent compliance requirements. This guide outlines key logistics and compliance considerations relevant to operating at the scale of the world’s largest tire manufacturers.

Global Supply Chain & Logistics Management

1. Raw Material Sourcing

Tire manufacturing relies heavily on raw materials such as natural rubber, synthetic rubber, steel, carbon black, and various chemical compounds. The largest manufacturers maintain long-term contracts with suppliers across multiple continents, including Southeast Asia (natural rubber), the Middle East (oil-based synthetics), and Latin America.

- Logistics Challenge: Ensuring timely delivery amid fluctuating commodity prices and geopolitical risks.

- Best Practice: Diversify sourcing regions and use digital procurement platforms to monitor supply chain resilience.

2. Manufacturing & Distribution Network

Bridgestone, Michelin, and Goodyear operate dozens of manufacturing plants globally, often located near key markets to reduce transportation costs and lead times.

- Key Regions: North America, Europe, Asia-Pacific, and emerging markets in Africa and South America.

- Logistics Strategy: Implement just-in-time (JIT) inventory systems and regional distribution centers to optimize delivery cycles.

3. Transportation Modalities

Tires are bulky and heavy, requiring efficient multimodal logistics:

- Ocean Freight: Primary mode for international shipments; containers are optimized for volume.

- Rail & Trucking: Used for regional and domestic distribution.

-

Air Freight: Limited to urgent or high-value specialty tires (e.g., aircraft or motorsport tires).

-

Compliance Note: Adherence to International Maritime Organization (IMO) regulations and container weight safety standards (e.g., SOLAS Verified Gross Mass).

Regulatory Compliance & Standards

1. Environmental Regulations

Tire manufacturers must comply with environmental laws governing emissions, waste disposal, and sustainable sourcing.

- Examples:

- EU REACH and RoHS regulations on hazardous substances.

- U.S. EPA standards for air and water emissions.

-

ISO 14001 certification for environmental management systems.

-

Sustainability Initiatives: Leading companies invest in retreading, recycling programs, and bio-based materials to meet ESG (Environmental, Social, and Governance) goals.

2. Safety & Product Standards

Tires must meet strict performance and safety standards in every market they serve.

- Key Certifications:

- DOT (U.S. Department of Transportation) – FMVSS 109, 119, 139 standards.

- ECE (Europe) – E-mark certification.

-

INMETRO (Brazil), CCC (China), and other national standards.

-

Logistics Impact: Non-compliant shipments may be rejected at customs, causing delays and financial losses.

3. Trade Compliance & Tariffs

Global tire trade is subject to tariffs, anti-dumping duties, and import restrictions.

- Example: The U.S. has imposed anti-dumping duties on certain Chinese tire imports.

- Best Practice: Maintain accurate Harmonized System (HS) code classification (e.g., 4011 for new pneumatic tires) and ensure proper documentation (commercial invoices, certificates of origin, packing lists).

Reverse Logistics & End-of-Life Tire Management

1. Tire Recycling & Disposal

Environmental regulations require proper handling of end-of-life tires (ELTs). The largest manufacturers often participate in or lead tire stewardship programs.

- Compliance Requirement: Adhere to EU ELT Directive, U.S. state-level scrap tire regulations, and extended producer responsibility (EPR) laws.

- Logistics Solution: Partner with certified recycling facilities and use track-and-trace systems for ELT shipments.

2. Retreading & Reuse

Commercial and truck tire manufacturers emphasize retreading to extend product life and reduce waste.

- Regulatory Note: Retreaded tires must meet the same safety standards as new tires in regulated markets.

Digitalization & Compliance Monitoring

Leading tire manufacturers use advanced logistics technologies:

- Track-and-Trace Systems: GPS and RFID tags for real-time shipment monitoring.

- Blockchain for Provenance: Ensures ethical sourcing of natural rubber (e.g., conflict-free zones).

- Automated Compliance Software: Tools that flag regulatory changes, manage documentation, and ensure audit readiness.

Conclusion

The largest tire manufacturers like Bridgestone maintain global leadership not only through production volume but also via sophisticated logistics networks and rigorous compliance frameworks. Success in this industry requires a strategic balance of supply chain efficiency, regulatory adherence, and sustainability. Companies aiming to compete at this level must invest in technology, risk management, and cross-border regulatory expertise to navigate the complex global tire market.

As of the most recent data, Bridgestone Corporation is widely recognized as the largest tire manufacturer in the world by revenue. Headquartered in Tokyo, Japan, Bridgestone leads the global market through its extensive product range, strong presence in both consumer and commercial tire segments, and operations in numerous countries. Other major competitors include Michelin (France) and Goodyear (United States), which rank closely behind in terms of production volume and global market share. However, Bridgestone consistently holds the top position based on annual sales, manufacturing capacity, and international reach.