Introduction: Navigating the Global Market for wholesale banking

In the rapidly evolving landscape of global finance, navigating the complexities of wholesale banking can be a daunting challenge for international B2B buyers. As companies expand their operations across borders, the need for sophisticated financial solutions becomes paramount. This guide addresses the key hurdles in sourcing wholesale banking services, providing a roadmap for understanding various types of offerings, their applications, and the intricacies involved in supplier vetting and cost analysis.

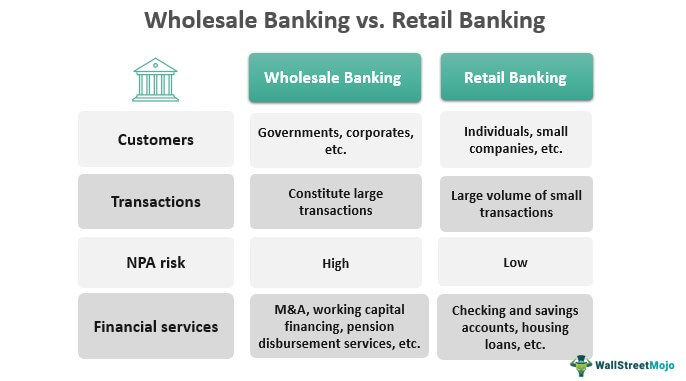

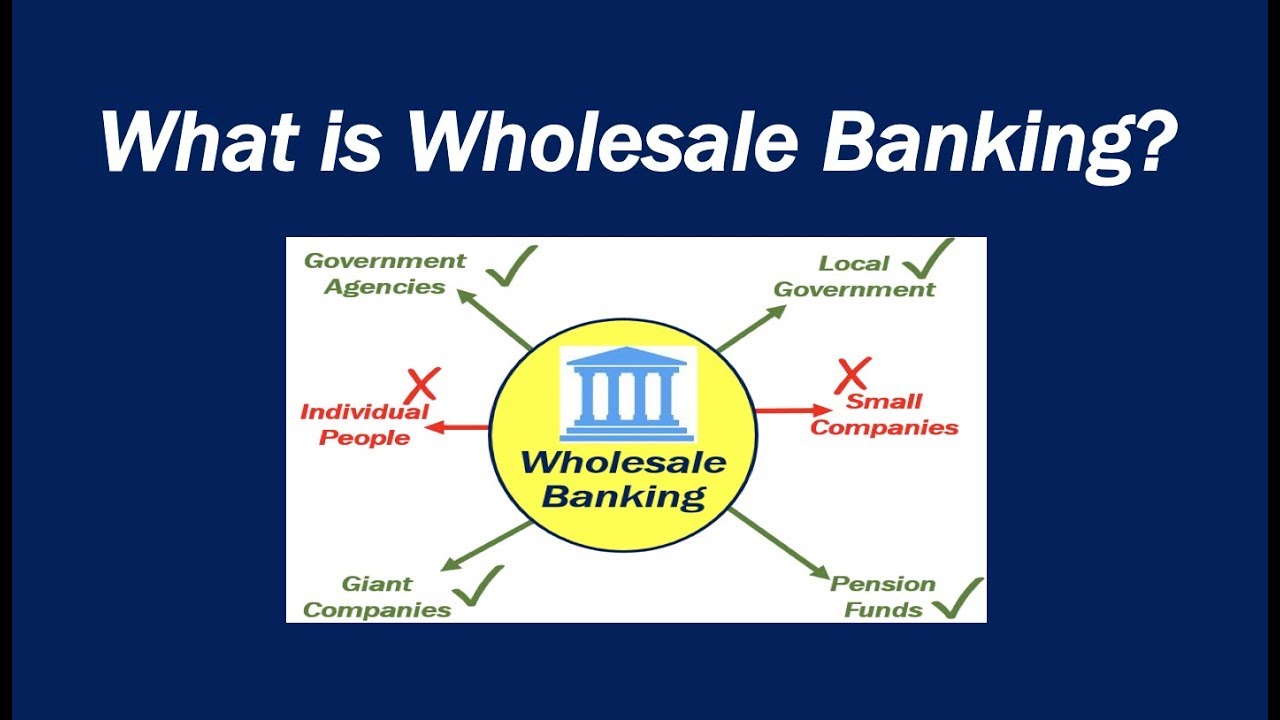

Wholesale banking encompasses a range of tailored services designed for large institutions, including corporations, government agencies, and financial entities. From mergers and acquisitions to trade financing and currency conversion, these services are critical for businesses looking to optimize their capital and enhance operational efficiency. This comprehensive guide will equip B2B buyers from Africa, South America, the Middle East, and Europe—such as Brazil and Saudi Arabia—with the insights needed to make informed decisions in their sourcing endeavors.

By delving into the nuances of wholesale banking, this resource empowers stakeholders to identify the right financial partners, understand market dynamics, and leverage global opportunities. As you embark on this journey, you’ll gain actionable knowledge that not only mitigates risks but also positions your organization for sustainable growth in the competitive international marketplace.

Top 10 Wholesale Banking Manufacturers & Suppliers List

1. Investopedia – Wholesale Banking Services

Domain: investopedia.com

Registered: 1999 (26 years)

Introduction: Wholesale banking services include currency conversion, working capital financing, large trade transactions, mergers and acquisitions, consultancy, and underwriting. It caters to large clients such as corporations, government agencies, and other financial institutions, providing tailored financial solutions and complex transactions.

2. HDFC Bank – Wholesale Banking Services

Domain: hdfcbank.com

Registered: 1997 (28 years)

Introduction: Wholesale Banking Services offered by HDFC Bank include: 1. Large Corporates 2. Commercial Credit Cards 3. Government & Institutional Business 4. Government Sector Services 5. Agricultural Lending 6. Cash Management 7. Investment Banking Services such as project appraisal, structured finance, M&A, and corporate advisory services. Additional services include pension payment, Jeevan Pramaan, and acc…

3. Reddit – Wholesale Banking Services

Domain: reddit.com

Registered: 2005 (20 years)

Introduction: Wholesale banking refers to the services that banks offer to large clients such as corporations, government agencies, investment firms, and other financial institutions. It focuses on providing complex and large-scale financial services, including loans, asset management, and currency exchanges. Examples include financing for construction projects, commercial real estate development, and infrastru…

4. Oliver Wyman – 2024 Wholesale Banking Outlook

Domain: oliverwyman.com

Registered: 1996 (29 years)

Introduction: The 2024 edition of the annual wholesale banking industry outlook, titled “Extending Credit: The Evolving Role of Wholesale Banks In Credit Markets,” explores the transformation of wholesale banks in credit markets, driven by regulatory pressure, product innovation, and new competitors. Key insights include a projected increase in industry-wide return on equity (RoE) to approximately 14% by 2027, …

5. Lumen Alta – Retail Banking Solutions

Domain: lumenalta.com

Registered: 2023 (2 years)

Introduction: Retail banking offers services such as checking accounts, savings accounts, personal loans, and payment solutions tailored for individuals and small-scale clients. It emphasizes user-friendly features, flexible loan terms, personalized advice, attractive savings options, and enhanced security measures. Wholesale banking provides services for large-scale entities, including substantial lending oper…

6. ING Wholesale Banking – Tailored Financial Solutions

Domain: ingwb.com

Registered: 2015 (10 years)

Introduction: ING Wholesale Banking offers a range of services including tailored financial solutions, sustainability support, and digital banking channels like InsideBusiness for managing financial flows. They serve corporate clients and financial institutions in over 35 countries, providing local and global insights along with sector expertise. ING is recognized for its leadership in sustainability, being inc…

7. Bain – Wholesale Banking Insights

Domain: bain.com

Registered: 1994 (31 years)

Introduction: Wholesale banks will likely face slower growth over the next few years, while heavy spending on IT puts pressure on short-term profitability.

8. Finance Unlocked – Comprehensive Learning Solutions

Domain: financeunlocked.com

Registered: 2017 (8 years)

Introduction: Our platform offers a variety of learning solutions including: 1. Expert-led content with over 1,000 on-demand video modules. 2. Learning analytics to track progress. 3. Interactive learning features such as video hotspots and knowledge check-ins. 4. Testing and certification options for CPD/CPE credits. 5. Managed learning solutions for organizations. 6. Tailored solutions for enterprises, teams,…

Understanding wholesale banking Types and Variations

| Type Name | Key Distinguishing Features | Primary B2B Applications | Brief Pros & Cons for Buyers |

|---|---|---|---|

| Corporate Banking | Tailored financial solutions for large corporations | Working capital financing, corporate loans | Pros: Customized services; Cons: Higher complexity |

| Investment Banking | Focus on capital raising and advisory services | Mergers & acquisitions, IPOs | Pros: Expert advice; Cons: Higher fees |

| Trade Finance | Financing solutions for international trade transactions | Import/export financing, letters of credit | Pros: Risk mitigation; Cons: Regulatory complexities |

| Treasury Management | Management of liquidity and financial risk | Cash flow optimization, investment strategies | Pros: Enhanced financial efficiency; Cons: Requires expertise |

| Real Estate Financing | Specialized loans for property development and investment | Commercial real estate projects, property acquisitions | Pros: Large capital access; Cons: Market volatility risks |

What Are the Characteristics of Corporate Banking in Wholesale Banking?

Corporate banking provides customized financial services to large corporations. This includes working capital financing, commercial loans, and treasury services tailored to a company’s specific needs. B2B buyers in this sector should consider the complexity of the financial products offered, as they often require a deep understanding of the buyer’s business model and cash flow needs. The personalized service can lead to more favorable terms, but buyers must be prepared for a potentially lengthy approval process.

How Does Investment Banking Differ Within Wholesale Banking?

Investment banking specializes in capital markets and financial advisory services, such as mergers and acquisitions (M&A) and initial public offerings (IPOs). For B2B entities, engaging an investment bank can provide invaluable insights into market conditions and strategic opportunities. However, the costs associated with these services can be significant, and companies must weigh the potential return on investment against these fees. This type of banking is best suited for businesses looking to expand through acquisition or seeking to raise substantial capital.

What Role Does Trade Finance Play in Wholesale Banking?

Trade finance is essential for businesses involved in international trade, providing the necessary funding and risk mitigation tools for import and export transactions. Common applications include letters of credit and export financing, which help manage the complexities of cross-border transactions. B2B buyers should consider the regulatory requirements and documentation needed, as these can add layers of complexity. Nevertheless, effective trade finance solutions can significantly enhance a company’s ability to engage in global markets.

Why Is Treasury Management Important for Businesses?

Treasury management focuses on optimizing a company’s liquidity, cash flow, and financial risk exposure. This service is crucial for large corporations looking to streamline their operations and maximize returns on excess cash. B2B buyers must assess their organization’s financial management capabilities and the expertise required to implement effective treasury strategies. While the benefits include improved financial efficiency and risk management, the necessity for specialized knowledge can be a barrier for some organizations.

How Does Real Estate Financing Fit Into Wholesale Banking?

Real estate financing is tailored for large-scale property investments and developments. This type of wholesale banking offers specialized loans for commercial projects, making it ideal for real estate developers and investors. B2B buyers should evaluate the terms of financing, including interest rates and repayment schedules, against the potential risks associated with property markets. While the access to substantial capital can facilitate growth, market volatility can pose risks that need to be carefully managed.

Key Industrial Applications of wholesale banking

| Industry/Sector | Specific Application of wholesale banking | Value/Benefit for the Business | Key Sourcing Considerations for this Application |

|---|---|---|---|

| Manufacturing | Supply Chain Financing | Improved cash flow management and operational efficiency | Evaluate the bank’s expertise in manufacturing financing and flexibility in terms. |

| Real Estate | Project Financing for Large Developments | Access to significant capital for large-scale projects | Assess the bank’s experience with real estate projects and their local market knowledge. |

| Energy & Utilities | Structured Finance for Renewable Projects | Facilitation of capital-intensive green initiatives | Look for banks with a strong track record in energy financing and sustainability practices. |

| Government & Public Sector | Treasury Management and Government Bonds | Enhanced liquidity management and investment strategies | Consider banks’ relationships with government entities and their expertise in public finance. |

| Trade & Export | Trade Finance Solutions | Mitigation of risks associated with cross-border transactions | Investigate the bank’s global network and expertise in trade finance solutions. |

How Is Wholesale Banking Utilized in the Manufacturing Sector?

In the manufacturing sector, wholesale banking provides essential supply chain financing that helps businesses manage their cash flow more effectively. By offering tailored financing solutions, banks can enable manufacturers to purchase raw materials and manage operational costs without straining their working capital. For international buyers, particularly in emerging markets like Africa and South America, it’s crucial to partner with banks that understand local supply chain dynamics and can offer flexible terms to accommodate fluctuating production schedules.

What Are the Financing Needs in Real Estate Development?

Real estate developers often rely on wholesale banking for project financing, especially for large-scale developments that require substantial capital investment. Wholesale banks can provide customized financing structures that align with the unique cash flow patterns of real estate projects, including construction loans and bridge financing. Buyers should prioritize banks with extensive knowledge of local real estate markets and a history of successfully financing similar projects to ensure they receive the best support and advice.

How Can Renewable Energy Projects Benefit from Structured Finance?

In the energy and utilities sector, wholesale banking plays a critical role in financing renewable energy projects through structured finance solutions. These banks facilitate access to the significant capital necessary for initiating large-scale green initiatives, helping businesses navigate the complexities of funding and regulatory requirements. For international buyers, particularly in regions like the Middle East, sourcing banks with specialized expertise in energy financing and a commitment to sustainability can lead to successful project execution.

What Treasury Management Solutions Are Available for Government Entities?

Government and public sector entities utilize wholesale banking for treasury management services, which include managing liquidity, investments, and government bonds. These services are vital for ensuring that public funds are effectively managed and invested, maximizing returns while minimizing risks. Buyers in this sector should seek banks with a proven track record in public finance and a deep understanding of governmental financial regulations and requirements.

How Does Trade Finance Support International Trade?

Wholesale banking provides trade finance solutions that are essential for businesses engaged in international trade. These services help mitigate risks associated with cross-border transactions, such as currency fluctuations and payment defaults. For B2B buyers, particularly in developing regions, it is important to partner with banks that have a strong global network and expertise in trade finance to facilitate smoother transactions and enhance their competitive edge in international markets.

A stock image related to wholesale banking.

3 Common User Pain Points for ‘wholesale banking’ & Their Solutions

Scenario 1: Navigating Complex Regulatory Environments in Wholesale Banking

The Problem: B2B buyers in wholesale banking often face the daunting challenge of navigating complex and varying regulatory environments across different countries. This is particularly true for international corporations and financial institutions looking to engage in cross-border transactions. In regions like Africa and South America, the regulatory landscape can be particularly opaque, leading to confusion and potential compliance risks. Companies may struggle with understanding local laws, tax implications, and compliance requirements, which can delay transactions and result in financial penalties.

The Solution: To effectively navigate these regulatory challenges, B2B buyers should prioritize establishing partnerships with wholesale banks that have a strong local presence and expertise in the target markets. It’s crucial to conduct thorough due diligence on potential banking partners to ensure they have robust compliance frameworks and a proven track record in the regions of interest. Additionally, leveraging technology platforms that offer regulatory updates and insights can significantly aid in staying informed about changing regulations. Creating a dedicated compliance team or engaging local legal experts can also provide the necessary guidance to ensure adherence to all regulatory requirements, thereby mitigating risks and facilitating smoother transactions.

Scenario 2: Managing Currency Risk in International Transactions

The Problem: For businesses involved in international trade, managing currency risk is a significant pain point. Fluctuations in exchange rates can adversely affect profit margins, especially when large sums are involved in wholesale banking transactions. B2B buyers in regions such as the Middle East and Europe often experience volatility that can lead to unexpected costs, impacting their financial planning and operational budgets.

The Solution: To effectively manage currency risk, B2B buyers should utilize financial instruments such as forward contracts and options offered by wholesale banks. These tools allow businesses to lock in exchange rates for future transactions, providing greater predictability in financial forecasting. Additionally, buyers should consider implementing a comprehensive foreign exchange strategy that includes regular assessments of currency exposure and the establishment of risk management policies. Engaging with a wholesale bank that specializes in foreign exchange services can provide tailored solutions that align with the company’s specific risk profile and transaction needs, ensuring that they are well-positioned to navigate currency fluctuations effectively.

Scenario 3: Streamlining Payment Processes for Large Transactions

The Problem: Wholesale banking often involves large-scale transactions that can be cumbersome and time-consuming to process. B2B buyers, particularly in sectors such as manufacturing and export, face challenges with slow payment processes, which can lead to cash flow issues and strained supplier relationships. Delays in payments can result in missed opportunities and increased operational costs, especially in competitive markets.

The Solution: To streamline payment processes, B2B buyers should explore automated payment solutions provided by wholesale banks, which can facilitate faster and more efficient transactions. Implementing electronic funds transfer (EFT) systems and leveraging real-time payment platforms can significantly reduce transaction times. Additionally, establishing clear communication channels with banking partners and suppliers regarding payment terms can help set expectations and minimize delays. Regularly reviewing and optimizing payment workflows can also uncover inefficiencies, allowing businesses to adopt best practices that enhance overall transaction speed and reliability. Engaging with a wholesale bank that offers tailored payment solutions and technological innovations can further enhance operational efficiency, ensuring timely and seamless financial transactions.

Strategic Material Selection Guide for wholesale banking

What Are the Key Materials Used in Wholesale Banking Operations?

In the context of wholesale banking, the selection of materials is critical for ensuring the efficiency and reliability of financial transactions and services. The materials used in various banking applications must meet specific performance criteria to handle the complexities of large-scale financial operations. Below are analyses of four common materials used in wholesale banking, focusing on their properties, advantages, disadvantages, and considerations for international B2B buyers.

Steel: The Backbone of Banking Infrastructure

Key Properties: Steel is known for its high tensile strength and durability. It can withstand significant pressure and is resistant to corrosion when treated properly.

Pros & Cons: Steel’s durability makes it ideal for constructing secure banking facilities and vaults. However, its weight can complicate manufacturing and installation processes. Additionally, while steel can be cost-effective, the price can fluctuate based on market conditions.

Impact on Application: Steel is commonly used in the construction of bank branches and ATMs, where security is paramount. Its compatibility with various construction techniques makes it a versatile choice.

Considerations for International Buyers: Buyers from regions like Africa and South America should be aware of local steel standards and certifications, such as ASTM or ISO, to ensure compliance with safety regulations.

Aluminum: Lightweight and Versatile

Key Properties: Aluminum is lightweight, resistant to corrosion, and has good thermal conductivity. It can be easily molded into complex shapes, making it suitable for various applications.

Pros & Cons: The lightweight nature of aluminum reduces transportation costs, but it may not provide the same level of security as steel. While generally more affordable than steel, aluminum can be less durable in high-stress environments.

Impact on Application: Aluminum is often used in the production of banking equipment, such as kiosks and signage, where ease of installation and aesthetic appeal are important.

Considerations for International Buyers: Buyers should consider local regulations regarding aluminum usage and ensure that the material meets relevant standards, such as DIN or JIS, especially in regions with stringent building codes.

Copper: Essential for Electrical Applications

Key Properties: Copper is an excellent conductor of electricity and has good corrosion resistance. It can handle high temperatures, making it suitable for electrical applications.

Pros & Cons: The primary advantage of copper is its conductivity, which is essential for banking technology infrastructure. However, copper is more expensive than other materials, and its susceptibility to theft can pose security risks.

Impact on Application: Copper is widely used in wiring and electronic components within banking systems, ensuring reliable communication and transaction processing.

Considerations for International Buyers: Buyers must ensure that copper products comply with international electrical standards and local regulations, particularly in regions like the Middle East, where electrical safety codes are stringent.

Plastic Composites: Modern and Cost-Effective

Key Properties: Plastic composites are lightweight, resistant to corrosion, and can be molded into various shapes. They are often used for protective casings and non-structural components.

Pros & Cons: The primary advantage of plastic composites is their cost-effectiveness and ease of manufacturing. However, they may lack the durability and security features of metals, making them less suitable for high-risk applications.

Impact on Application: Plastic composites are commonly used in banking software interfaces and non-critical hardware, such as card readers and terminals.

Considerations for International Buyers: When sourcing plastic materials, buyers should be aware of compliance with environmental regulations, particularly in Europe, where standards like REACH are enforced.

Summary Table of Material Selection for Wholesale Banking

| Material | Typical Use Case for wholesale banking | Key Advantage | Key Disadvantage/Limitation | Relative Cost (Low/Med/High) |

|---|---|---|---|---|

| Steel | Construction of bank branches and vaults | High durability and security | Heavy, complicates installation | Medium |

| Aluminum | Banking equipment and signage | Lightweight and versatile | Less secure than steel | Medium |

| Copper | Wiring and electronic components | Excellent electrical conductivity | High cost and theft risk | High |

| Plastic Composites | Non-critical hardware and interfaces | Cost-effective and easy to manufacture | Less durable than metals | Low |

This strategic material selection guide provides a comprehensive overview for international B2B buyers in wholesale banking, emphasizing the importance of material properties, application suitability, and compliance considerations across different regions.

A stock image related to wholesale banking.

In-depth Look: Manufacturing Processes and Quality Assurance for wholesale banking

What Are the Key Manufacturing Processes in Wholesale Banking?

In wholesale banking, the term “manufacturing” may not refer to physical goods but rather to the production of financial services and products. The processes involved can be viewed as stages of service creation that require meticulous planning and execution. Here are the main stages:

How Is Material Prepared in Wholesale Banking Services?

The first stage involves the preparation of materials, which in the context of wholesale banking includes gathering data, client information, and market research. Financial institutions must assess the needs of their corporate clients, government agencies, or other financial institutions. This involves analyzing client profiles, understanding their financial requirements, and collecting relevant market data to tailor solutions effectively.

What Techniques Are Used for Forming Financial Products?

Once the necessary information has been gathered, the next step is forming financial products and services. This includes structuring loans, designing investment portfolios, or creating custom derivatives. Key techniques at this stage often involve:

- Risk Assessment Models: Utilizing advanced analytics and risk modeling to identify potential risks associated with financial products.

- Financial Engineering: Crafting tailored financial solutions that meet the specific needs of clients, often involving complex calculations and simulations.

- Regulatory Compliance Checks: Ensuring that all products adhere to local and international regulations, which can vary significantly across regions, particularly for B2B clients from diverse markets like Africa, South America, and the Middle East.

How Is Assembly Achieved in Financial Service Delivery?

The assembly stage in wholesale banking is about integrating the various components of financial services into a cohesive offering. This includes the collaboration of multiple departments within a bank, such as risk management, compliance, and customer service, to ensure seamless service delivery. Techniques employed here include:

- Cross-Departmental Collaboration: Engaging teams from different departments to ensure that the financial product is viable and meets client expectations.

- Technology Integration: Utilizing sophisticated financial software to streamline processes, manage client relationships, and track transactions efficiently.

What Are the Finishing Touches in Service Delivery?

The finishing stage involves finalizing the service offering and preparing it for delivery to the client. This could involve the creation of final documents, contracts, and necessary compliance paperwork. Techniques include:

- Quality Review Processes: Conducting internal reviews to ensure that all products meet quality standards and align with client expectations.

- Final Compliance Checks: Ensuring all regulatory requirements have been met before service delivery.

What Quality Assurance Practices Are Essential in Wholesale Banking?

Quality assurance (QA) in wholesale banking is crucial to maintain service integrity, client trust, and regulatory compliance. Here are the key aspects of QA relevant to B2B buyers:

Which International Standards Should Be Followed?

Wholesale banks often adhere to international standards such as ISO 9001, which focuses on quality management systems, ensuring that the bank’s processes consistently meet client requirements. Other relevant certifications may include:

- ISO 27001: Focused on information security management, crucial for protecting sensitive client data.

- ISO 31000: Provides guidelines on risk management, ensuring that banks can identify and mitigate risks associated with their services.

What Are the Industry-Specific Quality Control Standards?

In addition to general international standards, wholesale banks may also follow industry-specific standards such as:

- Basel III: Regulatory framework focusing on bank capital adequacy, stress testing, and market liquidity risk.

- API (Application Programming Interface) Standards: Ensuring compatibility and security in data exchange between banking systems.

How Are Quality Control Checkpoints Established?

Quality control checkpoints are essential to ensure that the services provided meet both internal and external standards. Key checkpoints include:

- Incoming Quality Control (IQC): Assessing the quality of raw data and materials before they are utilized in service delivery.

- In-Process Quality Control (IPQC): Continuous monitoring during the service creation process to identify and rectify issues in real-time.

- Final Quality Control (FQC): Conducting thorough checks before the service is delivered to the client to ensure compliance with all standards.

What Common Testing Methods Are Used in Wholesale Banking?

Testing methods in wholesale banking can vary, but common practices include:

- Simulation Testing: Running simulations to assess how financial products will perform under various market conditions.

- Compliance Audits: Regular reviews to ensure all operations align with regulatory requirements and internal policies.

- Client Feedback Mechanisms: Collecting feedback from clients post-delivery to identify areas for improvement.

How Can B2B Buyers Verify Supplier Quality Control?

For B2B buyers, particularly those from diverse regions such as Africa, South America, the Middle East, and Europe, verifying supplier quality control is crucial. Here are effective strategies:

What Auditing Processes Should Be Implemented?

Conducting thorough audits of potential suppliers is essential. B2B buyers should look for:

- Third-Party Audits: Engaging independent auditors to assess the quality control processes of suppliers.

- Internal Quality Reports: Reviewing internal documentation and reports that outline quality assurance practices and results.

How Can Quality Reports Inform Decision-Making?

Requesting detailed quality reports from suppliers can provide insights into their QA processes. These reports should include:

- Quality Metrics: Key performance indicators (KPIs) that demonstrate the effectiveness of quality assurance measures.

- Incident Reports: Documentation of any quality issues and how they were resolved, offering transparency into the supplier’s operational integrity.

What Are the Quality Control Nuances for International B2B Buyers?

For international B2B buyers, understanding the nuances of quality control in wholesale banking is vital. Considerations include:

- Cultural Differences: Being aware of how quality standards may vary by region and adapting expectations accordingly.

- Regulatory Variations: Navigating different regulatory environments and ensuring that suppliers comply with local laws and international standards.

By understanding the manufacturing processes and quality assurance practices in wholesale banking, B2B buyers can make informed decisions that align with their organizational needs and risk management strategies. This comprehensive approach not only enhances service quality but also builds long-term partnerships between banks and their institutional clients.

Practical Sourcing Guide: A Step-by-Step Checklist for ‘wholesale banking’

In the dynamic landscape of wholesale banking, B2B buyers must navigate complex financial services tailored to their organizational needs. This practical sourcing guide is designed to help you effectively procure wholesale banking services that align with your strategic objectives. By following this step-by-step checklist, you can ensure that you choose the right banking partner for your large-scale financial transactions.

Step 1: Identify Your Banking Needs

Before engaging with potential wholesale banking providers, clearly define your specific financial requirements. Are you seeking services for mergers and acquisitions, trade financing, or currency conversion? Understanding your needs helps you communicate effectively with banks and enables them to tailor their offerings to suit your objectives.

Step 2: Research Potential Banking Partners

Conduct thorough research to identify banks that specialize in wholesale banking services. Look for institutions with a strong reputation in your industry and geographic region. Consider factors such as their experience, range of services, and client testimonials.

- Key Actions:

- Review online resources, industry reports, and banking directories.

- Attend financial services conferences to meet potential partners.

Step 3: Evaluate Service Offerings and Expertise

Once you have a shortlist of banks, assess their service offerings in detail. Look for providers that offer customized financial solutions and have expertise in your specific sector.

- Considerations:

- Do they have a dedicated team for your industry?

- What innovative products do they offer that could benefit your operations?

Step 4: Verify Regulatory Compliance and Certifications

Ensure that the banks you consider comply with local and international regulatory standards. This step is crucial to protect your organization from legal and financial risks.

- Verification Actions:

- Check for licenses and certifications from relevant financial authorities.

- Review their compliance history and any regulatory issues they may have faced.

Step 5: Request Proposals and Compare Terms

Solicit proposals from multiple banks to compare their offerings, fees, and terms. This step allows you to evaluate the cost-effectiveness of their services and understand the value they provide.

- What to Compare:

- Interest rates, fees, and terms of service.

- Flexibility in terms of loan amounts and repayment schedules.

Step 6: Conduct Due Diligence on Financial Stability

Assess the financial health of potential banking partners. A bank’s stability is vital for ensuring that they can support your long-term financial needs.

- Key Metrics to Review:

- Credit ratings from agencies like Moody’s or Standard & Poor’s.

- Financial statements to analyze profitability and liquidity ratios.

Step 7: Establish Clear Communication Channels

Once you select a banking partner, establish clear communication protocols. This ensures that both parties understand expectations and can quickly address any issues that arise.

- Action Points:

- Designate key contacts for ongoing communication.

- Set regular meetings to review performance and address any concerns.

By following this checklist, you can make informed decisions when sourcing wholesale banking services, ensuring that you choose a partner capable of supporting your organization’s financial goals in a complex global environment.

Comprehensive Cost and Pricing Analysis for wholesale banking Sourcing

What Are the Key Cost Components in Wholesale Banking?

In wholesale banking, understanding the cost structure is essential for making informed sourcing decisions. The primary cost components include:

-

Materials: While wholesale banking does not deal with physical materials in the traditional sense, it involves financial instruments and services that can be considered as ‘intangible materials.’ These might include software systems for transaction processing, risk assessment tools, and compliance mechanisms.

-

Labor: The expertise of financial analysts, investment bankers, and consultants constitutes a significant portion of labor costs. Skilled professionals are required to execute complex transactions, conduct market research, and provide tailored financial advice.

-

Manufacturing Overhead: Although wholesale banking is not a manufacturing industry, overhead can encompass technology costs, infrastructure maintenance, and administrative expenses necessary to support banking operations.

-

Tooling: In this context, tooling refers to the technology and platforms used for transaction processing, data analytics, and risk management. Investments in these tools can vary widely based on the sophistication of services offered.

-

Quality Control (QC): Ensuring compliance with regulatory standards and maintaining the integrity of financial transactions adds another layer of cost. Banks often invest heavily in QC measures to mitigate risks associated with fraud and financial mismanagement.

-

Logistics: For wholesale banking, logistics involves the seamless execution of transactions across borders, which may incur costs related to currency conversion, international regulations, and cross-border compliance.

-

Margin: The profit margin in wholesale banking can be influenced by competition, service complexity, and client relationships. Typically, margins are lower due to the high volume and scale of transactions.

How Do Price Influencers Affect Wholesale Banking Costs?

Several factors can influence pricing in wholesale banking:

-

Volume/MOQ (Minimum Order Quantity): Larger transactions often lead to better pricing due to economies of scale. Banks might offer tiered pricing models where clients receive discounts based on transaction volume.

-

Specifications/Customization: Customized services tailored to specific client needs can lead to higher costs. Clients should be aware that bespoke solutions often come with premium pricing.

-

Materials and Quality/Certifications: The integrity of financial instruments and the certifications of financial products can impact costs. Higher quality and reputable certifications often command higher prices due to the perceived lower risk.

-

Supplier Factors: The choice of banking partner can significantly influence costs. Established institutions with strong reputations may charge more due to their reliability and service quality.

-

Incoterms: For cross-border transactions, understanding Incoterms is crucial as they define the responsibilities of buyers and sellers in terms of costs and risks, potentially impacting the overall pricing structure.

What Are Effective Buyer Tips for Negotiating Costs in Wholesale Banking?

For international B2B buyers, particularly from regions like Africa, South America, the Middle East, and Europe, the following strategies can enhance cost-efficiency:

-

Negotiate Terms: Always engage in negotiations to explore potential discounts, especially for high-volume transactions. Building a long-term relationship with the bank can also lead to more favorable terms.

-

Consider Total Cost of Ownership (TCO): When evaluating offers, consider the TCO, which includes not only the initial costs but also ongoing fees, compliance expenses, and potential risks associated with the service.

-

Understand Pricing Nuances: Be aware that pricing models can vary significantly across regions. For instance, banks in emerging markets may have different pricing strategies compared to those in developed economies, influenced by local market dynamics.

-

Seek Transparency: Request clear pricing breakdowns from banks to identify any hidden fees or costs associated with services. Transparency is vital for effective budgeting and financial planning.

-

Leverage Technology: Use technology and data analytics to assess market trends and compare offers from different banks. This informed approach can empower buyers to negotiate better terms.

Disclaimer on Indicative Prices

It is important to note that pricing in wholesale banking can vary widely based on numerous factors, including market conditions, client relationships, and service specifications. The insights provided here are indicative and should not be construed as fixed pricing guidelines. Always engage directly with financial institutions for accurate and current pricing information tailored to your specific needs.

Alternatives Analysis: Comparing wholesale banking With Other Solutions

Understanding Alternatives to Wholesale Banking

In the realm of financial services, wholesale banking is a significant player, particularly for large corporations and government entities. However, as B2B buyers explore their options, it’s essential to consider alternative solutions that may better suit their specific needs. This analysis will compare wholesale banking with two viable alternatives: Investment Banking and Peer-to-Peer (P2P) Lending. Each option offers distinct advantages and challenges that can influence decision-making for businesses operating in various global markets.

Comparison Table

| Comparison Aspect | Wholesale Banking | Investment Banking | Peer-to-Peer (P2P) Lending |

|---|---|---|---|

| Performance | High efficiency in large transactions | High performance in capital raising and M&A | Moderate, depending on the platform and project |

| Cost | Generally lower fees for high-volume transactions | Higher fees due to advisory services | Lower fees, but interest rates can vary |

| Ease of Implementation | Established processes, but can be complex | Can be lengthy due to regulatory requirements | Quick setup, user-friendly platforms |

| Maintenance | Requires ongoing relationship management | Intensive due diligence and ongoing support | Minimal maintenance; mostly automated processes |

| Best Use Case | Large-scale financing, corporate advisory | Mergers, acquisitions, capital raising | Small to medium-sized loans, consumer financing |

Detailed Breakdown of Alternatives

What Are the Pros and Cons of Investment Banking?

Investment banking is a comprehensive financial service that specializes in raising capital for corporations and governments. Its performance excels in complex financial transactions, particularly mergers and acquisitions. However, the cost of hiring investment bankers can be prohibitive, as their fees are typically high due to the bespoke nature of their services. While the implementation process can be lengthy due to regulatory requirements, the extensive market knowledge and strategic advice offered can be invaluable for businesses seeking to navigate significant financial endeavors.

How Does Peer-to-Peer (P2P) Lending Compare?

P2P lending platforms connect borrowers directly with individual investors, allowing for quicker access to capital compared to traditional banking methods. The ease of implementation is a significant advantage, as businesses can usually set up accounts and receive funding relatively quickly. Costs are generally lower, as these platforms often charge minimal fees compared to banks; however, interest rates can vary widely based on the risk profile of the borrower. The primary limitation of P2P lending is its performance, which may not be as robust for large-scale projects compared to wholesale or investment banking. Additionally, P2P lending is best suited for small to medium-sized loans rather than large corporate financing needs.

How Can B2B Buyers Choose the Right Financial Solution?

When selecting the most appropriate financial solution, B2B buyers should assess their specific needs, including the scale of financing required, the complexity of the financial transactions, and their budget constraints. Wholesale banking is ideal for large corporations with substantial transaction volumes and the need for tailored financial products. In contrast, investment banking may be more suitable for businesses looking to engage in strategic growth through mergers and acquisitions. Lastly, for companies seeking quick access to smaller loans, P2P lending presents a flexible and cost-effective alternative. By weighing these factors carefully, B2B buyers can make informed decisions that align with their organizational goals and financial strategies.

Essential Technical Properties and Trade Terminology for wholesale banking

What Are the Key Technical Properties in Wholesale Banking?

Wholesale banking operates on a complex framework of services tailored for large-scale institutional clients. Understanding the essential technical properties is crucial for B2B buyers, as these specifications dictate the level of service and efficiency they can expect. Here are several critical specifications to consider:

1. Credit Risk Assessment

Credit risk assessment is a process used by banks to evaluate the creditworthiness of their clients. This involves analyzing financial statements, credit history, and market conditions to gauge the likelihood of default. For B2B buyers, understanding this property is vital, as it influences the terms of loans and credit facilities offered, impacting cash flow and project financing.

2. Liquidity Management

Liquidity management refers to a bank’s ability to meet its short-term obligations without incurring significant losses. Effective liquidity management ensures that there are sufficient cash flows to cover liabilities as they arise. For businesses engaging in wholesale banking, this property is essential for planning financial strategies and ensuring operational continuity during cash flow fluctuations.

3. Transaction Processing Speed

The speed at which transactions are processed can significantly affect business operations, especially in time-sensitive markets. Wholesale banking services often involve large sums of money and complex transactions, making swift processing a critical property. B2B buyers should prioritize banks that offer advanced technological infrastructures that facilitate real-time processing to enhance operational efficiency.

4. Regulatory Compliance Framework

A robust regulatory compliance framework ensures that banks adhere to local and international laws governing financial transactions. This includes anti-money laundering (AML) regulations and know-your-customer (KYC) requirements. For B2B clients, engaging with a wholesale bank that maintains stringent compliance standards is crucial to mitigate legal risks and ensure smooth operations across borders.

5. Capital Adequacy Ratio (CAR)

The capital adequacy ratio is a measure of a bank’s capital, expressed as a percentage of its risk-weighted assets. It is an essential indicator of financial stability and operational capacity. For institutional clients, a higher CAR signifies a more resilient bank, which is less likely to face liquidity crises and can offer more substantial lending capabilities.

What Are the Common Trade Terms in Wholesale Banking?

Understanding industry-specific jargon is imperative for effective communication and negotiation in wholesale banking. Here are several common terms that B2B buyers should be familiar with:

1. OEM (Original Equipment Manufacturer)

In the context of wholesale banking, OEM refers to firms that produce products that are then marketed under another company’s brand. For banks, this could relate to financial products or services that are branded and sold by other institutions, allowing for a broader market reach.

2. MOQ (Minimum Order Quantity)

MOQ is the smallest quantity of a product that a supplier is willing to sell. In wholesale banking, this can refer to the minimum amount of a financial service or product that must be transacted, which is crucial for determining the feasibility of large-scale financial commitments.

3. RFQ (Request for Quotation)

An RFQ is a document issued by a buyer to solicit price quotes from suppliers for specific services or products. In wholesale banking, this process allows institutional clients to gauge competitive pricing for services like loans, underwriting, or foreign exchange transactions.

4. Incoterms (International Commercial Terms)

Incoterms are a set of predefined commercial terms published by the International Chamber of Commerce (ICC) related to international commercial law. In wholesale banking, understanding Incoterms is essential for managing cross-border transactions and ensuring that all parties are aware of their responsibilities regarding shipping, insurance, and tariffs.

5. SWIFT (Society for Worldwide Interbank Financial Telecommunication)

SWIFT is a messaging network used by banks and financial institutions to securely transmit information and instructions through a standardized system of codes. For B2B buyers, familiarity with SWIFT is important for understanding international payment processes and ensuring timely transactions across borders.

By grasping these technical properties and trade terms, B2B buyers in wholesale banking can make informed decisions that align with their strategic financial goals.

Navigating Market Dynamics and Sourcing Trends in the wholesale banking Sector

What Are the Current Market Dynamics and Key Trends in Wholesale Banking?

Wholesale banking is experiencing significant transformation driven by globalization, technological advancements, and evolving regulatory frameworks. International B2B buyers, particularly those in Africa, South America, the Middle East, and Europe, should be aware of these dynamics to navigate the market effectively.

One of the primary drivers of change is the increasing demand for customized financial solutions. Corporations and government agencies are seeking more tailored services that align with their specific operational needs, which has prompted banks to innovate their offerings. Additionally, the rise of digital banking solutions is reshaping traditional practices, enabling faster, more efficient transactions and data management. Technologies such as blockchain and artificial intelligence are becoming integral to risk assessment and fraud detection, enhancing the security and efficiency of wholesale banking operations.

Emerging trends include a shift towards sustainable finance, with banks increasingly focusing on environmental, social, and governance (ESG) criteria in their lending practices. This trend is particularly relevant for international buyers as they look for financial partners who align with their sustainability goals. Moreover, the growing importance of cross-border transactions has led to an increase in demand for services that facilitate international trade and currency management, underscoring the need for banks to have a robust global presence.

How Important Is Sustainability and Ethical Sourcing in Wholesale Banking?

Sustainability and ethical sourcing are becoming critical considerations for B2B buyers in the wholesale banking sector. The environmental impact of financial services is under increasing scrutiny, with stakeholders demanding transparency and responsibility in banking practices. As a result, many banks are adopting sustainable finance frameworks, which prioritize investments in projects that have positive environmental and social outcomes.

Ethical supply chains are not only a regulatory necessity but also a competitive differentiator. Banks are increasingly integrating ESG factors into their lending criteria, thereby encouraging corporations to pursue green projects. This shift is particularly relevant for buyers from regions such as Africa and South America, where sustainable development is a priority.

Green certifications and materials are gaining traction, as they provide a framework for assessing the environmental impact of projects funded by wholesale banks. Buyers should look for financial institutions that are committed to sustainable practices and can offer products that support their own sustainability objectives, such as green bonds or sustainable investment funds.

What Is the Brief Evolution and History of Wholesale Banking?

The evolution of wholesale banking dates back to the establishment of the first commercial banks in the 17th century, which primarily served merchants and large corporations. Over the centuries, the sector has matured significantly, influenced by economic shifts, technological advancements, and regulatory changes.

In the late 20th century, the globalization of finance led to the rise of multinational banks that could cater to a diverse range of corporate clients across borders. The introduction of sophisticated financial instruments, such as derivatives and structured products, allowed banks to offer more complex services tailored to the needs of large clients.

Today, wholesale banking continues to evolve, with an emphasis on digital transformation and sustainable finance. The sector is increasingly focused on building long-term partnerships with clients, providing not just capital but also strategic advisory services that align with their broader business objectives. For B2B buyers, understanding this evolution is crucial in selecting financial partners that can support their growth in a rapidly changing marketplace.

Frequently Asked Questions (FAQs) for B2B Buyers of wholesale banking

-

How do I select the right wholesale banking partner for my business needs?

Choosing the right wholesale banking partner involves assessing their experience in your industry, the range of services they offer, and their global reach. Look for banks that have a strong presence in your target markets, especially in regions like Africa or South America. Evaluate their risk management practices, technological capabilities, and customer service. It’s also beneficial to request case studies or client references to understand how they’ve successfully supported similar businesses. -

What are the key services offered by wholesale banks for international trade?

Wholesale banks provide a variety of services that facilitate international trade, including trade finance, currency exchange, and risk management solutions. They offer letters of credit and documentary collections to ensure payment security. Additionally, services such as foreign exchange management and export financing can help mitigate currency risk and improve cash flow. Understanding these services can help you optimize your international transactions. -

What factors should I consider when negotiating payment terms with a wholesale bank?

When negotiating payment terms, consider factors such as the size of your transactions, the bank’s policies, and your cash flow needs. Aim for flexible terms that align with your business cycles, such as extended payment periods or installment options. Also, assess any fees associated with payment processing and currency conversion, as these can impact overall costs. Clear communication about your expectations and needs is essential to reaching a mutually beneficial agreement. -

How can I ensure compliance with international regulations when using wholesale banking services?

To ensure compliance, familiarize yourself with the regulatory requirements in both your home country and the countries you are trading with. This includes understanding anti-money laundering (AML) regulations, tax obligations, and import/export restrictions. Work closely with your wholesale banking partner, as they often provide guidance and support for compliance matters. Regular training and updates on regulatory changes can also help mitigate risks. -

What is the minimum order quantity (MOQ) for wholesale banking transactions?

Minimum order quantities (MOQs) in wholesale banking can vary based on the specific services or products being utilized. For large-scale financing or trade transactions, banks may have a set threshold to ensure the viability of the deal. Discuss your business requirements with potential banking partners to understand their MOQs and find a bank that aligns with your operational needs and financial capacity. -

How can I assess the quality assurance (QA) processes of a wholesale banking provider?

To evaluate the QA processes of a wholesale banking provider, inquire about their risk assessment and management frameworks. Look for certifications or standards they adhere to, such as ISO quality management systems. Additionally, request information on their internal audit procedures and customer feedback mechanisms. A reliable wholesale bank should have transparent processes in place to ensure service quality and customer satisfaction. -

What logistical support can I expect from wholesale banks in managing international transactions?

Wholesale banks typically offer logistical support through dedicated trade finance teams that assist in managing documentation, shipping arrangements, and compliance with international trade laws. They can facilitate the smooth transfer of funds and provide insights into foreign markets. Additionally, many banks have partnerships with logistics companies to streamline the process of shipping goods, allowing for a more efficient transaction experience. -

How do I vet potential wholesale banking suppliers for reliability and trustworthiness?

To vet potential wholesale banking suppliers, conduct thorough due diligence, including checking their regulatory compliance and financial health. Review their credit ratings and seek feedback from current or past clients regarding their service quality. Look for banks with established reputations in your industry and consider their responsiveness and communication style. Engaging in initial discussions can also provide insights into their operational capabilities and reliability.

Important Disclaimer & Terms of Use

⚠️ Important Disclaimer

The information provided in this guide, including content regarding manufacturers, technical specifications, and market analysis, is for informational and educational purposes only. It does not constitute professional procurement advice, financial advice, or legal advice.

While we have made every effort to ensure the accuracy and timeliness of the information, we are not responsible for any errors, omissions, or outdated information. Market conditions, company details, and technical standards are subject to change.

B2B buyers must conduct their own independent and thorough due diligence before making any purchasing decisions. This includes contacting suppliers directly, verifying certifications, requesting samples, and seeking professional consultation. The risk of relying on any information in this guide is borne solely by the reader.

Strategic Sourcing Conclusion and Outlook for wholesale banking

What Are the Key Takeaways for Strategic Sourcing in Wholesale Banking?

In summary, strategic sourcing in wholesale banking is essential for fostering robust relationships between financial institutions and large corporate clients. This sector offers tailored solutions that cater to the complex needs of businesses, including mergers and acquisitions, trade financing, and risk management. By leveraging the extensive market knowledge and sophisticated infrastructure of wholesale banks, international B2B buyers can access significant capital and customized services designed to facilitate large-scale operations.

How Can International Buyers Leverage Wholesale Banking Services?

For buyers in regions like Africa, South America, the Middle East, and Europe, the global reach of wholesale banks presents invaluable opportunities for cross-border transactions and market expansion. Engaging with these institutions not only enhances financial capabilities but also provides insights into emerging trends and strategic advantages.

What’s Next for Your Wholesale Banking Strategy?

As the wholesale banking landscape evolves, it is crucial for B2B buyers to adopt a proactive approach in seeking out partnerships that align with their long-term goals. By prioritizing strategic sourcing, organizations can position themselves for sustained growth and competitive advantage in an increasingly interconnected world. Embrace this opportunity—explore partnerships with wholesale banks today to unlock your business’s full potential.