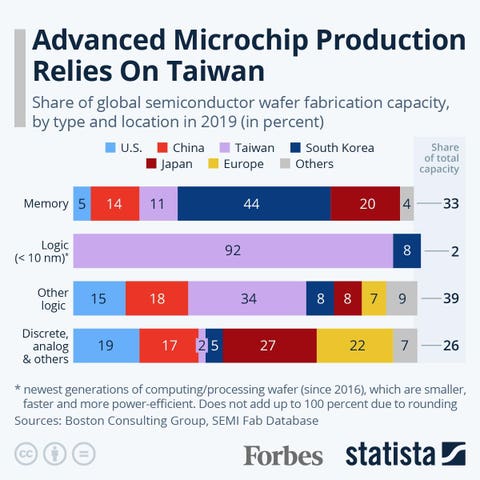

Taiwan has emerged as a dominant force in the global semiconductor industry, with its foundries accounting for over 60% of worldwide contract chip manufacturing revenue, according to data from Mordor Intelligence (2023). In particular, Taiwan Semiconductor Manufacturing Company (TSMC) alone captured approximately 59% of the global pure-play foundry market in 2023, solidifying the island’s pivotal role in producing advanced chips that power everything from smartphones to AI systems. While not the only chip manufacturer globally—South Korea, the U.S., and China also host key players—Taiwan stands out for its unmatched capacity, technological leadership in nodes below 10nm, and ecosystem maturity. The global semiconductor market, valued at USD 574 billion in 2022, is projected to grow at a CAGR of 8.7% through 2030 (Grand View Research, 2023), with advanced logic chips driving demand. Taiwan’s sustained investment in R&D, skilled labor force, and decades-long specialization in high-precision manufacturing have positioned it as the cornerstone of the world’s digital infrastructure, making its dominance in chip production a strategic economic and geopolitical focal point.

Top 5 Why Is Taiwan The Only Chip Manufacturers (2026 Audit Report)

(Ranked by Factory Capability & Trust Score)

Expert Sourcing Insights for Why Is Taiwan The Only Chip

H2: Why Is Taiwan the Only Chip Powerhouse in the Global Semiconductor Market? – 2026 Market Trends Analysis

As the global semiconductor industry accelerates into 2026, Taiwan remains the dominant force in advanced chip manufacturing, raising the question: Why is Taiwan still the only true chip powerhouse? Several interrelated technological, geopolitical, economic, and strategic factors explain Taiwan’s continued leadership, particularly through the dominance of Taiwan Semiconductor Manufacturing Company (TSMC), and underscore why no other region has yet matched its scale and precision in cutting-edge semiconductor fabrication.

- Technological Leadership and Manufacturing Excellence

Taiwan’s preeminence in chip manufacturing is anchored in TSMC’s unrivaled technological capabilities. By 2026, TSMC is expected to mass-produce chips using 2nm and early 1.4nm process nodes, maintaining a 2–3-year lead over competitors like Samsung and Intel. The company’s consistent R&D investment—projected to exceed $50 billion cumulatively from 2023 to 2026—enables it to push the boundaries of Moore’s Law. Taiwan’s ecosystem of specialized suppliers, engineering talent, and decades of process optimization create a formidable barrier to entry for would-be rivals.

- Concentration of Advanced Packaging and Ecosystem Integration

Beyond fabrication, Taiwan leads in advanced packaging technologies such as Chip-on-Wafer-on-Substrate (CoWoS) and System-in-Package (SiP), which are critical for AI and high-performance computing (HPC) chips. By 2026, demand for these packaging solutions—driven by AI accelerators from companies like NVIDIA and AMD—is surging. Taiwan’s vertically integrated semiconductor ecosystem, including EDA tools, material suppliers, and testing services, ensures rapid innovation cycles and high yield rates unmatched elsewhere.

- Geopolitical Dependencies and Supply Chain Realities

Despite global efforts to diversify semiconductor production (e.g., the U.S. CHIPS Act and EU Chips Act), most new fabs focus on mature nodes or lag behind in advanced manufacturing. By 2026, over 90% of sub-7nm chips will still be produced in Taiwan. The complexity, cost, and time required to replicate TSMC’s expertise mean that even with billions in subsidies, the U.S. and Europe will not achieve self-sufficiency in leading-edge chips before 2030. Meanwhile, geopolitical tensions elevate Taiwan’s strategic importance, reinforcing its role as the indispensable semiconductor node.

- Talent and Institutional Know-How

Taiwan benefits from a deep pool of semiconductor engineers, nurtured by institutions like National Taiwan University and decades of industry experience. TSMC’s proprietary manufacturing processes are the result of institutional knowledge accumulated over 35+ years—a “secret sauce” that cannot be easily transferred or replicated. As global demand for skilled chipmakers outpaces supply, Taiwan’s human capital advantage becomes even more pronounced.

- Strategic Customer Relationships

Leading tech firms—including Apple, NVIDIA, AMD, and Qualcomm—rely almost exclusively on TSMC for their most advanced products. These long-term partnerships, often secured through multi-year capacity commitments, give TSMC stable revenue and the financial confidence to invest aggressively in next-gen technologies. This customer lock-in effect further entrenches Taiwan’s dominance.

Conclusion

By 2026, Taiwan remains the only true chip powerhouse not due to accident, but because of a unique convergence of technological superiority, ecosystem maturity, human capital, and strategic positioning. While other nations invest heavily to catch up, Taiwan’s head start, compounded by the exponential complexity of advanced chipmaking, ensures its continued centrality in the global tech supply chain—making it not just a key player, but the irreplaceable cornerstone of the semiconductor era.

Why Is Taiwan The Only Chip (Quality, IP): Common Pitfalls in Sourcing

When sourcing semiconductor chips, many companies assume that Taiwan is the sole source of high-quality chips with robust intellectual property (IP) protection. While Taiwan—particularly through industry leaders like TSMC—dominates global advanced semiconductor manufacturing, this perception can lead to several strategic pitfalls. Relying solely on or overly favoring Taiwan without a nuanced understanding of the global landscape may expose businesses to supply chain risks, cost inefficiencies, and innovation limitations. Below are common pitfalls associated with this assumption.

Overlooking Diversification Risks

Assuming Taiwan is the only reliable source for high-quality chips can lead to dangerous over-concentration in the supply chain. Geopolitical tensions in the Taiwan Strait, natural disasters, or export restrictions could severely disrupt production. Businesses that fail to diversify across regions—such as South Korea, Japan, the U.S., or the EU—risk significant downtime and revenue loss during regional instability.

Misunderstanding IP Protection Beyond Geography

While Taiwan has strong IP enforcement in its semiconductor sector, equating geography with IP security is misleading. IP protection depends more on legal frameworks, contractual agreements, and internal corporate practices than on location alone. Companies may neglect to implement rigorous IP safeguards (e.g., NDAs, secure design flows, or audit rights) under the false belief that sourcing from Taiwan automatically ensures IP safety.

Ignoring Advancements in Alternative Markets

Believing that only Taiwan delivers cutting-edge quality overlooks rapid advancements in other regions. South Korea (Samsung), the U.S. (Intel, GlobalFoundries), and emerging players in Europe and China are investing heavily in advanced process nodes and packaging technologies. Failing to evaluate these alternatives may result in missed opportunities for cost optimization, innovation, or favorable trade terms.

Underestimating Total Cost of Sourcing

Taiwan’s leadership in advanced nodes often comes with premium pricing and long lead times. Companies that assume “Taiwan = best quality = must source here” may overlook total cost implications, including logistics, tariffs, and opportunity costs. In some cases, slightly lower process nodes from other foundries may offer better value for non-cutting-edge applications.

Neglecting Long-Term Strategic Autonomy

Overreliance on a single region, even a highly capable one like Taiwan, reduces strategic flexibility. Governments and industries worldwide are pushing for semiconductor sovereignty to reduce dependency on any one region. Companies that fail to consider multi-sourcing or onshoring strategies may find themselves at odds with future regulatory requirements or unable to respond to market shifts.

Confusing Foundry Leadership with Design Ecosystem

Taiwan excels in semiconductor manufacturing, but chip design and IP development are global activities. Assuming Taiwan owns or controls all valuable IP can lead to poor partner selection. Many leading fabless companies (e.g., NVIDIA, Qualcomm) design chips manufactured in Taiwan but hold IP developed in the U.S. or Europe. Sourcing decisions should separate manufacturing capability from IP origin and ownership.

Conclusion

While Taiwan remains a cornerstone of the global semiconductor ecosystem, viewing it as the only source of high-quality chips and secure IP is a strategic misstep. Businesses must avoid these common pitfalls by adopting a diversified, informed, and geographically agile sourcing strategy that evaluates technology, cost, risk, and IP protection on a case-by-case basis—rather than relying on regional assumptions.

Logistics & Compliance Guide for “Why Is Taiwan The Only Chip”

Overview of Taiwan’s Semiconductor Industry

Taiwan plays a pivotal role in the global semiconductor supply chain, primarily due to the dominance of companies like TSMC (Taiwan Semiconductor Manufacturing Company). Over 90% of the world’s most advanced chips are manufactured in Taiwan, making it a critical node in high-tech manufacturing. This guide outlines the logistics and compliance considerations when engaging with Taiwan’s semiconductor sector, particularly in the context of international trade, export controls, and global supply chain dependencies.

Export Controls and International Regulations

U.S. Export Administration Regulations (EAR)

The U.S. Department of Commerce’s Bureau of Industry and Security (BIS) regulates the export of semiconductor technology and equipment under the Export Administration Regulations (EAR). Advanced semiconductor manufacturing tools and certain chip designs are subject to strict licensing requirements, especially when destined for certain end-users or end-uses.

- License Requirements: Exporters must obtain a license for items listed on the Commerce Control List (CCL), especially those related to extreme ultraviolet (EUV) lithography and other advanced fabrication technologies.

- Entity List Restrictions: Companies or institutions in certain countries involved in activities contrary to U.S. national security may be placed on the Entity List, restricting access to U.S.-origin technology used in Taiwan’s fabs.

Wassenaar Arrangement

As a participating member, the United States and other countries coordinate export controls on dual-use goods and technologies, including semiconductor manufacturing equipment. Taiwan, while not a formal member, aligns its export practices with international standards through de facto cooperation.

Logistics of Semiconductor Supply Chains

Global Supply Chain Dependencies

Taiwan’s semiconductor industry relies on a globally distributed supply chain:

- Raw Materials: Silicon wafers, specialty gases (e.g., fluorine-based), and photoresists are imported from Japan, the U.S., and South Korea.

- Equipment: Key manufacturing tools come from U.S. (Applied Materials, Lam Research), the Netherlands (ASML), and Japan (Tokyo Electron).

- Final Distribution: Finished chips are shipped worldwide to electronics manufacturers in China, Vietnam, Mexico, and the U.S.

Transportation and Freight Management

- Air Cargo Dominance: High-value, low-weight semiconductor wafers and finished chips are predominantly shipped via air freight for speed and security.

- Cold Chain & Static Protection: Specialized packaging is required to prevent electrostatic discharge (ESD) and environmental damage during transit.

- Customs Clearance: Expedited customs procedures are essential. Use of bonded warehouses and free trade zones (e.g., in Taoyuan or Kaohsiung) helps defer duties and streamline international movement.

Compliance with International Trade Laws

Dual-Use and End-Use Monitoring

Due to the military-civilian dual-use nature of advanced chips, end-use verification is critical. Exporters and logistics providers must:

- Conduct end-user screening to avoid diversion to unauthorized entities.

- Maintain records of transaction history for audit purposes (typically 5 years under EAR).

- Implement Know Your Customer (KYC) protocols for downstream distributors.

Sanctions and Geopolitical Risks

- China-Taiwan Tensions: Shipping routes through the Taiwan Strait may face disruptions during geopolitical escalations. Contingency planning and route diversification are recommended.

- Secondary Sanctions: Companies using U.S.-origin technology in Taiwan must ensure downstream customers are not in violation of U.S. sanctions (e.g., Huawei-related restrictions).

Data Security and Intellectual Property Protection

ITAR and Cybersecurity Compliance

While most semiconductor tech falls under EAR, certain defense-related chip applications may be subject to the International Traffic in Arms Regulations (ITAR). Additionally:

- Cybersecurity protocols must protect chip design files (GDSII) during digital transfer.

- Non-Disclosure Agreements (NDAs) and secure data rooms are standard when sharing IP with logistics or manufacturing partners.

Export of Software and Technical Data

Design software (EDA tools from Synopsys, Cadence) used in chip development is export-controlled. Transfers to foreign nationals—even within Taiwan—may require authorization under “deemed export” rules.

Environmental, Social, and Governance (ESG) Considerations

Environmental Compliance

Semiconductor manufacturing is water- and energy-intensive. Logistics and operations must comply with:

- Taiwan EPA regulations on wastewater discharge and chemical handling.

- REACH and RoHS for shipments into the EU, restricting hazardous substances in electronics.

Labor and Ethical Sourcing

- Ensure third-party logistics (3PL) providers adhere to fair labor practices.

- Audit supply chain partners for compliance with anti-human trafficking laws (e.g., U.S. Uyghur Forced Labor Prevention Act).

Recommended Best Practices

- Engage Legal Counsel: Work with trade compliance attorneys familiar with U.S., EU, and Taiwan regulations.

- Automate Compliance Checks: Use export control classification number (ECCN) screening tools and automated license determination software.

- Diversify Supply Chains: Reduce overreliance on Taiwan by investing in alternative manufacturing hubs (e.g., U.S., Japan, EU).

- Maintain Audit Trails: Document all export transactions, licenses, and compliance training.

Conclusion

Taiwan’s unique position in the semiconductor industry brings significant logistical and compliance challenges. Navigating export controls, ensuring secure transportation, and mitigating geopolitical risks are essential for any organization involved in the global chip supply chain. Proactive compliance, robust logistics planning, and continuous monitoring of regulatory changes are key to sustainable engagement with Taiwan’s semiconductor ecosystem.

Taiwan is not the only chip manufacturer in the world, but it plays a disproportionately dominant role—particularly through Taiwan Semiconductor Manufacturing Company (TSMC)—in the global semiconductor industry. The conclusion to sourcing why Taiwan stands out as a pivotal player is as follows:

Taiwan has become the global leader in advanced semiconductor manufacturing due to a combination of strategic government investment, a highly skilled workforce, decades of industrial policy focused on technology development, and the emergence of world-class companies like TSMC. TSMC, in particular, leads the world in producing the most advanced and energy-efficient chips, used in everything from smartphones to artificial intelligence systems. Its technological edge, economies of scale, and consistent R&D investment have allowed it to outpace competitors in the U.S., South Korea, and elsewhere.

Geopolitically, this dominance makes Taiwan a critical node in global supply chains. However, it also introduces vulnerabilities, as regional instability could disrupt the supply of essential chips worldwide. While other countries are investing heavily to reduce reliance on Taiwan—such as the U.S. through the CHIPS Act—no current alternative matches Taiwan’s capacity and technological leadership in high-end chip fabrication.

Therefore, Taiwan is not the only chip manufacturer, but it is unmatched in producing the most advanced and widely used semiconductors. This leadership position is the result of long-term vision, sustained investment, and innovation—making Taiwan an indispensable player in the global tech ecosystem.